Leveraged Loan Buyers Are Losing Patience With Riskier Deals

Leveraged Loan Buyers Are Losing Patience With Riskier Deals

(Bloomberg) -- For much of the past year, leveraged loan investors have been pushovers. Now, they’re showing signs of pushing back.

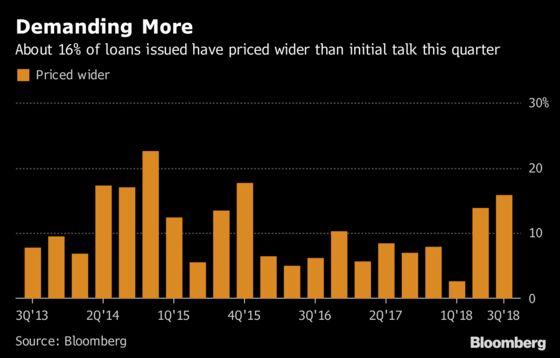

Money managers have demanded better terms on a spate of deals this week. Just today, Del Frisco Restaurant Group had to pay up when it borrowed a $310 million loan, agreeing to get just 95 cents from lenders for every dollar of debt it ultimately has to pay back, one of the steepest discounts seen this year. And underwriters have had to “flex,” or boost rates, on 15 percent of the leveraged loan deals they were syndicating to lure investors through Thursday, data compiled by Bloomberg show. That’s the worst since 2015, when oil prices were nosediving and credit markets broadly sold off as they braced for Fed tightening.

The market is still strong by many measures, but cracks may be developing in one of the best performing fixed-income markets in the U.S. this year. The pipeline of loans linked to acquisitions for syndication after the Sept. 3 Labor Day holiday is about twice the size of last year’s, with about $27 billion of loans teed up as of last week, so supply is likely to be strong.

Some money managers are waking up to the fact that credit risk is relatively high for all kinds of corporate debt now, said Mike Collins, senior investment officer at PGIM Fixed Income, which manages $717 billion.

“More speculative businesses are being financed in the loan market, high-yield bond market, and investment-grade market for that matter,” Collins said. “Markets are rightly pushing back on riskier transactions.”

With the Federal Reserve hiking rates, money managers have piled into investments like loans, which pay higher interest as central banks tighten, and into bundles of loans known as collateralized loan obligations. That demand has lifted the size of the U.S. leveraged loan market to around $1.3 trillion -- now larger than the high-yield bond market -- and spurred some companies to take out loans instead of selling bonds.

“Companies that really should be coming to the high-yield market and issuing at six, seven, eight percent yields are going to the loan market because the financing is much cheaper there,” Gershon Distenfeld, co-head of fixed income at AllianceBernstein LP, said on Bloomberg TV.

Reversing Trend?

That trend may reverse as the Fed shows signs of being closer to the end of its rate hiking process, said Matt Toms, chief investment officer of fixed income at Voya Investment Management.

“There’s been a clear preference to buy floating-rate debt where investors can,” Toms said. “As we move into 2019, that’s less obvious an impulse.”

Amid the strong demand, money managers for much of the year agreed to weaker safeguards and protections on loans to junk-rated companies, Moody’s Investors Service said in a report last week. Around 80 percent of leveraged loans are “cov-lite,” meaning they lack meaningful protections against, for example, the company’s earnings falling to low levels. In 2006-2007, that proportion would have been less than 25 percent, the report said.

What’s more, companies are funding themselves with more loans and fewer bonds, meaning that when borrowers fail, there will be fewer other investors to absorb losses, and loans will likely perform worse than they have historically. First-lien lenders will probably recover about 61 cents on the dollar from bad loans during this cycle, Moody’s estimates, compared with the historical level closer to 77 cents. For the second lien, recoveries will likely be around 14 cents, compared with the 43 cent average, Moody’s said.

“The market got heated and a little cooling off is a positive,” said Mike Terwilliger, a portfolio manager at Resource Alts. “The market is, to some extent, pulling back and being a little more rational and disciplined, and that’s a good thing.”

Top Performer

The U.S. leveraged loan market has gained 3.2 percent this year through Aug. 23, according to the S&P/LSTA Leveraged Loan Total Return Index. That’s better than high-yield bonds, Treasuries, and government-backed mortgage securities, to name a few, according to Bloomberg Barclays index data. But many of the gains for loans have come from interest payments-- prices have gained just 0.29 percent for the year, and are down this month.

To be sure, most loans are still pricing at the lower end of talk or even tighter than talk, as strong demand has allowed borrowers to offer less compensation and fewer protections. But as Aveanna Healthcare, a home health service provider, and chemical maker SI Group have recently shown, not all issuers are immune. Both had to widen pricing, twice in Aveanna’s case, and offer significant discounts to get the deals done. Representatives for both companies didn’t comment.

Other forms of corporate debt are showing signs of weakness too. A JPMorgan Chase & Co. survey found that fund managers were becoming increasingly bearish on corporate credit. High-yield bond spreads have widened almost 20 basis points since the beginning of last week.

“Valuations got a little too high and they’ve adjusted marginally, and that’s a good sign,” said PGIM’s Collins. “People are getting a little more skittish on credit risk.”

--With assistance from Faris Khan, Lara Wieczezynski, Jeannine Amodeo and Jonathan Ferro.

To contact the reporter on this story: Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Sally Bakewell

©2018 Bloomberg L.P.