Four Reasons Why the Dollar Market Has the Upper Hand on Refinitiv Deal

Four Reasons Why the Dollar Market Has the Upper Hand on Refinitiv Deal

(Bloomberg) -- The jumbo financing for purchasing a majority stake in Refinitiv, Thomson Reuters’s Corp.’s financial and risk business, is already heavily slanted toward dollars and some investors say that share of the pie may grow even bigger at the cost of the euros.

Right now the plan is unchanged: the company wants to raise 9.3 billion in dollars and 3.6 billion in euros ($4.2 billion). But the deal has gained strong early momentum in the U.S. relative to Europe, driving speculation that the dollar side could be increased, either for loans and bonds, or both, according to investors reviewing the deal who asked not to be named.

The deadline for fund managers to commit to loan portion has been brought forward to this Friday, earlier than the original Sept. 17. In Europe, next week’s roadshows have been canceled but London meetings with bond investors take place through to Friday. Arrangers won’t have full clarity on demand from all quarters of the market until late this week.

Refinitiv, AkzoNobel Specialty Chemicals LBOs: Quick Look

Cross-border borrowers typically set tranche sizes based on a combination of factors that includes their revenues and the cost of funds available to them in the different markets, including the cost of hedging between currencies. In Refinitiv’s case, its U.S. operations contribute 43 percent of revenues, Europe 40 percent and Asia 17 percent, according to information provided by the company to bondholders.

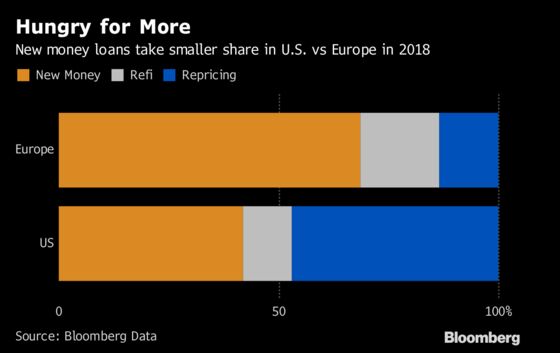

Want Some More Please

The U.S. market has seen relatively sparse leveraged debt issuance to back M&A this year. This has left buyers hungry for more, whereas in Europe they have had a feast this year, so cross-border borrowers such as Refinitiv could find a more eager bid for dollars. On top of this, the U.S. capital markets are deeper, and investors tend to be less finicky about weak covenants and aggressive structures than their European counterparts.

The European market is still deep, however, and the initially targeted roughly 2 billion euro loan tranche, although very large, should not be out of reach if the credit story and documentation stack up. Demand is driven by a long queue of CLOs wanting to price by year-end, and euro-denominated term loans may appeal to some investors that have been buying U.S. paper, due to the yield pick-up.

Wider Net

On the high-yield bond front, Refinitiv can cast its net wider among potential U.S. investors. The company is being categorized as a financial in the U.S, which is a standard part of the U.S. high-yield benchmark alongside companies classified as corporate. In Europe, financials are off-benchmark for a lot of European high-yield investors.

Bridge In

In addition to this, U.S. investors are said to have taken up more of the $5.5 billion bond bridge sold over the summer, according to fund managers. This would have given those investors that bought the bridge paper a headstart in terms of credit work, and would also mean a significant amount of the bonds were already covered as these investors roll into the deal.

Regulation

Some European investors have also pointed to MIFID II as a possible reason enabling a swifter response from the U.S. buyside. The regulations took effect on Jan. 1 and require European managers to pay for equity and fixed income research. In contrast, their U.S. counterparts will have had access to free research ahead of formal launch, improving their familiarity with the credit.

Bloomberg LP, parent company of Bloomberg News, competes with Thomson Reuters and the division that is being partially sold in providing news, data and analytics for Wall Street traders.

Some information from people familiar with the matter, who are not authorized to speak publicly and asked not to be identified. A spokesman for Blackstone Group LP, which leads a consortium buying a majority stake in Thomson Reuters’ financial terminal business, declined to comment on the currency changes.

(Sarah Husband and Ruth McGavin are leveraged finance strategists who write for Bloomberg. The observations they make are their own and are not intended as investment advice.)

--With assistance from Laura Benitez and Lisa Lee.

To contact the reporters on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net;Sarah Husband in London at shusband@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, Charles Daly

©2018 Bloomberg L.P.