Earnings Monsters Build to Power Above This Range: Taking Stock

Tons of Firepower Is Building to Blast This Range: Taking Stock

(Bloomberg) -- Tuesday is looking a lot like yesterday (crude is higher again) with the exception that Europe has reopened following the Easter holiday, and there are earnings monsters powering higher early.

Equities have looked comfortable around the 2,900 level in the S&P 500, and with no major macro themes lingering (a formal trade deal may provide a slight pop but a deal is mostly being priced in at this point), the burden rests with individual earnings names to break this holding pattern -- a range that has held for much of the past month. What is true is that this week packs enough firepower, with trillions worth of market cap due to report (like heavyweights VZ, KO, PG, TWTR, LMT and UTX this morning; TXN, SYK, and EBAY post market). Hasbro is up 16 percent already, Twitter is adding another 8%, while KO and UTX are adding another 3.5% each.

In more company-specific news, Tesla’s investor day didn’t provide many bombshells outside its plans for a robotaxis and an ambitious plan to push autonomous driving. Morgan Stanley’s Adam Jonas wrote that it “left big questions” around timing and didn’t do enough to alter their views on the need for human drivers -- a material factor in whether the concept gains traction from a financial standpoint. With earnings just around the corner, it will be interesting to see how investors choose to value the future versus the present.

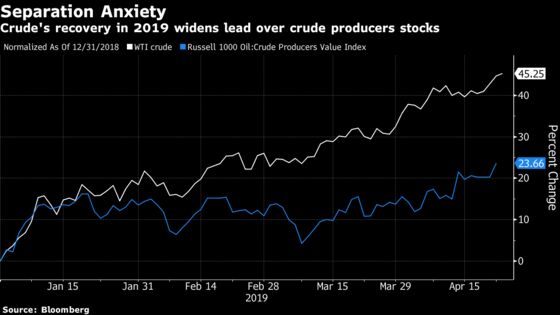

Energy led Monday, with the S5ENRS the leading gainer off the back of a boost in crude prices. Today looks similar as Brent and WTI continue to post fresh-2019 highs. The narrative in the segment has, and appears to to continue to be, the fact that stocks have failed to keep pace with the black liquid. Credit Suisse last week wrote that the higher oil prices were "not reflected in energy performance."

Third Eye

About a third of both the staples and financials sectors of the S&P 500 have reported results thus far, and what little visibility that provides, its a lot more than the other segments of the S&P. From a top-line perspective, results have tracked about in line with estimates, while earnings surprises are definitely leaning bullish. As far as that "earnings recession" narrative we’ve read so much about, earnings and sales are both tracking for growth, according to data compiled by Bloomberg.

A series of regional banks and some larger staples are on the docket today, two sectors that didn’t do much for the S&P Monday (insurance names were the main culprit behind financials weakness) as some rate sensitive sectors and industrials dragged (Boeing accounted for nearly half the segments weakness ahead of its results Wednesday -- more on that below).

Kimberly-Clark’s results almost single-handedly prevented staples from dragging the S&P negative, as nearly 2/3 of the segment were in the red. Equal-weighted Morgan Stanley noted KMB’s multiple expansion could be attributed to an “improving cost/pricing environment.” Procter & Gamble’s results just hit, boasting beats in the top and bottom line and a raised sales outlook (though shares are a bit weaker in the pre-market). RBC, in a note Monday wondered whether investors would start rotating away from health care and utilities and back into staples, especially given the observation that the stocks have “reacted strongly” to results. That and the fact that buy ratings are low in the segment vs others.

Financials are teetering on a perfect split of top line sales surprises thus far, but ultimately, as usual, it will be about net interest margin and rates. Zions Bancorp missed estimates last night, but is about flat in the early going after boasting decent loan growth and net interest income figures (Fifth Third also just hit the tape and is rising early). Looking across the rates spectrum, the 2 year/10 year spread has been inching higher here over the past few days, likely providing an underlying support.

In other thematic looks, Texas Instruments and Snap Inc. report post-market, with the former a key barometer to the state of play for semiconductors, and the latter still referenced frequently as a proxy for when IPOs struggle (that and Blue Apron). The smattering of recent IPOs (LYFT, ZM, PINS) has led many of the names to trade together, and at market’s whimsy (LYFT, ZM and PINS all outperformed Monday, with only LEVI (also a recent IPO) suffering--likely at the hands of the curious late day drop in apparel names.

