Lululemon Beats Wall Street’s Expectations Yet Again

Lululemon Just Keeps Beating Wall Street’s Expectations

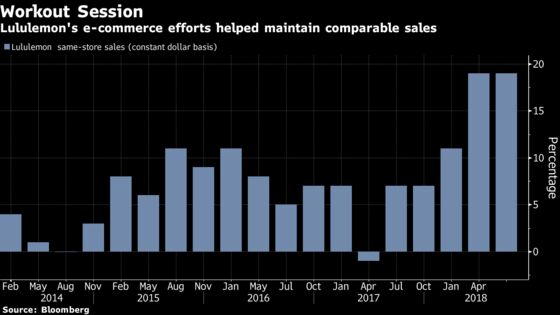

(Bloomberg) -- Lululemon Athletica Inc. investors don’t seem to mind the yoga-wear maker’s stretched valuation -- trading at a P/E ratio of about 44 times, more than twice the S&P 500’s. The Vancouver-based company has beaten all sorts of Wall Street estimates over the past two years: net sales in each of the past eight quarters; adjusted per-share earnings in six consecutive reporting periods; comparable sales on a constant currency basis in the last five quarters.

Shares are up as much as 14 percent to a record high.

The takeaway is that Lululemon is showing no signs of letting up, and the company’s 2020 net sales goal of $4 billion is certainly in reach, analysts say.

Here’s more of what they’re thinking:

Susquehanna (Sam Poser)

"Buy LULU even at this level." Increased year guidance still looks to be "conservative," according to the analyst, who raised his EPS view above the high end of the company’s new forecast range amid his projection of "material margin upside and potentially some revenue upside."

Second-quarter results "continue to prove that the combination of PEP (product, engagement, process) drives the most exceptional results within the retail industry." And Lulu is showing "no signs of becoming complacent."

Poser rates the stock positive, and raises his price target to $164 from $147.

RBC Capital (Brian Tunick)

"Lulu’s blowout" 19% constant currency comparable sales and 22 cent-EPS beat "on top of its impressive (and likely conservative)" third-quarter comparable sales forecast for low-teens growth "confirm that it remains a bright spot in a rising consumer tide."

Lululemon continues to show "top line momentum, expanding margins, scarcity of growth premium, and attractive category fundamentals."

Tunick reiterates his outperform rating, and boosts the price target to $160 from $130.

Telsey Advisory Group (Dana Telsey)

"The out-sized comp. gain contributed to a 320-basis point increase in the gross margin for the quarter to 54.8%, well head of guidance for 50-basis point expansion." In addition, product margin improved 260 basis points "from lower product costs, a favorable product mix, and lower markdowns."

"Momentum looks to continue, with multiple drivers including digital, men’s, and international." Product innovation, such as the City Sweat collection, Speed Up bra, and Embrace movement collection, should support comparable sales growth in near-term. Over the long term, investors should benefit from Lulu’s "strong cash generating model."

Telsey rates outperform and raises her price target on the shares to $170 from $145.

Bloomberg Intelligence (Poonam Goyal)

"Lululemon’s strength reinforces our view of it as a best-in-class retailer that can exceed expectations through its focus on product innovation and experience."

The company’s "impressive" 19 percent comparable sales gain and 21% operating margin point to "an architecture that allows the company to envision targets beyond those it set for 2020."

Goyal sees momentum continuing into the second half of the year, driven by "better products, innovation, robust traffic gains and better digital conversion," "with the potential to achieve the company’s 2020 goal of doubling sales, ahead of plan."

Bernstein (Jamie Merriman)

This "was a stunningly good quarter. As men discover the benefits of ABC pants and women continue to namaste, Lululemon is executing on all cylinders and is clearly continuing to resonate with the consumer."

"We are increasingly positive on Lululemon’s growth prospects over the next few years," but "from a share price perspective though, we worry that we may have missed it."

At the Aug. 30 closing price, shares were trading at 34.6x his next 12-month estimate; with 39 percent projected EPS growth this year, "it’s hard to argue that Lulu shouldn’t trade at an elevated multiple." That said, Merriman’s discounted cash flow analysis suggests a fair value price of just $122 per share.

Rating stays market perform, with a new price target of $137 from $99.

Stifel (Jim Duffy)

Results in the second quarter were "impressive and we see Lulu defining the prototype omni-channel model to which consumer brands should aspire."

The company’s 2020 objective for $4 billion in revenue and implied earnings power of $5.00 per share "is becoming more tangible," and the stock has "appropriately re-rated."

Duffy admittedly "under estimated" Lululemon’s capacity "to drive traffic and further improve gross margins." "While fundamentals remain strong and second half may hold upside potential,"

Duffy remains sidelined (hold rating) based on valuation. Price target goes to $150 from $113.

Goldman (Alexandra Walvis)

Lululemon’s "growth outperformed expectations across both stores and e-commerce, and featured an acceleration in traffic, impressive new customer acquisition, and a product range that is clearly resonating across the established women’s business as well as the more nascent men’s offer."

Walvis raises her estimates and boosts her price target to $152 from $133, which still incorporates an 85 percent/15 percent fundamental/M&A methodology. She continues with a neutral rating given belief that "valuation appropriately reflects Lulu’s growth profile."

- Lululemon has 20 buy ratings, 14 holds, and 2 sells, according to Bloomberg data. The average 12-month price target, based on 29 estimates, is $147, up from $125 a week ago, and implies 10 percent downside from the closing price on Aug. 30.

--With assistance from Mithra Wijesurendra and Riti Joshi.

To contact the reporter on this story: Janet Freund in New York at jfreund11@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Christiana Sciaudone, Lisa Wolfson

©2018 Bloomberg L.P.