A $200 Billion Exotic Quant Trade Is Facing Existential Doubts

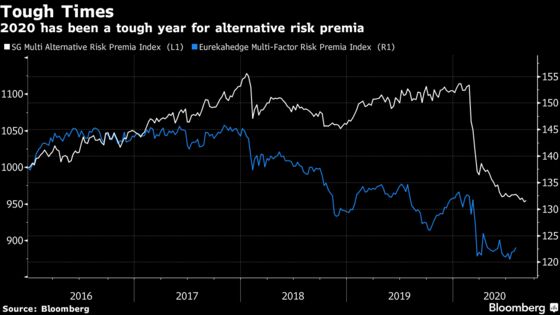

Strategies used in the ARP mix from stock trend-following to volatility insurance, were whipped around because of pandemic.

(Bloomberg) -- When 2020 began, one of the hottest businesses on Wall Street was selling exotic quant trades known as alternative risk premia. These strategies were marketed as diversifying, loved by hedge funds and priced cheaply.

Then Covid-19 happened.

As the pandemic gripped markets, strategies commonly used in the ARP mix from stock trend-following to volatility insurance were whipped around like never before. That meant these funds largely failed to live up to their uncorrelated hype in the sell-off, and were then left behind by the ferocious rebound in risk.

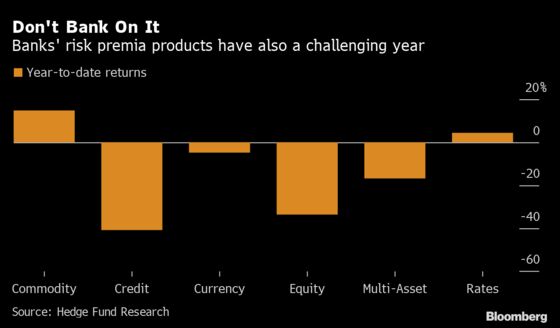

Eight months into the year, Societe Generale SA’s ARP index is down 14%. A Eurekahedge benchmark tracking indexes sold by investment banks has lost 7%. Managers including GAM Systematic and AQR Capital Management have seen their assets in such funds at least halve in 2020.

The fear is that ARP funds, with an estimated $200 billion overall, have either became too popular for their own good, or are ill-suited for a market shifting between meltdown and melt-up at a record pace.

“Allocators have been wondering whether these things really work,” said Antti Suhonen, senior adviser at MJ Hudson Allenbridge in London, which offers investment advice to institutions. “It’s true this year has seen very exceptional moves. But even so the performance has been disappointing.”

ARP products combine a diverse bunch of trades, often tried-and-tested ideas beloved by quants such as the tendency for cheap stocks to outperform in the long run or for short-term commodity futures to trade below long-term ones. The composition of funds and their returns vary vastly, but managers can point to a few unifying trends that have been a drag on performance in 2020.

The March turmoil upended the normal trading patterns these strategies rely on. Then the fast market recovery whipsawed trend-following systems and forced systematic models to dial back market exposures and miss out on gains.

At the same time, many popular factors used by these funds -- such as value and foreign-exchange carry -- failed to rebound along with stock benchmarks.

“The recovery depended on whether you were in those main long risk categories of liquid equities and fixed income,” said Anthony Lawler, head of GAM Systematic, which oversees about $3 billion. “ARP by and large are not in those things.”

This year is adding to growing doubts over ARP, which has lagged stock indexes in recent years but has also posted a mixed performance as a portfolio diversifier. While defenders would argue that these products were never supposed to be a hedge against traditional assets, many investors likely got a different impression from their marketing, says MJ Hudson’s Suhonen.

That disappointment has now spurred something of an industry reckoning, with some quants tweaking models while others adopt a fundamental re-think. At Unigestion, for example, the team has added a momentum signal that makes sure the fund isn’t putting too much money in losing strategies, investment manager Joan Lee says.

On Wall Street, where investment banks sell ARP strategies individually as swap products, the response has been to churn out an ever wider range of indexes for clients. If the old ones are struggling, at least there are new ones on offer, the thinking goes.

Guillaume Arnaud worries that the quant strategies long documented by academics have now become too crowded in today’s market. At Societe Generale SA, he and his team have been touting lesser-known strategies, such as one that takes advantages of the gap between short- and long-term repurchase agreements.

“Premia that are less researched or implemented can prove to be a bit more juicy,” said Arnaud.

JPMorgan Chase & Co.’s Arnaud Jobert, who runs the equity side of bank’s Investable Indices franchise, says the bank has also expanded its menu into more sophisticated ARP strategies. That’s helped contribute to the nearly three-fold increase over the past three years in the number of indexes on sale to about 4,000 currently, according to a person familiar with the matter.

While many in the industry are soul searching, there is always the possibility that poor performance is cyclical. For some quants, now might be the best time to bet on lagging strategies.

“At some point we do think there is a tremendous amount of money to be made as fundamentals return back to equity markets and value and other factors start performing,” said Deepak Gurnani, founder of ARP Investments in New York. “However, the timing is somewhat uncertain.”

©2020 Bloomberg L.P.