Aramco Could Deploy ‘Barbarians at the Gate’ Playbook for Sabic

Aramco Could Deploy 'Barbarians at the Gate' Playbook for Sabic

(Bloomberg) -- Saudi Arabia isn’t the first place you’d look for exotically structured M&A, but as oil giant Aramco pursues the kingdom’s biggest-ever deal it could use an option first pioneered by buccaneering Wall Streeters three decades ago: a giant leveraged buyout.

Saudi Aramco is planning to buy a strategic stake worth as much as $70 billion in petrochemical firm Sabic. The oil producer could finance the acquisition the traditional way: tapping bond investors and taking bank loans, according to people familiar with the matter. Trouble is, a big global bond issue would require Aramco to reveal detailed financial results for the first time.

Within the kingdom, there’s a big debate about whether to open Aramco to outside scrutiny. Crown Prince Mohammed bin Salman has spoken in the past about the benefits of openness and pushed for an initial public offering for the company -- a plan that’s been put on hold while the Sabic deal is done. Others in government and Aramco favor keeping things secret.

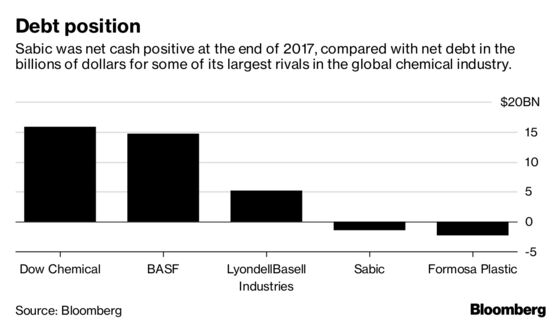

Aramco could be tempted by an alternative path that employs a private-equity style leveraged buyout and ensures Aramco’s numbers stay under wraps: using Sabic’s balance sheet to help paying for the deal. The chemical producer is virtually debt free, so has the capacity to load up on debt and pay Aramco and other shareholders a large special dividend.

"Aramco could, in theory, partially fund the stake purchase via an LBO," said Sriharsha Pappu, global head of chemicals research at HSBC Bank Plc, said in a note to clients. It would work by Aramco putting as much as $40 billion of debt "on Sabic’s balance sheet and paying a special dividend" of a similar amount to itself that would cover a large chunk of the price tag, he said.

Aramco declined to comment.

The use of leveraged buy-out became famous in the late 1980s, particularly after an acrimonious battle for the control of American conglomerate RJR Nabisco Inc. that was chronicled in the seminal business book "Barbarians at the Gate."

If the deal goes ahead as a traditional acquisition, Aramco could issue the largest ever corporate bond on its own balance sheet, beating the $49 billion that Verizon Communications Inc. raised in 2013 to buy a stake in Verizon Wireless Inc, the people said, asking not to be named discussing internal matters.

Still, using Sabic’s balance sheet rather than Aramco’s looks viable.

The Saudi Basic Industries Corp., as Sabic is formally known, is virtually debt free, with cash and equivalents of about $17 billion matching its debt. With earnings before interest, taxes and depreciation last year of nearly $14 billion, the company could probably support net debt of about $35 billion, using a net debt-to-Ebita ratio of 2.5 times, the typical limit for an investment grade company.

Sabic is currently listed on the Riyadh stock exchange, with the country’s wealth fund -- the Public Investment Fund -- controlling a 70 percent stake and the other 30 percent in the hands of minority shareholders.

The acquisition of Sabic would allow Aramco to channel to the PIF some of the billions of dollars that the sovereign wealth fund was hoping to raise from the oil giant’s IPO. In turn, the deal would cement Aramco’s own push to diversify into refining and chemicals to hedge its reliance on oil production.

Aramco hasn’t yet decided the size of the final stake it would buy from the PIF, and neither how it would finance it. Currently, it’s exploring all the options, according to a person familiar with the matter. The preferred route probably remains a conventional deal financed by the oil company’s own balance sheet and a headline-grabbing bond issue.

Simultaneously, Aramco and the PIF are in talks about the price, with parties arguing about whether Aramco should pay current prices, or the average of the last 30, 60, 180 or even 365 days. Depending on the period used to calculate the price, Aramco could end up paying between $70 and $60 billion if it buys the full stake controlled by the sovereign wealth fund.

To contact the reporter on this story: Javier Blas in London at jblas3@bloomberg.net

To contact the editors responsible for this story: Will Kennedy at wkennedy3@bloomberg.net, Helen Robertson

©2018 Bloomberg L.P.