Mervyn King Still Doesn't Think British Banks Are Safe Enough

Mervyn King Still Doesn't Think British Banks Are Safe Enough

(Bloomberg) -- The U.K. banking system is stronger than it was after it almost brought the nation to its knees a decade ago, but people who oversaw the crash are still fearful of a repeat.

“The big lesson to me is that although banks today are safer than they were then, they’re not safe,” Mervyn King, governor of the Bank of England as the financial crisis broke, said in a Bloomberg Television interview. His former underling, Victoria Cleland, now one of the central bank’s top-ranking women after she was tapped to help contain the damage from Northern Rock, says the awareness of risk remains heightened.

King, Cleland and others say there’s still work to do after the crisis prompted the abandonment of the so-called light-touch, principles-based framework the U.K. boasted about in Gordon Brown’s days as finance minister. King’s recipe to prevent a re-run: ensure lenders have enough collateral in place at the central bank to justify it acting as lender of last resort, restoring liquidity to the financial system.

“It is vital to sort out the conditions under which those loans will be made in advance, to make sure that banks do have enough collateral or security to justify those loans, and that it’s big enough to let the central bank lend enough money to prevent a bank run and collapse of the system,” said King, who was succeeded by Mark Carney in 2013 and has now returned to academia.

Among regulators’ changes:

- The new U.K. framework is rules-based, designed to allow banks to fail without bringing down the system. Banks must now fund their activities with multiple times the capital employed pre-crisis, and hold easy-to-sell assets to ensure they have liquidity

- Retail and wholesale businesses have been separated

- The Bank of England handles prudential regulation for the biggest banks and insurers

- The Financial Conduct Authority is in charge of policing bad behavior

- Authorities have new powers to rein in lending and insist on more capital, as well as to decide when a firm is no longer viable and must either be shuttered or resolved

- Annual stress tests now give an early warning of weaknesses

- Lenders have “living wills” -- road maps for their own demise

For Carney -- who is among those who criticize crisis-era policy makers for having been overly concerned with the dangers of moral hazard -- major lenders still can’t be resolved without drawing on taxpayers’ funds. The governor has said many times that until the debt securities destined to restock the equity of a collapsed bank are fully in place, banks won’t be fully resolvable.

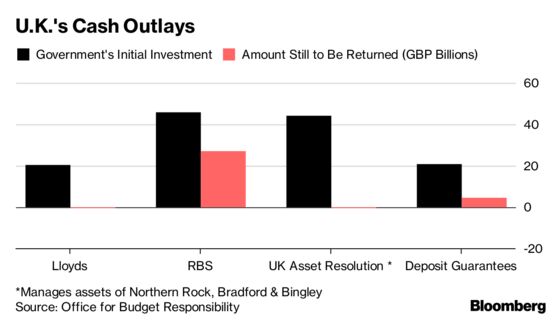

The collapsed bank that kicked off the crisis was Northern Rock, a mortgage lender that lost its access to short-term funding a year before Lehman Brothers went bust. The biggest rescue was Royal Bank of Scotland Group Plc: eventually totaling more than 45 billion pounds ($60 billion at today’s exchange rate), it was the world’s biggest bailout.

Cleland was posted to Northern Rock’s base in northern England and remembers patching together ad-hoc policy over pizza dinners to contain the damage as the bank was nationalized. Later, she was assigned to Bradford & Bingley Plc, another housing lender taken over by the state.

“The world isn’t perfect -- there’s still a lot of work going on in developing better resolution plans and bail ins, acknowledging what can go wrong,” Cleland, who is now executive director for banking, payments and financial resilience at the central bank, said in an interview. She helped set up the BOE’s Special Resolution Unit and also designed elements of the 2009 Banking Act.

“What’s been learned is that you can plan for a million things -- but there will still be something different,” Cleland said.

--With assistance from Guy Johnson.

To contact the reporters on this story: John Glover in London at johnglover@bloomberg.net;Lucy Meakin in London at lmeakin1@bloomberg.net

To contact the editors responsible for this story: Sree Vidya Bhaktavatsalam at sbhaktavatsa@bloomberg.net, Keith Campbell, Jon Menon

©2018 Bloomberg L.P.