Emerging-Market Funds Avoid Asia Even as Bargains Appear

For some emerging market funds, Asia’s beaten-down assets aren’t yet cheap enough.

(Bloomberg) -- For some emerging-market funds, Asia’s beaten-down assets aren’t yet cheap enough.

Portfolio managers aren’t rushing out their checkbooks to gain exposure to the fast-growing region, even as high-yielding currencies such as India’s rupee languish near record lows. Instead, they’re positioning for further weakness, with the U.S.-China trade war and a strong dollar expected to remain persistent themes.

“We are biasing our exposure to the dollar,” said Manu George, director of fixed income in Singapore at Schroder Investment Management Ltd., which oversees $593 billion. “We have not been constructive for a few months on Asian FX and hence we are staying put for now.”

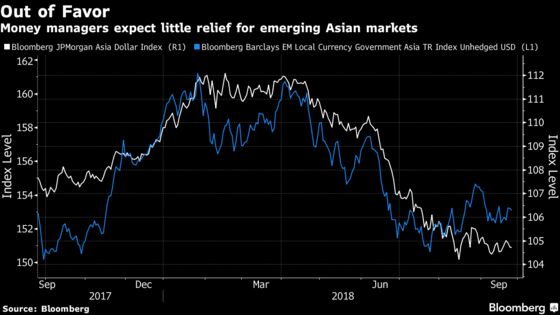

Emerging currencies and bonds extended losses this quarter as Argentina’s credit woes and financial turmoil in Turkey fueled fears of contagion. A stronger greenback is adding to the stress, with the Bloomberg Dollar Spot Index climbing to the highest in more than a year last month amid bets the Federal Reserve will keep raising U.S. interest rates.

The Indian rupee and Indonesian rupiah are leading declines in Asia, as the U.S.-China trade dispute clouds the outlook for money managers. The U.S. imposed duties on an additional $200 billion in Chinese goods on Monday, and China said negotiations to improve the situation won’t take place as long as President Donald Trump continues to threaten more tariffs.

Still, Asian policy makers are taking steps to bolster confidence. India has set targets to cut import of goods including electronics to reduce demand for dollars and support the rupee, people with knowledge of the matter said. Economists predict Bank Indonesia will tighten policy at a review Thursday, after raising rates by a total of 1.25 percentage points since the middle of May.

“The trade war has some length to go and could lead to further weakness in the Chinese renminbi,” said Alexander Zeeh, chief executive officer at S.E.A. Asset Management in Singapore. “As a result I would expect other Asian central banks to be in favor to weaken their currencies in tandem to remain relatively competitive with Chinese exports. This is the main reason I would avoid most Asian FX local-currency bonds.”

Exceptional Baht

Not everyone is negative.

“In this environment of increased emerging-market volatility, past experience shows us that Asia FX could act as a safe haven,” said Anders Faergemann, a fund manager in London at PineBridge Investments, which oversees $87 billion. “We’re still optimistic on emerging markets from a fundamental perspective.” PineBridge increased its exposure to Thailand’s baht, while it also favors other EM currencies which it says are undervalued, including the Mexican and Colombian pesos.

Nikko Asset Management Co., which manages $216 billion globally, agrees that the baht will remain resilient but advocates broader patience as the drag from the trade war outweighs the attractive valuations on Asian bonds.

“We are not increasing exposure at the moment as we think that the current weak market sentiment driven by ongoing trade tensions could linger for a while,” said Edward Ng, a fixed-income portfolio manager at Nikko Asset in Singapore. “Given the vulnerable sentiments in EM, we have been cautious in this space, particularly on countries with weak external balances.”

To contact the reporters on this story: Liau Y-Sing in Kuala Lumpur at yliau@bloomberg.net;Hooyeon Kim in Seoul at hkim592@bloomberg.net;Kartik Goyal in Mumbai at kgoyal@bloomberg.net

To contact the editors responsible for this story: Mark Cudmore at mcudmore8@bloomberg.net, ;Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds

©2018 Bloomberg L.P.