Something Alarming Happened This Week. It Matters: Taking Stock

Notes from sell Side JPMorgan is getting more cautious on home builders, noting that recovery will be “fairly tepid” in 2019.

(Bloomberg) -- Things are looking up again, with the e-minis trading higher for most of the morning, Europe’s Stoxx 600 rising almost half a percent and China bouncing huge to finish up 5.5% in the past four sessions.

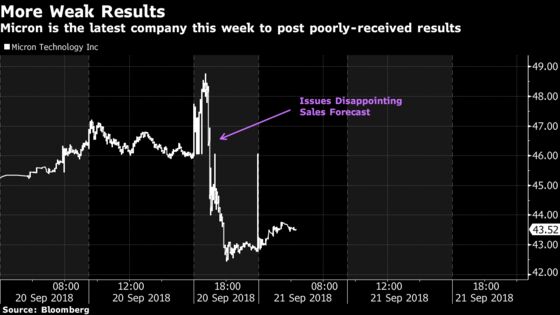

That is, if you don’t look at the semiconductors (Micron slipping >5% on a weak sales forecast), the pot stocks (everyone’s favorite Tilray dipped another ~11%), and the stock market in India, which experienced some sort of mass exodus in financial shares that drove the Sensex to its widest intraday range in over four years -- the iSHares MSCI ETF to watch over here would be INDA.

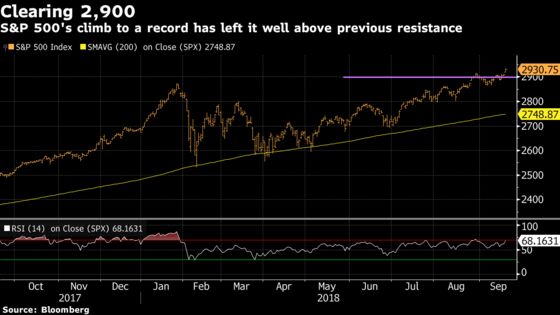

Meanwhile, the S&P cash index closed at a record high and has now gained eight of the last nine days. We’ve appeared to have cleared the previous resistance at 2,900 and it looks like we’ll have to start talking about the 3,000 level in the very near future.

As for today volatility could be heightened given the combo of a quadruple witching (last quadwitch saw S&P 500 trading volume swell 75% to 3.5 billion shares from the prior month) and the S&P 500 GICS reclassification. The latter will bring about the new Communication Services sector, a new place for FAANGs like Facebook, Alphabet, and Netflix to call home and something we’ll hear about ad nauseam once it goes into effect.

Something Alarming Happened

The disappointing guidance from Micron’s call, which led to shares nosediving in afterhours trading will likely rattle the semiconductors today, enough so to bring the SOX back towards the two moving averages that its been riding for the past couple weeks (the 50-day and the 100-day).

But what’s more interesting than the spillage in Micron, which isn’t too surprising given some of the warnings on the Street leading up to the print as well as the stock’s relative underperformance versus peers for some time now, is what a week this turned out to be for earnings as a whole -- it wasn’t a good one.

You’d think market bulls are jazzed about being so close to the end of the quarter, and thus so close to the next season of earnings, given the copious amounts of revenue and earnings beats last go around. But this week’s results weren’t even close to being on the encouraging side, even if the sample size was a small one.

Of the few and far between reports that did hit the wire, almost every single one had some sort of misstep that caused shares to careen to the downside, for example FedEx (-5.5% after earnings), General Mills (-7.6%), Red Hat (-6.5%), Cracker Barrel (-4.6%), Thor Industries (-14%), Apogee Enterprises (-12%), and several auto-related names like Copart (-13%), BorgWarner (-2.7%), and AutoZone (-2%).

You actually have to dig pretty deep to find any stocks that had a positive reaction to earnings in the past four days -- smaller-caps Steelcase and Herman Miller were the only two that came up for me -- which is pretty incredible considering the melt-up that we’re seeing in the broader tape.

What is it all mean? Clearly not a whole lot if the market is shrugging it off for new records. But it might matter a whole lot as we inch closer to the upcoming earnings season. Just don’t forget what took place this week when we get to the heart of it in a few weeks, for it may have been the first real ominous sign that third-quarter earnings weren’t of the same caliber as the unbelievable ratio of beats to misses that we saw last quarter.

On Tap for Next Week

OK, enough depressing talk.

Next week is a whole new week and perhaps it’ll be Nike that shines a light on the earnings letdown parade. The "Swoosh" is the biggest report on the schedule, and it’ll be in extra focus given the recent Kaepernick ad controversy, although not that that has mattered as the stock closed at yet another record high on Thursday.

Numbers will also be hitting from Bed Bath & Beyond, BlackBerry, Jabil, CarMax, and Conagra while investor-slash-analyst meetings from Salesforce and Intuit could make some noise.

The FOMC rate decision (nee rate hike, as the market has already decided) is the big macro event of the week, aside from another round of saber-rattling on the trade war front as the 10% tariff on $200 billion of Chinese goods goes into effect on Monday.

Sectors to stay on top of include the homebuilders with pockets of data being released mid-week (the group might get hit today on JPMorgan’s cautious note chock full of downgrades; more on this below), the alternative-energy names as a major solar conference (Solar Power International) gets underway, and anything sensitive to the move in yields, as we saw this week that the banks powered higher (BKX up >3% in two days to top of a tight six-month range) while the utilities, telecom, and REIT sectors all lagged as a reaction to the 10-year breaking back above the closely-watched 3% level.

Notes From the Sell Side

JPMorgan is getting more cautious on the homebuilders, noting that the recovery in housing will likely remain "fairly tepid" in 2019 while rising new home inventory and declining affordability should result in a slower rate of home price appreciation next year. Five builders are being downgraded in the process, including PulteGroup and MDC Holdings to underweight.

More analysts are backing up the truck on the defense stocks after the group sold off on concerns over a DoD proposal that could significantly impact payments. Goldman said the weakness was a buying opportunity yesterday afternoon and similar calls are out overnight from Cowen and Morgan Stanley, with the latter citing three reasons not to panic, including the considerable opposition from the companies that’ll limit the implementation of the proposal.

Shade continued to be thrown on Nvidia’s latest GPU, with Nomura Instinet saying they remain unconvinced on Turing ("Ray tracing and DLSS, while apparently compelling features, are today just ‘call options’ for when game developers create content that this technology can support") -- the stock was the weakest in the SOX yesterday after Morgan Stanley, a bull, said it doesn’t expect near term upside from gaming as the Turing ramp may turn out to be "a slow burn."

Evercore ISI has one-upped the two biggest Square bulls, who each have a price target of $100, by lifting its target to $101 after a conversation with management. They see the Square Cash App as a material driver to revenue and earnings over time, particularly from the continued penetration of Square Cash Card and Instant Deposit.

Raymond James initiated on the gene editing names, giving Crispr Therapeutics (-1% pre-market) its first equivalent sell rating on the Street, calling it "crispy and overcooked." They prefer Editas, which is seen emerging as the leader in the space.

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- Apple’s new iPhone XS and XS Max will start shipping

- 8:00am -- BX investor day

- 9:30am -- IPOs Eventbrite (EB), Farfetch (FTCH) will start trading after the open

- 9:45am -- Markit PMIs

- 2:00pm -- Tiger Woods tees off at Tour Championship

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.