(Bloomberg Opinion) -- It was the best of times, it was the worst of times.

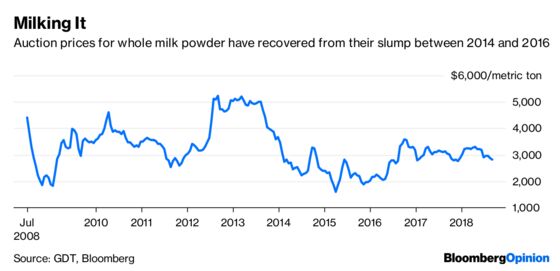

For the 10,162 farmer shareholders in Fonterra Cooperative Group Ltd., the past 12 months have been good. After a global dairy glut drove milk powder to a record low of $1,590 a metric ton in 2015, prices have been back at healthy levels for two years running. This year’s farmgate price of $6.69 per kilogram of milk solids is the best since 2014.

So why are the shares down more than 20 percent this year, and why did Fonterra – whose size and role in setting global dairy prices invites comparisons to Saudi Arabian Oil Co.’s position in the petroleum market – just post its first-ever annual loss?

The answer is the company’s awkward hybrid nature. On one hand, it’s a cooperative that seeks the best possible price for dairy products sold by the farmers who own the company.On the other hand, it wants to be the peer of dairy giants like Nestle SA and Danone SA, which make their money from buying cheap commodity milk and turning it into higher-margin branded consumer goods on the shelves of the world’s grocery stores.

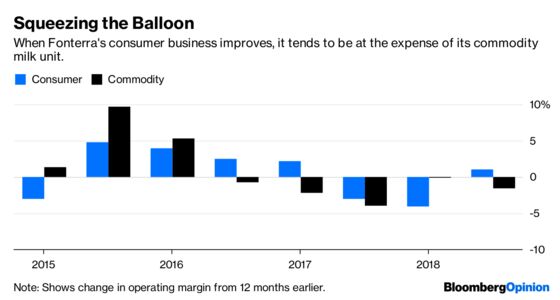

Look at the main reasons the company gave for missing its earnings forecast in annual results Thursday: strong butter prices and an increase in the farmgate milk price late in the season. That sounds like good news, until you consider that it represents costlier raw materials for the branded-products unit, with a concomitant squeeze on margins.

A better idea would be to dissolve this failed marriage and set Fonterra’s branded-products business free to operate in competitive tension with its milk cooperative.

Have a look at the performance of A2 Milk Co., based 15 minutes’ walk from Fonterra’s Auckland headquarters, to see what that could achieve. With just 180 employees next to Fonterra’s 22,358 and NZ$922 million ($605 million) of revenue against Fonterra’s NZ$20.44 billion, A2 might be considered the junior partner of the two. But over the past six months or so its market capitalization has on occasion been running ahead of its larger cousin.

It’s not hard to see why. A2 claims its products are easier to digest than conventional dairy. That’s given it some impressive marketing clout in Asia, the holy grail for the world’s dairy companies, where lactose intolerance is common. After entering the region as recently as 2013, Ebitda from its Chinese and Asian unit already came to NZ$82 million last year, about a quarter of the operating profit from Fonterra’s equivalent branded business.

That gap is likely to tighten further in the years ahead after a deal in February between the two companies that will see Fonterra work to supply A2 with more milk that suits its requirements.

No side really benefits from Fonterra as it’s currently constituted. Its farmer shareholders would like to see the company as a whole prosper, but every dollar of margin earned by the consumer business is a dollar that might otherwise belong to the farmers themselves.

Meanwhile, external investors who might be keen to spend money building up an Asia-focused global dairy brand to rival Nestle and Danone are understandably put off by the fact that Fonterra’s constitution prevents them getting the sort of management control they’d expect for their cash.

A contrite Fonterra made a vague promise on Thursday to “take stock of the business” as well as fixing underperforming units, and improving the accuracy of its forecasts. That’s to be welcomed, but the real solution must be more radical. By splitting itself up, it would allow farmers who want to stabilize their milk prices to continue investing in that while offering them an option on a separate business dedicated to selling higher-margin packaged foods.

To win back the love of investors, Fonterra must first end this unhappy marriage.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.