ICBC Profit Rises Most Since '14 Before `Challenging' Period

ICBC's Second-Quarter Profit Rises Fastest in Four Years

(Bloomberg) -- Industrial & Commercial Bank of China Ltd. posted its fastest profit growth since September 2014 as margins and asset quality improved, but flagged challenging times ahead as the trade war with the U.S. intensifies.

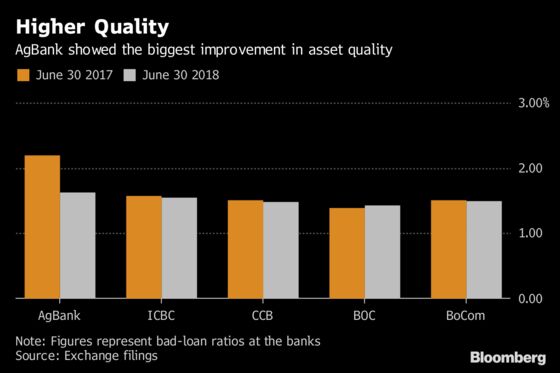

Net income at the world’s largest lender by assets rose 5.8 percent to 81.6 billion yuan ($11.9 billion) in the quarter ended June from a year earlier, according to an exchange filing Thursday, broadly in line with estimates. China’s five biggest banks have all reported profit growth of at least 5 percent for the latest quarter, and escaped the surge in bad loans that swamped smaller lenders.

While the big five benefited from President Xi Jinping’s crackdown on riskier shadow financing in the first half, analysts are cutting profit forecasts for the rest of this year as the trade war threatens to slow China’s growth. Lenders’ pricing power and capital strength may also be weakened by a renewed push for credit expansion and loosening of monetary policy, as authorities look to sustain the economy.

The second half of this year and 2019 will be challenging for ICBC amid economic uncertainties, and the bank is stress-testing companies exposed to the trade war, Chairman Yi Huiman said at a briefing in Beijing. Still, ICBC aims to maintain stable margins and asset quality, he said.

Net profit of state-owned banks would grow 5.6 percent in the second quarter, analysts led by Shujin Chen at Hua Tai Securities Ltd. wrote in a note dated Aug. 14.

Analysts surveyed by Bloomberg now predict combined profits at the big five will increase about 5 percent in 2018, less than the 8 percent forecast in March. ICBC and rivals China Construction Bank Corp., Agricultural Bank of China Ltd., Bank of China Ltd. and Bank of Communications Co. together control more than a third of China’s $40 trillion in banking assets and posted 4 percent profit growth in 2017.

Investors are pricing in this risk. ICBC declined 1.6 percent to HK$5.71 as of 9:39 a.m. in Hong Kong Friday, while the benchmark Hang Seng Index lost 1.5 percent. Shares of the big banks are trading at an average 0.7 times their estimated book value for 2018, compared with 1.1 times for HSBC Holdings Plc and 1.7 times for JPMorgan Chase & Co.

“Given valuations have dropped from a higher level, it’s more difficult for banks to tap the market for funding,” said Grace Wu, Hong Kong-based senior director at Fitch Ratings. “One of the key constraints holding back the banks from extending another round of stimulus is always the fact that there isn’t enough capital.”

ICBC plans to raise up to 100 billion yuan by selling preferred shares domestically to replenish capital, the lender said in a separate statement late Thursday, adding it may also sell more such stock overseas. ICBC in 2015 completed its first preferred share issuance, raising a total of 80 billion yuan at home and abroad.

Profit Growth

- ICBC: +5.8% to 81.6 billion yuan

- CCB: +7.2% to 73.2 billion yuan

- AgBank: +7.9% to 57.1 billion yuan

- BoC: +5.3% to 60 billion yuan

- Bocom: +5.2% to 20.7 billion yuan

Moreover, directing banks to extend loans to specific sectors hampers their prudential management, Wu said. China’s regulators have taken several steps to free up credit in the past month, and recently ordered lenders to boost support for infrastructure projects, small businesses, agriculture and exporters.

The order to step up lending comes against a backdrop of rising corporate defaults and a surge in bad debt in the second quarter, though most of the increase came from rural lenders.

ICBC plans to dispose of 220 billion yuan of soured loans this year, Yi said. Demand for loans is strong and the lender has “moderately” raised its growth target for 2018, President Gu Shu said at the briefing.

Banks | Net interest margin (June 2018 vs June 2017) | Capital adequacy ratio |

| ICBC | 2.30% vs 2.16% | 14.73% vs 14.46% |

| CCB | 2.34% vs 2.14% | 13.08% vs 13.09% |

| AgBank | 2.35% vs 2.24% | 14.77% vs 13.16% |

| BoC | 1.88% vs 1.84% | 13.78% vs 13.41% |

| Bocom | 1.41% vs 1.57% | 13.86% vs 13.86% |

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Alfred Liu in Hong Kong at aliu226@bloomberg.net;Lucille Liu in Hong Kong at xliu621@bloomberg.net;Heng Xie in Beijing at hxie34@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues, Russell Ward

©2018 Bloomberg L.P.

With assistance from Editorial Board