CIBC's 3-Year Streak of Outpacing Rivals on Mortgages Ends

CIBC's 3-Year Streak of Outpacing Rivals on Mortgages Ends

(Bloomberg) -- Canadian Imperial Bank of Commerce’s prediction of a mortgage slowdown has come true.

Mortgage balances rose 2.5 percent to C$208.5 billion ($160 billion) in the fiscal third quarter from a year earlier, the Toronto-based bank said Thursday in announcing earnings that beat analysts’ estimates.

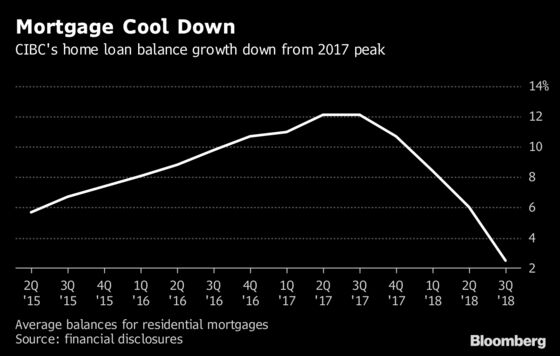

That’s the slowest in more than four years and about one-fifth the pace of a year ago. The deceleration ends CIBC’s three-year streak of outpacing Canada’s other large lenders on mortgage growth. Royal Bank of Canada said this week that mortgage balances were 5.9 percent higher than a year earlier.

CIBC executives said in May that domestic loan growth would “moderate” in the second half of the year, with Canadian banking head Christina Kramer estimating that it would fall to “low-single-digits” by year-end. Her forecast was less than Canada’s other big lenders, which have maintained “mid-single-digit" growth expectations for the year.

Despite the mortgage slowdown, CIBC posted a 16 percent jump in Canadian personal and commercial banking earnings due to a “significant” expansion of deposit margins and growth in credit cards and unsecured loans amid rising interest rates, Chief Financial Officer Kevin Glass said.

"Those would be the major offsets in terms of mortgage growth declining," Glass said in a phone interview. “Mortgages are a key product for us -- it’s very important from a client relationship perspective -- but it’s not a high margin product, so if mortgages come off it has a far smaller impact than rate increases do, for instance."

Profit Climbs

CIBC has the greatest relative exposure to Canada’s housing market, with a higher percentage of earnings coming from domestic personal and commercial banking than its bigger rivals. CIBC’s growth has cooled since it stopped expanding its team of mobile-mortgage advisers that fueled a surge in home-loan balances, with year-over-year growth peaking last year at around 12 percent. Government measures to slow Canada’s heated housing market, including tougher mortgage-qualification rules imposed in January, have also affected demand.

Net income for the quarter rose 25 percent to C$1.37 billion, or C$3.01 a share, from C$1.1 billion, or C$2.60, a year earlier, CIBC said in a statement. Adjusted profit, which excludes some items, was C$3.08 a share, compared with the C$2.93 average estimate of 14 analysts surveyed by Bloomberg. The bank increased its quarterly dividend 2.3 percent to C$1.36 a share.

Shares of CIBC rose 0.8 percent to C$122.74 at 10:41 a.m. in Toronto, its highest intraday price since Jan. 22 and the best performance in the S&P/TSX Canadian Banks Index. The stock has gained 0.2 percent this year, compared with the 2.4 percent advance of the eight-company index.

On Wednesday, Royal Bank posted third-quarter profit that beat estimates on gains in wealth management, capital markets and personal-and-commercial banking. Bank of Nova Scotia and Bank of Montreal are scheduled to report results on Aug. 28, followed by National Bank of Canada on Aug. 29 and Toronto-Dominion Bank on Aug. 30.

Here’s a summary of CIBC’s results:

- Revenue rose 11 percent to C$4.55 billion from a year earlier, while non-interest expenses increased 4.9 percent to C$2.57 billion.

- The bank set aside C$241 million for soured loans, up 15 percent from a year earlier due mainly to higher losses in its CIBC FirstCaribbean bank from the Barbados government’s debt restructuring.

- Earnings from Canadian personal and small business banking climbed 14 percent to C$639 million.

- Canadian commercial banking and wealth management profit rose 20 percent to C$350 million.

- U.S. commercial banking and wealth, including contributions from its PrivateBank takeover, were C$162 million, compared with C$41 million a year ago.

- Capital markets earnings increased 5.2 percent to C$265 million.

To contact the reporter on this story: Doug Alexander in Toronto at dalexander3@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;David Scanlan at dscanlan@bloomberg.net, Steven Crabill, Steve Dickson

©2018 Bloomberg L.P.