Hudson's Bay Deal Brings German Department Stores Together

Hudson's Bay Deal Brings German Department Stores Together

(Bloomberg) -- Two of the most storied names in German department stores are combining in a deal orchestrated by an Austrian real estate billionaire, highlighting the pressures facing traditional retailers amid the rise of Amazon.com Inc.

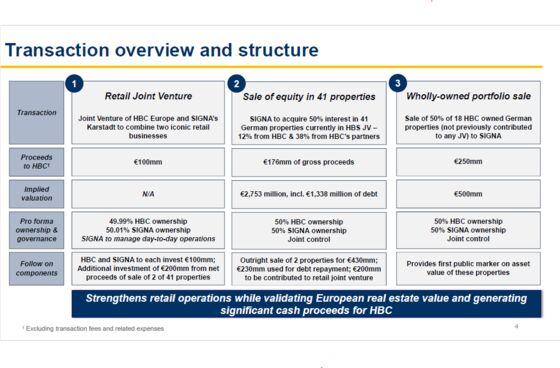

Karstadt, controlled by Rene Benko’s Signa Holding GmbH, agreed to take over Galeria Kaufhof, owned by Saks Fifth Avenue parent Hudson’s Bay Co., creating a retail company with 5.4 billion euros ($6.3 billion) in revenue. Benko has long wanted to merge the brands, having had an overture rejected as recently as February.

Signa Retail GmbH will own 50.01 percent of the venture, which Karstadt Chief Executive Officer Stephan Fanderl will lead, Hudson’s Bay said in a statement Tuesday. Each company will invest 100 million euros in the combined entity, which will also receive 200 million euros from the sale of two buildings.

In a separate transaction, affiliate Signa Prime Selection AG is buying a 50 percent stake in Hudson’s Bay’s European real estate holdings, along with Kaufhof stores in Cologne and Dusseldorf, Germany. That deal values the real estate assets at 3.3 billion euros and will generate proceeds of C$616 million ($469 million) for Hudson’s Bay, earmarked for debt repayment.

Hudson’s Bay shares rose as much as 10 percent, the most since November, to C$11.88 in Toronto trading Tuesday.

Consolidation Moves

The agreements are the latest in a series of consolidation moves by European retailers struggling to compete with Amazon and other e-commerce providers. Last month U.K. billionaire Mike Ashley’s Sports Direct International Plc agreed to buy British department-store chain House of Fraser Ltd., as questions swirl around the future of rival Debenhams Plc.

Coming only three years after Hudson’s Bay ventured into Europe, the two pacts are also the biggest moves to date by new CEO Helena Foulkes, who pledged that “everything’s on the table” as she tries to turn the company’s fortunes around. In June, she announced plans to divest flash-sale website Gilt and close 10 Lord & Taylor stores.

Tuesday’s announcement is a turnaround for Hudson’s Bay, which said in spurning the February offer from Signa that the European business and real estate assets were “critical components of our long-term strategy.”

The Canadian company’s Europe operations, which also include the Inno chain, account for more than a quarter of total revenue. But the region has been a weak spot for Hudson’s Bay, with comparable-store sales there falling in seven of the past eight quarters. Foulkes has said that the company’s eponymous stores it had opened so far in the Netherlands haven’t met expectations.

Hudson’s Bay is boosting investment in e-commerce, store renovations and new stores. It has already cut jobs and partnered with Walmart Inc. and WeWork Cos. The Toronto-based company unloaded a minority stake to a private equity firm and agreed to sell its flagship Lord & Taylor building on Fifth Avenue in Manhattan.

In a phone interview, Foulkes said she felt the hardest part of her efforts is over.

“There’s also a really big opportunity to run a much better business in North America,” she said. “This transaction will allow us to go after that opportunity.”

The real estate deal announced Tuesday helps Hudson’s Bay to meet a key demand from activist investor Jonathan Litt, who’d complained the company wasn’t making the most of its buildings’ value.

In a statement Tuesday, Litt said the deal’s terms confirm his belief that the company’s real estate is undervalued. He urged the Hudson’s Bay board to keep monetizing assets, “including selling HBC’s remaining interest in the European business, after synergies are realized, in the near future.”

Household Names

Karstadt and Kaufhof have long been household names in Germany, with either or both holding prime real estate in just about every major town. Germans flocked to the multifloor department stores for everyday needs from groceries to staples and apparel until the turn of the millennium, when the rise of discount supermarkets, monobrand stores and online shopping began to erode their all-under-one-roof concept.

Karstadt’s former owner, Arcandor AG, fell into insolvency in 2009 under the leadership of Thomas Middelhoff. The executive, known for his high-rolling lifestyle, served a prison term after misappropriating 500,000 euros of corporate funds for helicopter and private-jet trips.

Metro AG, which had earlier looked at acquiring Karstadt to combine it with its Kaufhof chain, in 2015 sold 135 Kaufhof stores in Germany and Belgium to Hudson’s Bay, beating out Signa’s Benko. He bought Karstadt in 2014 and has said the operations swung to a small profit last year.

Benko, 41, has gone from renovating rundown lofts in Innsbruck after dropping out of high school to become the biggest private real estate investor in Austria, offering everything from luxury hotels to affordable housing. Closely held Signa says it owns property worth 12 billion euros and has projects in development worth 8 billion euros.

Earlier this year, Signa agreed to take over one of Austria’s biggest furniture chains from debt-stricken Steinhoff International Holdings NV.

--With assistance from Richard Weiss, Matthias Wabl and Boris Groendahl.

To contact the reporter on this story: Sandrine Rastello in Montreal at srastello@bloomberg.net

To contact the editors responsible for this story: Anne Riley Moffat at ariley17@bloomberg.net, John J. Edwards III, Thomas Mulier

©2018 Bloomberg L.P.