The Junk Bond Market Looks Like a Runaway Train

The Junk Bond Market Looks Like a Runaway Train

(Bloomberg Opinion) -- Bond investors often say that “No one wants to be a forced seller.” And that makes perfect sense: If you need to sell during a rout, no matter the price, you’re going to take a big hit. But it should be equally as scary to be a forced buyer.

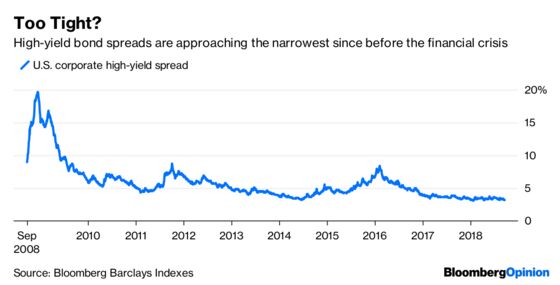

Increasingly, that’s what happening in the U.S. high-yield corporate bond market. With ample cash and little new supply to purchase, investors have pushed the average spread on junk debt down to just 3.15 percentage points, close to the narrowest since 2007, according to Bloomberg Barclays index data. As recently as 2016, that gap was more than twice as wide.

A handful of companies have benefited from this trend in recent days. Diamondback Energy Inc. received more than $2 billion of orders for a $500 million offering, allowing it to boost the size to $750 million. International Game Technology Plc and Clearway Energy Inc. were also bombarded with money, leaving investors accepting smaller yields. And a deal that funded Blackstone Group LP’s acquisition of Thomson Reuters Corp.’s financial and risk business saw more than $10 billion come pouring in for the $2.8 billion dollar-denominated portion.

It’s no secret why high-yield securities are hot. Moody’s Investors Service expects the default rate on speculative-grade debt will fall to 2.6 percent by the year-end from 3.4 percent now. Meanwhile, U.S. Treasury yields are climbing toward the highest levels in years, making bonds less vulnerable to higher interest rates more attractive. Combine that with the cash flowing in from coupon and principal payments, plus a 25 percent decline in issuance relative to last year, and it’s no surprise these deals are being gobbled up.

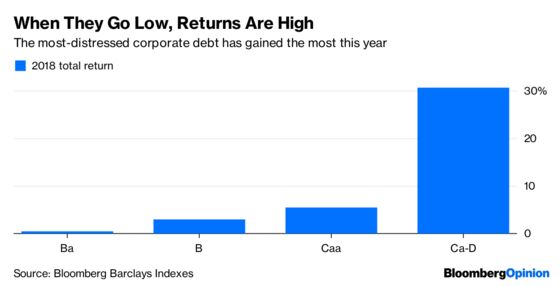

Investors aren’t complaining. The Bloomberg Barclays U.S. Corporate High Yield Bond Index has returned 2.4 percent in 2018, more than just about any other fixed-income market. And the lower the rating, the better the performance: Securities seven to nine steps below investment grade (CCC, or Caa) have gained 5.5 percent, while the most distressed debt has soared about 31 percent.

Still, it’s hard to shake the feeling that the junk-bond market is missing its brakes. This momentum-chasing happens in credit markets from time to time, of course, and high points in the economic cycle naturally encourage risk-taking. But some cooling-off may be warranted.

This week’s AkzoNobel Specialty Chemicals deal illustrates the risk of hopping aboard the runaway high-yield debt train. Investors placed more than $2.5 billion of orders for a $605 million offering to fund the company’s buyout by Carlyle Group LP. On Thursday, the yield was set at 8 percent, down from an initial whisper number of 9 percent.

But, as analysts at credit-research firm Covenant Review point out, the sale is “replete with very aggressive terms” that favor the company’s private equity owner. Yet few investors will push back. They simply can’t, given the prevailing market trends.

Even more alarming is that analysts see this relentless demand as a reason why things won’t end badly in credit markets this time around. Bloomberg News’s Katherine Doherty wrote up an analysis from Brian Reynolds, asset class strategist at Canaccord Genuity. He says distressed funds are likely to “put their money to work aggressively” in the event of another panic — keeping it brief, and avoiding the disaster of 10 years ago. Investors are far more willing to buy troubled companies’ debt than a decade ago, an example “of how credit investors are taking shadow banking to new heights,” and creating what Reynolds calls “new and innovative ways of financial engineering.”

I’m not convinced this is how things would go in bad times. It’s easy to love distressed companies now. Profits are huge, and have been for years — the high-yield index has only posted an annual loss once since the end of the recession. But that glosses over the painful 26 percent drop in 2008.

For now, it seems investors are happy to delay any reckoning. A recent Bloomberg News story chronicled how some of the biggest distressed companies have largely succeeded this year in asking investors for more time to pay off debt. Whether that works out remains to be seen. And this may not be the top for high-yield bonds. Earnings are strong, the economy is roaring, and spreads are still about 80 basis points from their all-time narrowest levels. Barring an unforeseen surge in supply or dramatic reversal in risk appetite, the rally could very well keep chugging along.

But now more than ever, investors should get picky. You hate to be a forced buyer. You hate to be a forced seller. But the absolute worst thing? Being both.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.