The Shale Dividend for Utilities Is Ending

The Shale Dividend for Utilities Is Ending

(Bloomberg Opinion) -- Forget Saudi Arabia; maybe it’s utilities Elon Musk should have been courting for his take-Tesla-private fling.

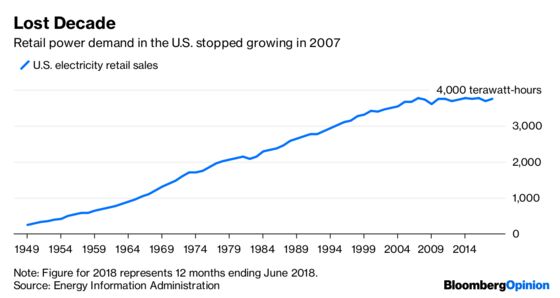

In a power-sector workshop convened by Bloomberg New Energy Finance in June, more than two-thirds of industry attendees said they think U.S. electricity demand will have peaked by 2030. Looking at the past decade, hooking up millions of vehicles to the grid may offer the best route to ensuring it hasn’t peaked already:

Given that flattened-out line, it may surprise you to learn the fixed assets of America’s investor-owned utilities actually doubled between 2006 and 2016.

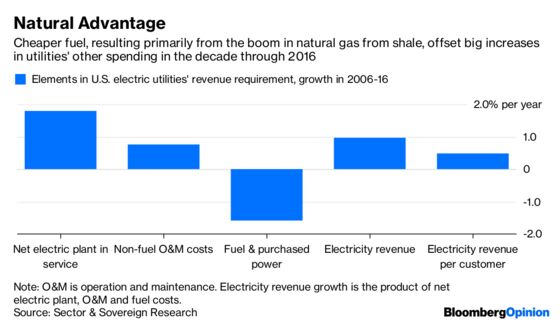

In a report published last month, Hugh Wynne and Eric Selmon of Sector & Sovereign Research looked at the apparent mismatch between stagnant electricity demand and utilities’ surging spending.

It’s worth recalling at this point that utilities recover their costs and earn a return on their investment set periodically by regulators. These costs (including their return) are spread across the kilowatt-hours sold to ratepayers (you and me, essentially).

Wynne and Selmon found that net electric plants in service for investor-owned utilities increased at 7.2 percent a year between 2006 and 2016, more than twice the level of GDP growth. Meanwhile, operation and maintenance expenses other than fuel — which also go into your bill — rose by 3 percent a year. Yet the average revenue per customer went up by only 0.5 percent a year in that time — which makes you wonder how on earth this happened:

Cheap shale gas is how it happened. Wynne and Selmon estimate roughly half of the various costs utilities need to recover in bills relates to the investment in net plant and non-fuel costs, split evenly. Combined, that means utilities would have required 2.6 percent increases in revenue per year to cover them.But the cost of fuel and purchased power weighs in at 45 percent of the pie. And this actually fell by 3.5 percent per year, largely because of cheaper natural gas pushing down generation costs, bringing the rate of growth in revenue requirement down to just 1 percent a year. Add in the impact of a growing number of customers, and there’s your 0.5 percent figure.

In short, cheap gas was a windfall that helped offset an investment spree. The industry shouldn’t expect another. Indeed, almost half the attendees at BNEF’s workshop expected fuel prices to recover and push up wholesale generation costs by 2030. That looks unlikely given the comatose state of the gas market and the growing impact of renewable energy. But costs aren’t likely to drop much either. Assuming they stay flat, SSR’s analysts project customer bills would have to rise by 2.3 percent a year over the next five years in order for utilities to recover their costs, based on current capital expenditure plans.

That doesn’t seem like a lot. But it would represent a meaningful change, with average bills rising faster than inflation after a decade of being comfortably below it. All else equal, bills that rose by about 5 percent over the course of 10 years would jump by 12 percent in five. That’s before considering what rising interest rates — also exceptionally low for the past decade — could mean for utilities’ rate-of-return requests to regulators. Incidentally, it would also make customers’ burden of bailing out struggling coal-fired and nuclear plants, as the Trump administration wants, that much harder to bear.

The attendees at BNEF’s workshop largely seem to think regulators will have their back on all this, with 64 percent agreeing to some extent that considerable increases in fixed charges would be approved between now and 2030. Large majorities also expected support for utilities playing a big role in owning and managing distributed energy resources and electric-vehicle charging infrastructure.

Utilities have inherent strengths, not least ownership of the grid. But the jury is out on all this, as suggested by the name of BNEF’s workshop: “Future of the North American Power Company.” Notably, when asked to mock up a 2023 Bloomberg Businessweek cover on the industry, all groups selected the same two images, including one indicating Amazon.com Inc. moving into the power market. Might Jeff Bezos take away from utilities (even as Elon Musk potentially gives)? It’s unclear, but disruption was clearly on everyone’s mind. (Disclosure: My wife runs a startup developing a distributed-energy platform.)

While this plays out, the challenge of balancing growth plans — many utilities target annual earnings increases of 4 to 6 percent — with pressure on customers looks set to become harder as the shale dividend fades. Besides in-house efficiency drives, mergers can offer a quicker route to savings, so consolidation may pick up further in the next few years. Keeping a lid on operating costs will help alleviate pressure on the bottom line. Perhaps just as importantly, it would appease regulators during a period of potentially far-reaching change.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.