China's Big Banks Benefit From Better Margins as Slowdown Looms

China's Big Banks Benefit From Better Margins as Slowdown Looms

(Bloomberg) -- China’s biggest banks posted stable earnings growth in the second quarter, boosted by tighter liquidity even as the broader sector struggled with government policies.

Profits at four of the five largest lenders rose at least 5 percent in the three months through June, as President Xi Jinping’s crackdown on riskier financiers pushed business to large state-connected banks. The results were broadly in line with expectations, even as a record surge in bad debt, prompted by the deleveraging effort, swamped smaller lenders.

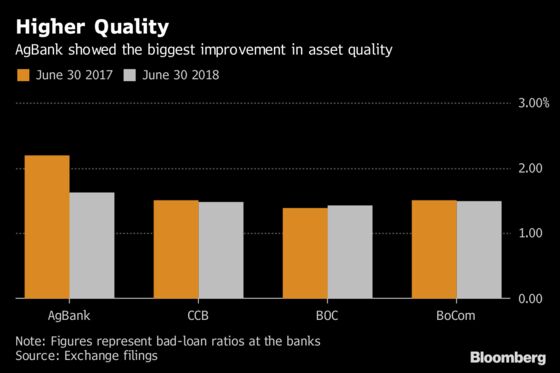

While Chinese policy makers are focusing on cutting risky debt, they are also seeking to protect economic growth as the trade war with the U.S. intensifies. Authorities have taken several steps to free up credit, including ordering the nation’s lenders to boost support for infrastructure projects and small businesses. Bad-debt ratios at the big banks are improving as they reduce exposure to industries suffering from overcapacity and boost recovery efforts.

“We think broad-based results are improving with strong pre-provision operating profit growth on the back of faster loan origination and net interest margin expansion,” Goldman Sachs Group Inc. analysts including Tian Lu wrote in a note published Wednesday.

Shares of Agricultural Bank of China Ltd. rose as much as 1.6 percent in Hong Kong on Wednesday, while Bank of China Ltd. and China Construction Bank Corp. stock dropped as much as 1.7 percent. The three banks reported earnings Tuesday. Bank of Communications Co. has seen its shares gain 3.6 percent since reporting on Thursday.

The government crackdown on risk saw the banking sector’s bad debt surge by a record in the second quarter, 80 percent of which came from small rural lenders. That could force authorities to further pull back their deleveraging campaign, which had eased in recent weeks. Policy makers are also injecting cash to help sustain the economy.

Easing the campaign may relieve some of the pressure on smaller banks, but not everyone is in favor of such an approach, said Alex Wong, director of asset management at Ample Capital Ltd.

“People don’t like this policy giving new liquidity and delaying the deleveraging process,” said Wong. “We have seen this in China over the past 10 years. Time to time they loosen and then they tighten again, so I think people are a little bit sick of it.”

Banks | Net interest margin (June 30 vs year earlier) | Capital Adequacy Ratio |

| Agbank | 2.35% vs 2.24% | 14.77% vs 13.16% |

| BOC | 1.88% vs 1.84% | 13.78% vs 13.41% |

| BoCom | 1.41% vs 1.57% | 13.86% vs 13.86% |

| CCB | 2.34% vs 2.14% | 13.08% vs 13.09% |

Bank of China’s overdue loans, a leading indicator for potential bad loans, rose 35 percent from the beginning of the year to 275 billion yuan, or 2.41 percent of total credit. China International Capital Corp. analysts cut their price target for the stock to HK$6.37 each, citing rising economic volatility and lower risk appetite from investors.

CCB said it saw a 7.2 percent increase in profit to 73.2 billion yuan. BoCom, China’s fifth-largest lender by assets, reported a 5.2 percent profit increase to 20.7 billion yuan last week.

The average nonperforming loan coverage ratio for banks including CCB and BOC reached 202 percent, above the 150 percent regulatory requirement, while the 90-day overdue loan ratio continued to decrease, the Goldman Sachs note showed. “This suggests to us that improving asset quality may help bring lower credit cost from this point on, given the likely healthier and cleaner balance sheets,” the analysts wrote.

--With assistance from Philip Glamann.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Alfred Liu in Hong Kong at aliu226@bloomberg.net;Lucille Liu in Hong Kong at xliu621@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues

©2018 Bloomberg L.P.

With assistance from Editorial Board