Top India Microlender Seeks $900 Million to Finance Loan Growth

One of India’s top microlenders needs the cash to meet its credit-growth target of about 40 percent for the year ending March.

(Bloomberg) -- One of India’s top microlenders is seeking about 60 billion rupees ($900 million) from banks and non-bank lenders to fund loan growth as demand from borrowers living in small towns and rural areas bucks the slump in the nation’s overall credit offtake.

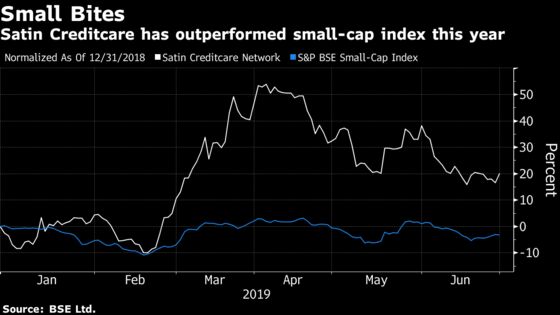

Satin Creditcare Network Ltd., whose assets exceed 70 billion rupees, needs the cash to meet its credit-growth target of about 40% for the year ending March, Chairman H. P. Singh said by phone. Its shares have handily beaten an index of small-cap stocks this year as the lender’s credit profile has remained largely unscathed amid the lingering shadow-banking crisis.

Key Comments

- Not expecting rise in overall funding costs as major part comes as loans from banks and non-bank lenders

- Credit ratings of Satin haven’t seen a downgrade by any of the four rating companies as the lender doesn’t rely on mutual funds for financing requirements

- NOTE: Shadow lenders raising money from mutual funds have been under stress as they turned cautious on lending after defaults by the IL&FS Group last year

- Loans at microfinance companies have been growing at a faster pace than commercial banks over the last six years as the majority of their customers are small borrowers in rural areas where demand remains strong

- NOTE: Loans at microlenders grew by an average 26% since 2014, almost double the rate seen at banks during the period

- The company plans to apply for a small finance bank license as and when the Reserve Bank of India announces rules for the permit

- The microfinance companies aren’t facing the challenge of asset-liability mismatch as the loans are small and for shorter duration. A low bad loan ratio also help them to remain less impacted than other categories of non-bank finance lenders: Chokkalingam G, managing director at Equinomics Research & Advisory Ltd.

To contact the reporter on this story: Nupur Acharya in Mumbai at nacharya7@bloomberg.net

To contact the editors responsible for this story: Divya Balji at dbalji1@bloomberg.net, Anto Antony, Ravil Shirodkar

©2019 Bloomberg L.P.