A Rate Hike Worked for Russia. Why Not South Africa?

(Bloomberg Opinion) -- Time to take a leaf out of Moscow’s playbook? It might be a smart move for South Africa’s central bank to follow Russia’s lead and raise interest rates on Thursday.

It would certainly be unexpected. Only three of the 19 economists in a Bloomberg survey are calling for a 25 basis point increase. There’s logic to that call.

The economy’s unexpected contraction in the first half looks like an aberration. Gross domestic product may come in at 1.3 percent for the full year, in line with the pace of 2017. And even if inflation ticks up on Wednesday to the 5.2 percent forecast, this will still lie within the central bank’s target range of 3 to 6 percent.

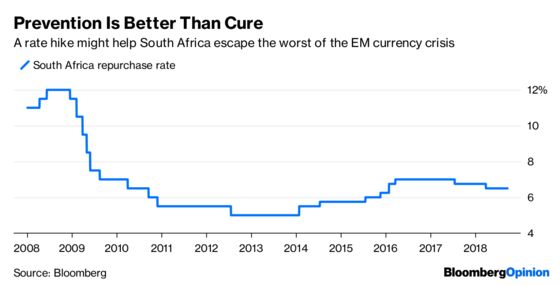

The issue is the rand. Its 16.5 percent drop against the dollar this year makes it the fourth-worst performer in emerging markets. An interest-rate hike this week could make the difference between regaining control of the currency and the start of a downward spiral on the order of the Turkish lira’s.

Confronted with a similar situation, the Central Bank of Russia confounded economists’ expectations by delivering a surprise 25 basis-point rate increase on Friday. This demonstration of the monetary authority’s determination to contain inflation at the first whiff of accelerating prices — in the face of political opposition — lent the ruble some much-needed stability.

It’s a different story for Turkey. The central bank’s 625 basis-point rate hike on Thursday also came as a surprise, not least because it arrived mere hours after President Recep Tayyip Erdogan railed against tighter policy. But though the move was the right one, the central bank’s delay has proved very costly, as I have argued. And despite the magnitude of the move the currency is still floundering.

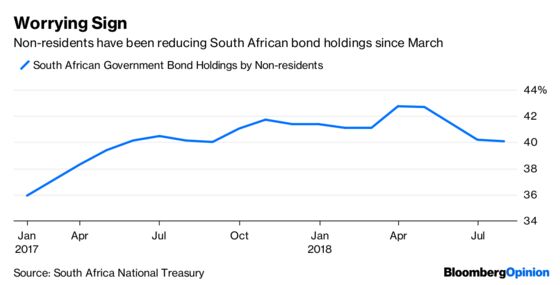

South Africa should take note. The key to the central bank’s decision lies in its bond market, or rather, who owns it.

Forty percent of government securities are held by foreigners, double the emerging market average. Unfortunately, it’s not as easy as it used to be to cover debt interest payments, as Bloomberg Intelligence’s Mark Bohlund has pointed out.

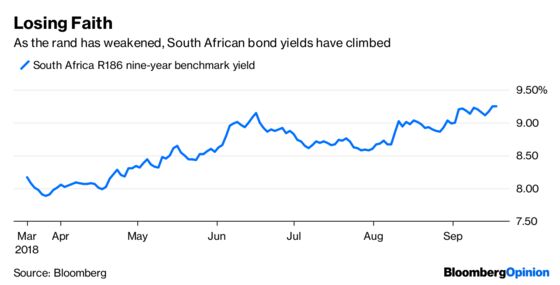

As the rand has faltered yields have risen, with the benchmark nine-year government bond now at 9.2 percent. What South Africa now owes to foreign investors far outweighs what it earns from investments abroad.

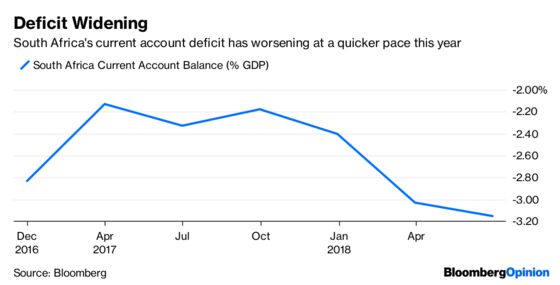

Though it reported a healthy trade surplus for most of 2017, this year has seen some worrying dips into deficit as prices of the nation’s two principal exports, gold and platinum, deteriorated, driving mining production down to a six-year low. Though the surplus is back, and a weaker rand should encourage demand for exports, it’s too small to cover the vast payments to foreigners.

This adds up to a current account deficit that’s deteriorating at a faster rate.

A weaker rand will only worsen this — and a deeper decline could spark the kind of capital flight that could turn into a serious rout.

The simplest way for the central bank to strengthen the rand and narrow the current account deficit — which it should aim at, under its financial stability mandate — would be to raise interest rates. Add to this the inflationary pressure that gets created by a weaker currency, and there’s good reason for officials to do more than a hawkish hold.

South Africa had for some time been the lodestar of emerging markets, offering relative stability and sophisticated, liquid markets. But an unfortunate combination of events have hit at the same time, and the arrival of a new president earlier in the year hasn’t seem to have done much to assuage investors’ concerns, even as Moody’s Investors Service maintained its investment-grade rating.

The country needs to try and differentiate itself from wider emerging market contagion. It may have serious problems of its own, but they are not of the magnitude of Argentina’s or Turkey’s. A proactive rate hike could make all the difference.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.