(Bloomberg Opinion) -- Which are the most lucrative airline routes? The ones that fly tourists and executives between global capitals on sparkling new planes, accompanied by in-flight movies, glasses of champagne and lie-flat beds? Or the ones that hop around the boondocks on ancient turboprops with the seat stuffing coming out?

Of course it’s the latter. Every business knows that you can charge the highest prices in the most uncompetitive markets, and back-country routes typically have a single operator, often supported by government subsidies to minimize the isolation of rural populations.

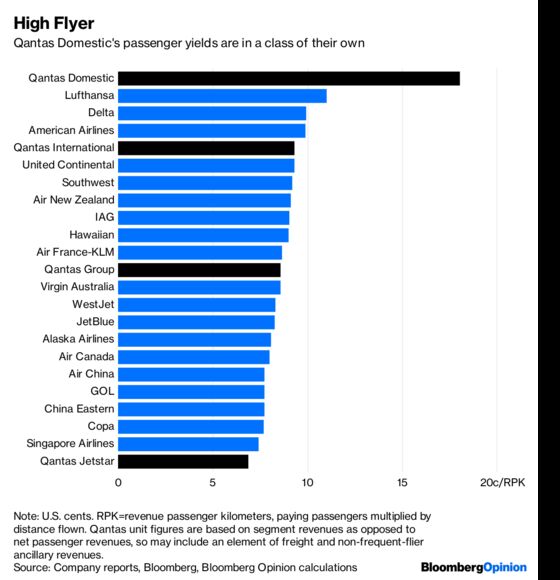

As a result, passenger yields — revenue per passenger, per kilometer flown — tend to be highest on regional airlines servicing the back of beyond. Australia’s Regional Express Holdings Ltd. has the highest yields of 121 listed airlines for which Bloomberg has data, at 40.31 cents per revenue passenger kilometer, compared to a median of 7.41 cents across the industry as a whole.

Revenue per available seat kilometer, or RASK, rose 4 percent to 8.31 Australian cents in the year through June, Qantas reported in annual results Thursday, helping to drive the company’s preferred measure of underlying profit before tax to a record A$1.6 billion ($1.2 billion).

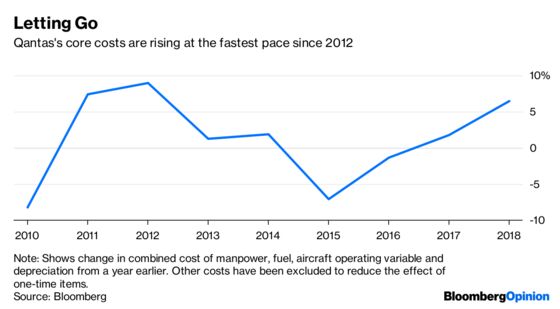

That sounds good, but it carries risks. With so much money lying around, Qantas is starting to grow fat — its core costs are up 6.4 percent from a year earlier to a four-year high. That may encourage leaner competitors in the global aviation market to move in on its territory. Investors certainly seem concerned, driving the shares down as much as 7.7 percent, the biggest intraday decline in almost two years, before they recovered to a 1.5 percent drop in afternoon trading.

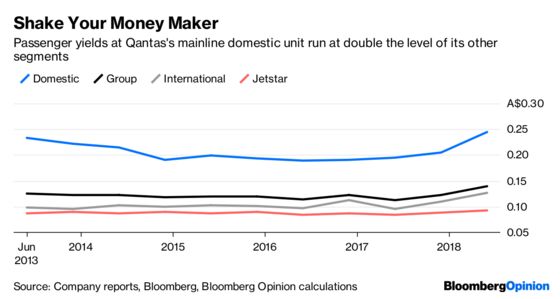

Qantas doesn’t break out passenger yield measures by unit, but it’s not hard to do a rough cut, especially as frequent-flier revenues are grouped separately. Budget arm Jetstar and Qantas International are indeed pretty competitive, with the figures coming to 9.3 Australian cents and 12.6 Australian cents, respectively, in the most recent half-year.

Qantas Domestic, however, is another story: Yield at the mainline carrier came to 24.4 Australian cents for the six-month period, better than what Delta Air Lines Inc. and American Airlines Group Inc. get on their regional affiliates and more than double that industry median of 7.41 U.S. cents.

Chief Executive Officer Alan Joyce has been helped by the disarray at his only domestic mainline competitor, Virgin Australia Holdings Ltd. The only moment in recent years when Qantas Domestic has dipped into losses came in the six months through June 2014, when Virgin’s shareholders — mainly foreign airlines that compete with Qantas on international routes — were funding the second-ranked carrier’s ambitions to break Joyce’s hold on Australia’s domestic market. Virgin hasn’t posted a full-year profit since 2012, and its domestic routes only get passenger yields of around 15 Australian cents, well below Qantas’s figure.

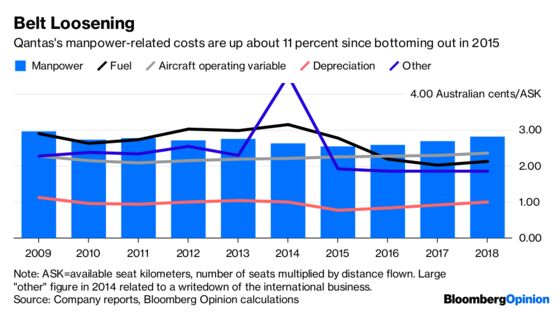

Since that campaign failed, airlines have shied away from trying to dislodge Qantas from its perch — but shareholders should be wary of getting too comfortable, especially given the way costs have been creeping up. Qantas’s manpower bill last year came to 2.8 Australian cents per available seat kilometer, the highest level since Joyce’s first year in the job in 2009 — quite a turnaround for a chief executive who made his name as a swingeing cost-cutter.

While rising fuel prices might lead competitors to be wary of investing cash, the opposite can also be the case. When your cost base is up, after all, the attractions of a high-revenue market like Australia look even greater.

There’s no formal barrier to foreign airlines setting up as domestic carriers in Australia, and capitalism has a habit of sniffing out corners of the market where monopolistic profits are being made and eroding them with competition.

For the moment, Qantas is able to print money in a way that few of its global peers can match. That may not always be the case.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.