A Desperate Catalyst After Some Big Nothings: Taking Stock

A Desperate Catalyst After Some Big Nothings: Taking Stock

(Bloomberg) -- In news that should surprise no one, Thursday’s big "shocker" was that trade officials between the U.S. and China agreed to keep talking -- a result this column went out on a "limb" to predict just days ago. But with that overhang now removed, equities can now focus on monthly payrolls, a desperately-needed data point to force a re-rating of the S&P that is coming up on a key technical level.

Though this January was the best for equities in 30 years, it does come off the back of that volatile downdraft, and watching the action over the past week and a half, the recovery feels tenuous -- or at least a bit "stall-ey." Taking Wednesday and Thursday as examples, the market appears to be lurching from one catalyst to the next, seemingly at the mercy of binary events (read: FOMC decision, Chicago PMI). Once processed, we go sideways.

We also appear to be in the "where bad is good" territory on economic figures, as the bulls seek data that confirm and encourage the FOMC to stay pat on rates. The January Chicago PMI was case and point.

Payrolls data this morning are forecast for +165K, a little over half the prior month’s blow out number of 312K. The numbers ideally will force the market to make up its mind (perhaps juicing the declining volatility of late) now that his mega-week of catalysts is nearing an end. Futures are essentially unchanged, and the S&P is right up against the 100-DMA at 2712.

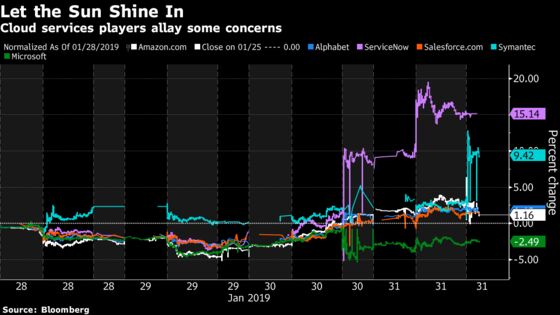

Clouds Part

Fears related to data centers and the cloud economy that surfaced with Intel and Nvidia this week have, at minimum, been further complicated as the week wore on. Results from MSFT (where its PC business, not its cloud, dragged on results), SYMC (CEO cited outperformance in Enterprise Security), NOW (results and forecast subscription revenue and billings growth exceeded analyst ests.), and now Amazon.com in results Thursday. The world’s largest publicly-traded company beat expectations for net sales in its AWS unit (web services), notching growth of 45% in the process (that said, shares are down 4% after rising 3% this week into the print). Nomura analysts after the results said "shares are about to look cheap," while Goldman analysts continue to see the company as the "best risk-reward’ in Internet.

Raymond James for one (there are nearly 50 analysts with bullish ratings on Amazon for what its worth), expected continued momentum and leadership in cloud, along with improving operating margins. This materialized, at least on TTM basis, validating not only their views, but also Bill Miller (of Legg Mason fame), who made a CNBC appearance midday to boost beauty company shares (AVP, COTY), and plug some Apple and Amazon stock. He says he expects Amazon’s international segment to stop losing money in the next few years, while also expecting the stock to double in three years (equating to ~$3,400, or 40% above the Street’s current 12-month Street-high target). AMZN’s results, according to Morgan Stanley, are a "bullish read-across" for Alphabet. The search engine giant is due to report Monday.

Sectors in Focus Today

- Paper, panel and lumber names after Weyerhaeuser, Norbord results, watch RYN, PCH LPX; RFP missed Thursday and tanked

- Chemicals again after LYB earnings missed on EBITDA and sales, after DowDupont Thursday halted the chemical rally in its tracks

- Integrated oil as XOM, CVX both report

- Pharmacy benefit managers after the HHS proposal to curb protections for drug plan rebates (CVS, CI were down post market)

- Cybersecurity and Internet names SWI, PANW, after Symantec’s results (PFPT also reported, with Keybanc writing that results show the market opportunity and execution remain strong)

- Active wear retail after Deckers Outdoor beat the highest estimate

On Tap for Next Week

The Super Bowl Sunday night (where the Patriots are favorites by 2.5 points over the Rams) may cast a haze over Monday’s action, which luckily features a fraction of the catalysts we saw this week. But Sunday, look for whether Vegas had it right, or video game maker Electronic Arts. The scarily accurate Madden video game (which has correctly picked the winner 10 of the last 15 times) sees the Rams in a comeback victory over the Patriots following an MVP performance from Aaron Donald.

But once you’ve recovered, its time to focus on the main event Monday, Alphabet earnings -- days after its FAANG brethren foreshadowed the state of play in tech land. Earnings will still dominate the week, save the State of the Union Address Tuesday night and the Bank of England interest rate decision as the major macro events (some markets in Asia will be closed for parts of the week for the Lunar New Year: Year of the Pig). The U.S. Government is still attempting to catch up to the backlog of delayed economic data from the shutdown, so keep an eye peeled on eco for your freshest updates.

Capri Holdings reports results (formerly Michael Kors -- the latest in a series of fashion houses that have re-branded, a la Tapestry (previously Coach) which also reports next week). Disney (we’ll be watching for updates on the Fox transaction) and Snap come Tuesday (Spotify late night), while General Motors and Chipotle are due mid-week. We’ll also follow Twitter on Thursday to see if it can hold some of the gains seen this week on the back of Facebook results.

Notes From the Sell Side

JPMorgan’s Tusa is out with additional commentary on, you guessed it, GE, in a note entitled, "The Math Still Matters." GE Thursday rose the most intraday since the depths the financial crisis (that notable March bounce in 2009), and Tusa writes that the stock reaction from 4Q results left the JPMorgan analysts "scratching our heads." He writes that one would need to have "highly optimistic" assumptions in FCF run rate to support a share price near $10 (last close $10.16). This follows Vertical Research’s downgrade to hold from buy late yesterday, which was mostly a valuation call. Analyst Jeffrey T. Sprague discussed the near 40% upward move in the shares since their upgrade in late December but is now uncertain as to the industrial conglomerate’s outlook. His sum-of-the-parts (SOTP) valuation puts shares at $11.

Floor & Decor just got double downgraded (to underperform from buy), and is indicated to open lower this morning after BofAML analyst Elizabeth L Suzuki wrote that despite healthy trends in renovation, the tailwinds for housing are "softening." She expects margins and comp sales to "fade lower," and highlights the late cycle of the bull market leading her to prefer Home Depot, Lowe’s and Whirlpool given their track records in such market conditions.

Tick-by-Tick Guide to Today’s Actionable Events

- Jan. Vehicle Sales Day

- Waste Management Phoenix Open is played at TPC Scottsdale (Jon Rahm the favorite at 7/1, followed by Justin Thomas at 9/1 odds)

- 8:00am -- MRK earnings call

- 8:30am -- Jan. Change in Nonfarm, Mfg Payrolls

- 8:30am -- Jan. Unemployment Rate

- 9:30am -- XOM earnings call

- 9:45am -- Jan. Final Markit US Manufacturing PMI

- 10:00am -- Jan. ISM Manufacturing, Prices Paid

- 10:00am -- Jan. Final U. Of Michigan Sentiment

--With assistance from Jeran Wittenstein.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.