Much of America Is Shut Out of The Greatest Borrowing Binge Ever

Even amidst the credit boom, smaller firms that power America’s economic engine are often being shut out.

(Bloomberg) -- Unprecedented government stimulus has allowed more companies to borrow at lower rates than ever before. Yet amid the credit boom, smaller firms that power America’s economic engine are often being shut out, hamstringing the recovery just as it begins.

The Federal Reserve’s pledge to use its near limitless balance sheet to buy corporate bonds has aided stricken airlines, oil drillers and hotels. It’s also helped companies from Alphabet Inc. and Amazon.com Inc. to Visa Inc. and Chevron Corp. access some of the cheapest financing ever seen. All told, firms have sold about $1.9 trillion of investment-grade debt, junk bonds and leveraged loans this year, according to data compiled by Bloomberg.

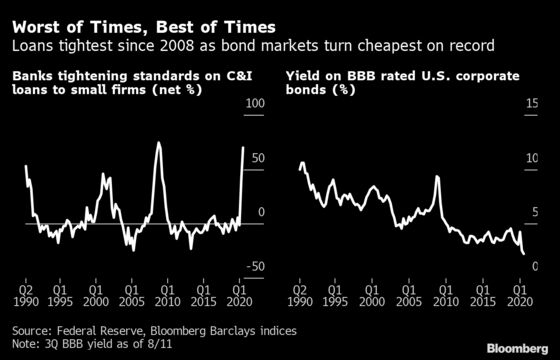

But for companies not large enough to tap fixed-income markets, the outlook is much more dire. Banks are tightening conditions on loans to smaller firms at a pace not seen since the financial crisis, while many direct lenders that have traditionally focused on the middle market are pulling back or turning to bigger deals instead. What’s more, the Fed’s emergency lending programs for mid-sized businesses and municipalities have been criticized as slow, complex, and largely inaccessible.

A lack of credit for small and medium-sized firms could tip many into bankruptcy, adding to the thousands of local businesses that have already quietly disappeared amid the pandemic’s mounting devastation. Given the sector employs roughly 68 million Americans -- Fed Chairman Jerome Powell calls it America’s “jobs machine” -- and is critical to regional economies across the U.S., a prolonged inability to access financing runs the risk of stalling the nascent rebound.

“The Fed actions have moved issuers that are big enough in front of the velvet rope, and those that aren’t stay outside,” said Peter Atwater, founder of research firm Financial Insyghts and an adjunct lecturer of economics at university William & Mary. “Capital markets access has become a determiner of life or death for business.”

That’s not to say the Fed’s current policy approach is necessarily misguided. In fact, many economists commend its quick and decisive actions when the pandemic hit and say those bold steps were key in staving off another financial crisis and possibly even a depression. But amid such large-scale intervention, certain parts of the economy are clearly benefiting more than others -- the big and powerful over the small and financially vulnerable, a disparity that to some degree mirrors the broader inequality problems that have been exposed by the pandemic.

The Fed announced its corporate bond-buying plan in March, opening the issuance floodgates after the coronavirus outbreak brought the market to a virtual standstill. Investment-grade firms have borrowed more than $1.3 trillion in 2020, a record pace, while junk-rated companies have sold $274 billion of bonds, according to data compiled by Bloomberg. In addition, they’ve priced over $270 billion of leveraged loans.

Alphabet’s $10 billion bond sale earlier this month saw record-low yields on the seven-year portion, besting levels set by Amazon in June. Chevron priced a two-year bond with an unprecedented 0.333% coupon earlier this week, while Visa issued seven, 10- and 30-year notes that all beat or matched previous records.

On the high-yield side, aluminum-packaging company Ball Corp. sold $1.3 billion of 10-year notes at 2.875% on Monday, the lowest ever for a U.S. speculative-grade offering with a maturity of five year or longer.

“It’s a battle between the Fed’s $750 billion special purpose vehicle to buy corporate investment-grade and high-yield bonds and those who don’t have access to this free money,” said Stephen Blumenthal, chief executive officer at money manager CMG Capital Management Group Inc.

Survival Uncertain

It’s a battle that smaller companies are decidedly losing.

Some 70% of bank senior loan officers surveyed by the Fed said they have tightened lending standards on loans for small commercial and industrial firms in the third quarter. That’s the highest proportion since late 2008. The trend also extends to mid-size and larger firms as well, though the latter enjoy unprecedented access to capital markets. About 54% said they increased premiums for small borrowers, the most in over a decade.

“Everyone is willing to lend to the biggest firms,” said Olivier Darmouni, a professor of finance at Columbia Business School. “But since the pandemic has not been tamed, creditors are now asking if the businesses will actually survive and they’ll get their money back. For smaller firms, there’s a lot more uncertainty of that.”

In a bid to encourage banks to extend credit to mid-size firms, the Fed introduced its $600 billion Main Street Lending Program in April, wherein those making eligible loans can sell 95% of them to the central bank. Despite efforts to broaden the program, it’s issued just $253 million in loans as of Aug. 10. That’s compounded criticism that it only works for a narrow set of companies, is too complex and doesn’t provide enough incentive to risk-averse lenders.

Boston Fed President Eric Rosengren said Wednesday that as borrowers and banks become more familiar with the program, it’s seeing a steady increase in participation, adding that it may become even more essential should the coming months bring a resurgence of the virus.

A spokesman for the Fed referred Bloomberg to Rosengren’s remarks when contacted for comment.

Still, the facility stands in contrast to the Paycheck Protection Program, run by the Small Business Administration and the Treasury, which dolled out more than 5.2 million loans totaling $525 billion before closing last week. The PPP facility, for its part, has gotten its own share of criticism, with some saying the smallest companies and those in disadvantaged areas have been shut out, while politically connected businesses and firms that aren’t struggling have gotten funding.

Making matters worse, direct lenders, which often provide financing to small and mid-size firms, have been retrenching for months as they tend to their own portfolios, while those sitting atop the most capital are increasingly targeting bigger deals.

Business development company Ares Capital Corp. said on a second quarter earnings call that the average Ebitda size of companies it finances has doubled versus the same period a year ago, and that it’s also charging more to lend. Apollo Global Management Inc. set up a new lending business last month focusing on loans of around $1 billion.

“There is little the Fed can do when there are liquidity issues outside the banking system,” Financial Insyghts’s Atwater said. “It has really highlighted the challenge in trying to provide credit to small businesses in a way that is prudent for the lender.”

Cerebro Capital, an online platform that allows middle-market borrowers to source credit facilities, saw a surge in demand for its services amid the tighter lending market, according to Allan Smallwood, senior director of capital markets at the firm. At the end of July, Cerebro helped a fifth generation family-owned commercial printing business close a deal after its existing bank lender exited when it tripped a loan covenant, he said.

Haves, Have Nots

Of course, the tale of diverging ‘haves’ and ‘have nots’ is hardly new in credit, manifesting when economic turbulence prompts lenders to retrench and investors to seek the relative safety of stable, blue-chip firms.

But the magnitude of the disparity this time around is more alarming when combined with expectations for record corporate defaults this year and following second quarter data showing the economy suffered its sharpest downturn since at least the 1940s. A growing chorus is also warning on inflation, which can hit smaller firms particularly hard. One of those is Larry McDonald, founder of The Bear Traps Report investment newsletter.

“It’s an inequality explosion in terms of financial sustainability,” said McDonald, who also authored the book ‘A Colossal Failure of Common Sense’ about the demise of Lehman Brothers Holdings Inc. “You have financial conditions tightening in some spots, and then wide open for the big guys -- it’s crazy.”

©2020 Bloomberg L.P.