A One-Day Rival to Treasuries Is Born in Europe’s Pandemic Bonds

A One-Day Rival to Treasuries Is Born in Europe’s Pandemic Bonds

(Bloomberg) -- The European challenge to U.S. dominance of global financial markets just got a shot in the arm.

After a record-smashing debut bond sale by the European Union this month to help fund its pandemic recovery, traders are contemplating whether the region’s assets could one day emerge as an alternative haven to Treasuries. This was just the first salvo in the bloc’s plans to sell almost $1 trillion of debt in coming years, a move that will forge a fully fledged market that could ultimately lure investors to the euro at the dollar’s expense.

Of course, that’s still a fair way off. The U.S. Treasury has more than $20 trillion of debt outstanding across multiple maturities, a storied history of issuance and none of the political drama that’s plagued the EU’s integrity in recent years. But with questions raging over whether U.S. debt is losing its efficacy as a hedge, global reserve managers snapped up almost 40% of the EU’s recent 10-year social debt sale, and investors and policy makers are starting to contemplate a greater role for the euro in global markets.

“Though the Treasury market still remains much more important, it’s a big step forward,” said Francesco Papadia, former director general for market operations at the European Central Bank and now a senior fellow at the Bruegel think-tank in Brussels. “When thinking about the international use of the euro, there were two big related limitations: the absence of something like U.S. Treasuries and also of a safe yield curve for euro assets. These are partially dealt with by this large EU bond issuance.”

Since its creation over two decades ago, the euro has never posed a realistic threat to the dollar’s prime position in the global financial system. Key barriers have included the greenback’s benchmark status in international trading, EU institutional flaws exposed during the euro-zone crisis, and the lack of a euro-denominated haven asset.

The latter got a major boost this year after member nations overcame differences for a groundbreaking joint fiscal plan to fund the economic recovery from the coronavirus crisis. It’s a move that looked implausible before the pandemic -- the idea of jointly-issued debt was dismissed even during the perils of the euro-zone crisis -- and speaks to a faith in the resilience of the European project after a troubled decade.

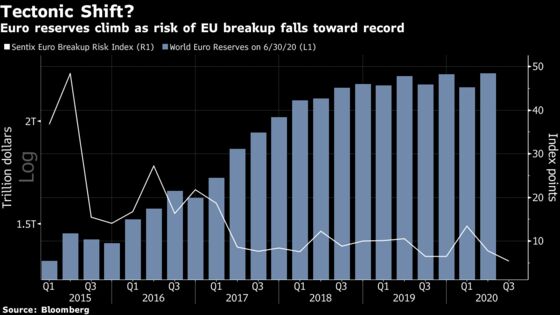

Investors have also gained more confidence. A measure of the probability of a country leaving the euro in the next 12 months is near a record low, based on a monthly survey of individuals and institutions. Meanwhile, the share of global reserves held in euros jumped 4% in the latest quarterly data, the most since early 2018, outpacing a 1.9% gain in the dollar equivalent.

Still, European policy makers showed little interest in promoting policies that would boost the euro’s international status until recently. The turning point was a 2018 address by former European Commission President Jean-Claude Juncker, according to Marek Dabrowski, co-founder of the Center for Social and Economic Research in Warsaw.

“This was a response to the increasing incidences of protectionism and unilateralism of the U.S. administration under President Donald Trump,” said Dabrowski, who wrote a paper for the European Parliament on the euro’s challenge to the dollar. “Now if you read ECB documents they look more friendly to the internationalization process.”

ECB President Christine Lagarde said in June that the reform measures to deal with the virus should also serve to safeguard the attractiveness of the euro globally. That followed the EU Commission’s President Ursula von der Leyen’s push “to strengthen the international role of the euro” in her agenda for Europe when she took office last year.

Dollar Pessimism

Markets could also support a longer-term shift to favor the euro. The currency has gained more than 4% this year to around $1.17, its second-best performance since 2007. The debt sharing could help it climb further to a six-year high of $1.30 in 2021, according to Mizuho International’s Peter Chatwell.

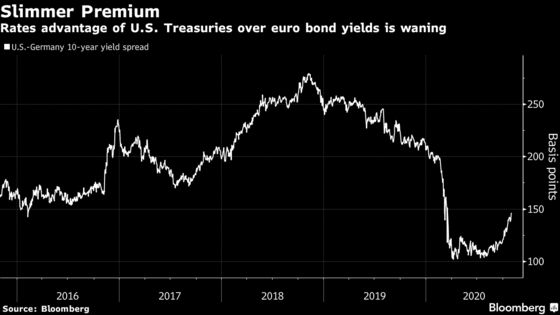

Many banks now see the U.S. currency entering a downtrend that could span years. Key to this is the Federal Reserve’s decidedly dovish policy bias, which is eroding the greenback’s interest-rate advantage and making dollar assets less attractive. The extra yield on 10-year Treasuries over German bunds is at 145 basis points, down from 210 at the end of 2019.

“The biggest foreign-exchange trends, now and for a long time, will be the Covid-induced downward convergence of interest rates,” said Kit Juckes, chief foreign-exchange strategist at Societe Generale SA. “This, I think, is unambiguously negative for the dollar, and far from priced-in.”

At the same time, unprecedented fiscal stimulus unveiled by U.S. policy makers threatens to worsen America’s budget deficit -- another negative for the dollar. The nation’s deteriorating external accounts also weigh on the currency.

Strategists at Credit Agricole SA see the euro’s long-term fair value against the dollar at around $1.24. They expect downside risks to U.S. growth, a dovish Fed and concerns about the country’s fiscal health to drive diversification out of the greenback and into the euro. The new EU bonds offer an ideal home for such rebalancing flows, they say.

‘Multi-Polar World’

For now, the expected volume of EU bonds still pales in comparison to the U.S. Treasury market. The bloc plans 100 billion euros ($117 billion) of social bonds by next year and another 750 billion euros for its pandemic fund, about a third of which will come from green bonds. So its appetite for joint issuance will need to outlast the coronavirus-induced economic slump.

“These are targeted and temporary measures, they’re not yet permanent,” said Alvise Lennkh, an executive director at credit ratings provider Scope Group. “If these measures were to become permanent through political decisions in the future -- for instance, the creation of a centralized fiscal capacity which would have a more permanent nature -- it would solidify the euro’s claim.”

These issues, along with other incumbency advantages such as the dollar’s use to price oil, gold and other commodities, stops analysts at Scope Group or Bruegel’s Papadia from seeing the euro upending the dollar in the foreseeable future. But events this year should lead to a narrowing gap between the shared currency and the greenback, they say, which in coming decades could result in a much-changed monetary universe.

“The global financial system is seemingly heading toward a multi-polar world with several dominant currencies rather than having one hegemon,” said Credit Agricole’s head of Group-of-10 currency strategy Valentin Marinov, noting China’s yuan will also likely have a larger role to play. “I would expect central banks across central and Eastern Europe for example to increase further their holdings of euros and reduce their dollars.”

©2020 Bloomberg L.P.