A Big Secret in Japan Debt Market Is Getting Harder to Keep

A Big Secret in Japan Debt Market Is Getting Harder to Keep

(Bloomberg) -- It’s an oddity of Japan’s corporate bond market: many debt sales that bankers said were successful actually weren’t. The secret may be getting harder to keep.

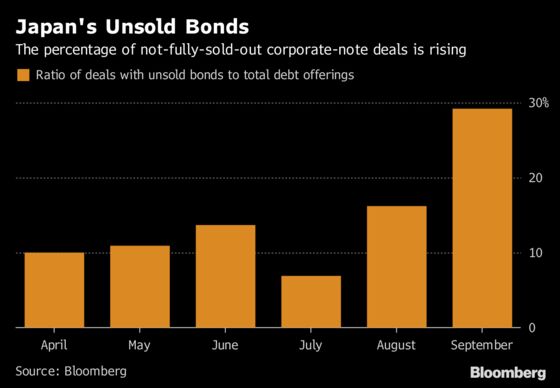

Underwriters failed to fully sell at least 29 percent of company note offerings in September, twice the average over the past six months, according to information compiled by Bloomberg based on more than 400 interviews with investors, underwriters and issuers.

Deals from Japan Airlines Co., Japan Tobacco Inc., Honda Finance Co. and Idemitsu Kosan Co. were among them, said some of those people, who asked not to be identified discussing a sensitive topic. Spokespeople for all four companies said that’s not what they were told by their banks.

It’s hardly a financial-system flaw for underwriters to soak up part of a deal. That’s what they’re paid to do. But not being transparent about it can create problems.

The fudging on unsold bonds is either to cover up a lack of demand, salvaging business relationships with issuers, or to give underwriters room to make nice with favored clients by selling them the leftover securities at a discount later, according to the people familiar with the matter. That can be to the detriment of investors who paid more for the bond at the initial offering, and also if it further drives down the market price.

A surge in issuance encouraged the practice in September. Companies had held off from selling bonds after a July policy tweak by the Bank of Japan, then scrambled to issue debt from late-August as bond yields settled down.

Spokespeople for Japan Airlines, Japan Tobacco, Honda Finance and Idemitsu said that underwriters told them that there were more orders than available bonds in their respective deals. Spokespeople for the five biggest underwriters of Japanese corporate bonds so far this fiscal year -- Mizuho Securities Co., Daiwa Securities Co., Nomura Securities Co., SMBC Nikko Securities Inc. and Mitsubishi UFJ Morgan Stanley Securities Co. -- declined to comment.

Bloomberg News has been tracking unsold bonds in Japan since July 2017, obtaining the information by interviewing issuers, investors and underwriters.

Some of the yield premiums on the unsold notes have risen more than the market as a whole. The spread on Japan Tobacco’s 2038 bonds, for example, has climbed four basis points since its sale last month, and the extra yield on Japan Airlines’ 20-year debt has increased 1 1/2 basis points. Spreads on Japanese corporate notes have been flat since mid-September, according to an ICE BofAML index.

Regulators and an industry group have acknowledged that some of the trading practices in Japan’s corporate debt market are opaque. In a 2010 report, the Japan Securities Dealers Association said there was criticism that bond terms had at times diverged from market levels due to inaccurate reporting by underwriters on demand for the securities.

Little by little, changes are being made.

Some borrowers, especially those issuing Samurai and hybrid securities, are selling notes using the so-called pot system, under which syndicate banks share details with issuers about bond buyers to find the best prices. It’s the norm for debt sales in the U.S. and Europe.

Disclosure Change

The JSDA also began from October to reveal whether, in bond trades on the secondary market, the seller was a brokerage or not. If it was and the note had been issued recently, there’s a possibility that the brokerage was unloading a bond it couldn’t sell earlier in the primary market as an underwriter, according to investors familiar with the matter.

The industry group only divulges this information for issues where credit ratings are AA level or higher. A working group discussed last year whether to expand the disclosure to bonds graded at the A level, but decided against it due to opposition from brokerages, said Katsuyuki Tokushima, the chief investment analyst at NLI Research Institute in Tokyo who is a member of the group. The topic may be revisited at the working group’s annual meeting next month.

To contact the reporter on this story: Issei Hazama in Tokyo at ihazama@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum

©2018 Bloomberg L.P.