A Booming Corner of Private Credit Has Some Investors on Edge

A Booming Corner of Private Credit Has Some Investors on Edge

(Bloomberg) -- Private equity firms are increasingly turning to an obscure type of loan, once almost exclusively used to finance smaller deals, to fund larger and larger buyouts. Yet a growing number of analysts and investors warn the debt may be riskier than it appears.

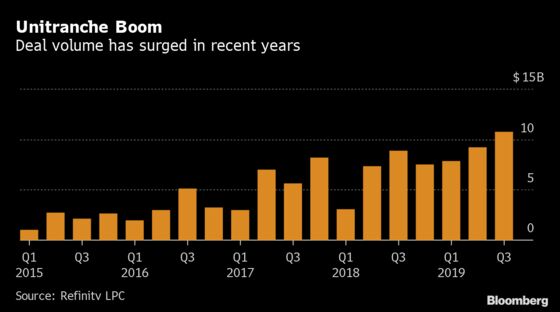

Demand for unitranches, which blend first-priority and subordinated loans into a single facility from just a handful of lenders, is surging as borrowers bypass conventional sources of financing in pursuit of greater speed and simplicity. Previously used solely to fund middle-market transactions, volume reached a record $10.7 billion last quarter as non-traditional lenders deploy more cash for deals that in the past may have gone to the institutional loan market.

The frenzied growth is another example of how red-hot demand for private credit is reshaping the global lending landscape. Yet the boom in unitranches is worrying some who say the debt, which is sometimes carved up via sophisticated side deals, remains unproven, especially in the face of a potential economic downturn and increase in restructurings. That could ultimately hurt investors who’ve plowed hundreds of billions of dollars into private debt funds in recent years.

“Unitranches have taken a lot of the market share because the market has evolved toward that need for speed,” said Garrett Ryan, head of capital markets at Twin Brook Capital Partners, a direct lender that provides financing, including unitranche loans, to middle-market companies.

That need for speed has come at a price, some market participants say.

By combining senior and junior debt into a single tier and eliminating the syndication process, unitranches can be arranged in a fraction of the time it takes to complete a traditional leveraged loan.

The structure made up about 21% of private equity sponsored middle-market deals this year through September, up from 14% in 2018 and just 2.5% five years ago, according to data from Refinitiv LPC.

Yet recently more buyout firms are turning to unitranches to finance bigger deals as direct lenders amass larger pools of capital to invest. The pacts that can be used to spread out the risk once a loan is complete are also becoming increasingly complex.

More importantly, they remain largely untested in distressed scenarios, fueling a degree of uncertainty not present in other types of financing, firms including Fitch Ratings warn.

“All of this is going to be tested, and there will be some real pain,” said Jeff Dickson, executive managing director and head of alternatives at PGIM Private Capital. Dickson said he’s avoiding unitranche deals because they’re not compensating investors enough for the underlying risk.

“It’s all uncharted territory,” he added.

Read more: Another jumbo loan falls to the booming world of private credit

Among the biggest questions is whether bankruptcy courts even have jurisdiction over the side deals, known as an agreement among lenders. Partitioned unitranche debt is still governed by just one set of loan documents. A bankruptcy court may recognize the investors as having a single claim against the borrower, even though the private agreements often contain payment priorities and waterfall provisions.

If a court were to decide it does not have purview over a contract that doesn’t involve the debtor, that would likely force the intercreditor dispute into state or federal court, significantly delaying recovery efforts, according to Fitch.

About $4.7 billion of unitranche financings in the third quarter were for larger corporate deals. That pushed the average loan size in the period to a record $235 million, Refinitiv data show.

In August New Media Investment Group Inc. secured a $1.8 billion loan from Apollo Global Management for the acquisition of Gannett Co.

That was on the heels of a $1.25 billion unitranche that financed Ion Investment Group’s purchase of financial data provider Acuris in June.

Antares, Bain

As unitranches have gotten bigger, more lenders are joining forces to underwrite the financings, allowing some to avoid side agreements altogether.

Among the largest players in the booming market are household names in the direct-lending world -- Varagon Capital Partners, Twin Brook, Ares Management, Golub Capital and Antares Capital, which two years ago banded together with Bain Capital Credit to form a joint venture specifically dedicated to unitranches.

“Our goal in general is to provide the sponsor with multiple options in term of how they can finance the business,” said Timothy Lyne, a founding partner at Antares. “They can choose the syndicated route, the club route, or the unitranche, which is absolutely a higher bar from a selection process. Because we’re going deeper into the capital stack, we’re going to be more selective.”

As the unitranche market grows, the loans are also getting cheaper relative to dual first-lien and second-lien structures.

The extra yield lenders were compensated to own a unitranche reached an all-time low of 38 basis points in the fourth quarter before rising slightly in 2019, according to data from Refinitiv. Private equity-backed unitranches have priced to yield an average of 604 basis points over the London interbank offered rate this year, the data show.

“I see no reason why unitranche as a financing solution won’t continue to grow as long as the pricing is competitive and the terms are favorable,” said Jeffrey Stevenson, managing partner at private investment firm VSS. “There’s a hunger for yield, so the source of capital should continue to flow into these debt providers who will in turn have increasingly large pools of capital to deploy.”

--With assistance from Lisa Lee.

To contact the reporters on this story: Kelsey Butler in New York at kbutler55@bloomberg.net;Allison McNeely in New York at amcneely@bloomberg.net

To contact the editors responsible for this story: Natalie Harrison at nharrison73@bloomberg.net, ;Rick Green at rgreen18@bloomberg.net, Boris Korby, Sally Bakewell

©2019 Bloomberg L.P.