The Biggest Bull on a Gasoline-Powered Future Is… 7-Eleven?

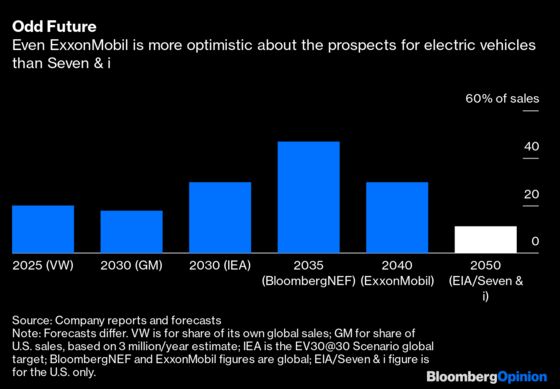

(Bloomberg Opinion) -- You might think that 2020 was the year everyone gave up on petroleum-powered transport. Royal Dutch Shell Plc Chief Executive Officer Ben van Beurden has expressed doubts about whether oil demand will ever return to pre-Covid levels. The world’s largest carmaker Volkswagen AG pledged that more than a fifth of its vehicles will be battery-driven by 2025.

The International Energy Agency is pushing for 30% of vehicle sales to be electric by 2030 and expects gasoline demand to peak late this decade even under current policies. Major oil refineries are switching to manufacture raw materials for plastics and jet fuel on the expectation that consumption in their core market of powering road transportation is in decline.

Seven & i Holdings Co. has a different view. It’s impossible to see the 7-Eleven owner’s $21 billion offer to buy Marathon Petroleum Corp.’s Speedway convenience stores as anything but a wager on the future of their main sales item: gasoline.

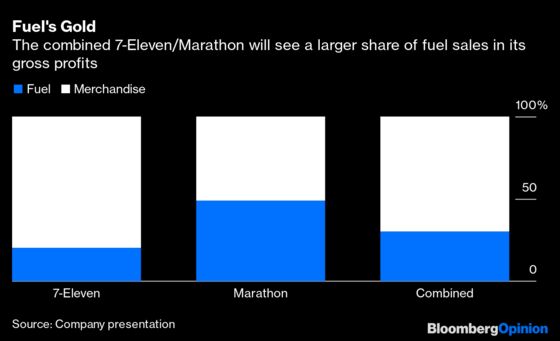

Seven & i’s motivation is straightforward. Speedway has 3,900 sites concentrated in the Midwest and South of the U.S. That’s equivalent to about 40% of 7-Eleven’s existing North American network, and turns over about $1.5 billion of annual earnings before interest, taxes, depreciation and amortization. By using its convenience-store expertise, Seven & i can upgrade Speedway’s shelves to a more attractive and profitable mix of own-brand products. Fuel, which accounts for about three-quarters of revenue and half of gross profit, will largely look after itself.

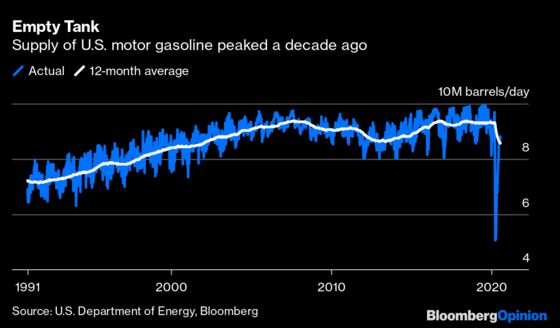

As we've written, that prediction looks like a mistake. Even under a Trump administration that’s worked hard to tear up fuel-economy rules, gas demand has stood still for four years. Despite evidence that urban traffic has rebounded close to pre-pandemic densities and long holiday road trips are exceeding former levels, on a trailing 12-month basis, gasoline consumption is currently at its slowest since the early 2000s.

The increasing efficiency of conventional vehicles is already enough to reduce the amount that car owners spend filling the tank and the number of trips they make to gas stations, a dynamic that will hurt both the fuel and non-fuel sides of the business.

Add in the impact of electric vehicles and the effect will be compounded. At present, there are just 1.5 million on U.S. roads; by the end of the decade, General Motors Co. expects to see at least twice that number sold there every year, equivalent to nearly 20% of annual sales. While gas stations can install chargers to accommodate this market, battery vehicles charged at home or in workplaces won’t have to make the regular visits to the pump and convenience store that even hybrid cars require.

The risk for Seven & i is that it’s willfully blind to these looming changes. Battery cars as a share of U.S. vehicle sales will rise to just 5% in 2030 and 11% in 2050, according to its presentation. That’s drastically lower than most carmakers and oil companies are predicting (BloombergNEF pegs the share at around 25% in 2030 and above 60% by 2040).

Remarkably, Seven & i posits as one of the “reasons for the acquisition” the way that taking control of Marathon’s store network will help it achieve environmental, social and governance goals such as installing energy-efficient lighting, switching stores to renewable power, and reducing use of plastic packaging.

This misses the forest for the trees. The overwhelming majority of emissions from a gas station aren’t the Scope 1 and Scope 2 type generated on-site and from buying electricity, but the Scope 3 carbon generated when the fuel it sells is burned in car engines.

Unlike the ESG initiatives that Seven & i boasts about, this isn’t just a nice-to-have factor to stick in the corporate responsibility report. The shift that the automotive and petroleum industries expect to see in the power-trains of road vehicles over the coming decade is a challenge to the core of the fuel retail model. With this deal, 7-Eleven will go from depending on gas for 20% of its gross profit to 30%. It’s heading the wrong direction down a one-way street.

Although the 7-Eleven brand is used around the world, we're using "7-Eleven" in this article to refer to the North American unit owned by the Japanese parent company, Seven & i.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2020 Bloomberg L.P.