Turbulence

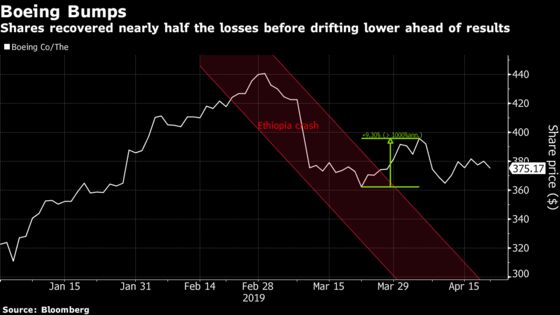

As mentioned above, Boeing was an unusual standout Monday, and it would be hard to ignore the fact that it may be related to results that are due tomorrow. Though briefly erasing much of its losses related to the 737 Max issues, shares have continued to descend. My colleague Esha Dey explains.

Boeing’s first-quarter results are going to be all about the 737 Max aircraft. That said, do not expect to get a lot of clarity from the company on the twin crashes that have idled the global fleet.

While Boeing would likely avoid divulging any detail tied to the crash investigations or the possible reason behind the incidents during the results announcement, the market will listen closely for updates on the financial impact from the fiasco and the eventual recovery.

Analysts’ estimates for first-quarter earnings, sales and free cash flow have come down significantly over the past month, and the company may also lower or temporarily revoke its outlook for the full year. According to Buckingham Research analyst Richard Safran, the planemaker could update its guidance during second-quarter results later this year.

To sum it up, watch out for comments on how long the grounding may last, discussions and deals with suppliers, details on expected production rate for second half of the year and next year, and lastly, how the company is planning and preparing to avoid such a debacle in future.

Sectors in Focus Today

- Home goods and appliance manufacturers after Whirlpool results exceeded expectations; shares are up more than 7% in the pre-market

- Electric car makers (NIO, TSLA) after Belgian materials company Umicore warned on an electric car slowdown in China

- Asset managers after Franklin Resources announced it was cutting workforce by 5%

- Oil servicer names after oil continued to rise in the wake of the Trump administration’s purported plans not to not renew Iran sanction waivers

- UBS initiated on managed care names (ANTM, CI at buy; UNH, HUM at neutral) following the selloff. Analysts cited data reinforcing fundamentals as stocks discount long term growth. Managed care, hospitals, life sciences stocks will remain in focus as S5HLTH languishes near its lows for the year, though managed care names were some of the strongest Monday. Centene’s results early had shares up more than 8% after the co. raised its forecasts

Notes From the Sell Side

Arista Networks shares have surged more than 70% since a December low, and Morgan Stanley is taking this gain as an opportunity to step back. The firm downgraded the stock to equal weight, writing that while “we still like the story,” it was waiting “until we see evidence that incremental upside drivers in campus are beginning to ramp.” The company’s campus networking business is “the primary source of upside from current levels,” but it will likely take 5-7 years for this business to reach its long-term revenue target, Morgan Stanley wrote. Arista is scheduled to report first-quarter results on May 2.

While Morgan Stanley is selling high, Guggenheim is buying low, raising its view on the U.S.-listed shares of Trivago after the stock closed at a record low on Monday. The online travel agency “seems to have been forgotten by the Street,” it wrote, adding that while “we still have some longer-dated concerns," it saw opportunity given the current stock price "and the potential for material estimate upside.” That upside is seen coming from the company’s recent focus toward profitability, adding that "ad spend was still 80% of revenue last year and that leaves a lot to potentially cut." Shares are up 4.7% before the bell.

Tick-By-Tick to Today’s Actionable Events

- Quiet period for LYFT ends; YETI lockup expiry

- Larry Kudlow speaks at National Press Club luncheon

- 7:30am -- LMT earnings

- 8:00am -- TWTR earnings call

- 8:30am -- HAS, VZ, PG, PHM, KO, UTX earnings call

- 9:00am -- Feb. FHFA House Price Index

- 10:00am -- April Richmond Fed Mfg Index

- 10:00am -- March New Home Sales

- 11:00am -LMT earnings call

- 4:01pm -- TXN earnings

- 4:05pm -- SYK earnings

- 4:10pm -- SNAP earnings

- 4:15pm -- EBAY earnings

- 4:30pm -- SYK, TXN earnings call

- 5:00pm -- EBAY, SNAP earnings call

--With assistance from Esha Dey and Ryan Vlastelica.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Brad Olesen

©2019 Bloomberg L.P.