Bulls May Need to Wait Longer for the Big Record: Taking Stock

Bulls May Need to Wait Longer for the Big Record: Taking Stock

(Bloomberg) -- The weekly gains in the S&P 500 are in danger of being wiped out by what may become a full-scale financial meltdown in Turkey -- traders are at the edge of their seats in anticipation of Erdogan’s public address, which was scheduled to have started at ~7am.

The e-minis are off 13 handles to 2,841, Europe’s Stoxx 600 has fallen almost 1% led by weakness in the miners and a warning from fertilizer company K+S (which may spill over to Nutrien and Mosaic today), the Turkish lira plunged to a record, the iShares MSCI Turkey ETF is cratering by more than 6% in pre-market trading (inflows surged in the TUR in what may be a strategy to help facilitate previous short positions), and the VIX is back above 12 for its largest gain in nearly two weeks.

And so the S&P cash index is pointing toward an open below the late July highs and the 2,850 resistance level that some market participants have pointed to of late. That isn’t exactly an ideal setup for the bulls in the near term given the potential for a 2,800-2,850 range being established and the lack of conviction in some of the recent upticks, which could make the longs assume that a melt-up above the January record may be pushed out until liquidity returns in September.

Meanwhile, money continues to pour into the U.S. stock market, with total long-term fund flows (mutual funds and ETFs) posting their strongest week of inflows since mid-June, according to Morgan Stanley, who cites EPFR Global data. U.S. equity ETFs had more than $7.5 billion in inflows to total over $23 billion in the past six weeks and above $56 billion year-to-date.

Crowded Swings

While the broader tape has barely budged in the past few days, single-stock volatility in some of the most shorted and/or crowded names out there remains a constant, and we saw more of the same once Thursday’s closing bell rang:

- Large hedge fund ownership: Avalara, which is nearly 40% owned by hedge funds, is down ~11% on its first earnings as a public company, though the pullback shouldn’t be too surprising given shares have almost doubled since the June IPO

- Heavily shorted: The Trade Desk +21% on a solid earnings, Overstock +15% on private equity investment, Universal Display +10% on a beat, Microchip -8.2% on disappointing guidance (this could hit the semiconductors space today), and Dropbox -8.5% after COO exits (RBC upgrades to outperform, calling the COO move a likely "entrepreneurial itch" transition)

- High hedge fund ownership and short interest: Corcept Therapeutics -19% after slashing its revenue view, Sunrun -12% on an EPS miss, Redfin down ~10% on a weak forecast (management cited an unexpected drop in bookings growth in past three weeks), and Puma Biotech +18% on strong Nerlynx quarterly sales figures

On Tap Next Week

August doldrums, marked by anemic volumes and tight ranges, should be setting in next week as the amount of actionable catalysts shrivel up and vacations begin to take precedence over trading in and out of a market that is less liquid than usual.

There’ll surely be more twists and turns in the U.S.-China trade war, the debate over exorbitantly high drug prices (Trump said he would make an announcement to bring down prices "substantially"), and everyone’s favorite topic: The soap opera that is Tesla’s purported "funding secured" buyout, Elon Musk’s whereabouts (not one tweet in a day and a half), and a plot that is exponentially thickening like cement (the board will reportedly meet with financial advisers next week).

We’ll get some key economic data in the form of retail sales and industrial production for both the U.S. and China. There will also be a couple of readings on the housing front following a smattering of reports in the U.S. that have come in weaker than expected.

June-end earnings are mostly over aside from a few China-based companies like the Internet behemoth Tencent, the recent high-flying IPO of HUYA Inc., and the now-controversial GDS Holdings which is ensnared in a battle with a short seller.

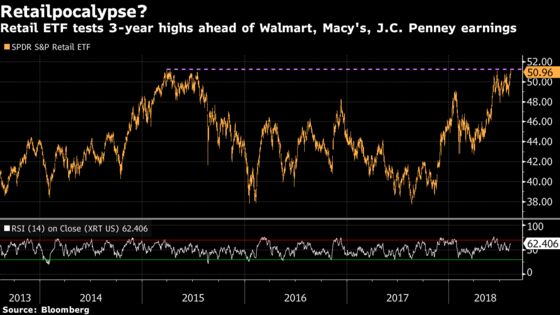

July-end earnings, on the other hand, are just getting started. We’ll hear from tech giant Cisco, a couple of chip majors in Nvidia and Applied Materials, ag machinery bellwether Deere, and a slew of consumer names like Walmart, Home Depot, Macy’s, J. C. Penney, and Nordstrom.

We’ll also be heavily dissecting the 13-F data at the Tuesday deadline to see what the new "hedge fund hotels are" and to see which funds held the FAANGs, Tesla, and other volatile stocks at the end of the second quarter.

Here are some charts on the semis, the homebuilders, and the retailers ahead of next week’s catalysts:

Notes From the Sell Side

The semiconductors remain one of the biggest debates in analyst circles. After Morgan Stanley downgraded the sector to a cautious rating yesterday, Goldman is out slashing Intel to a sell (margin concerns and manufacturing issues that "could potentially be deeper-rooted than what most think") and upgrading AMD to a neutral as it’s harder to argue the bear thesis given Intel’s struggles with 10nm process technology.

Morgan Stanley analyst Adam Jonas says a Tesla LBO doesn’t appear to be feasible, even with less than $10 billion of incremental debt, though sees an equity buyout as a potentially viable option if financed by existing holders, new strategics, divestiture of valuable captive assets (like autonomous/shared), and potentially some help from SpaceX. Separately, the bank’s European autos team is removing their underweight bias on the space and upgrading BMW and Renault in the process.

JPMorgan cuts Campbell Soup to an underweight as the firm doesn’t expect a sale at a significant premium. BofAML downgrades Fortune Brands Home to an underperform, remaining consistent with cautious theme on the building products (downgraded Jeld-Wen earlier this week). And Booking Holdings is getting punished by former cheerleaders of the stock, with three downgrades this morning (UBS, Citi, JPMorgan) and one on Thursday thanks to growth concerns tied to their recent earnings release.

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- ISS may release recommendation on ESRX/CI deal

- 7:00am -- RUTH earnings

- 8:30am -- CPI

- 12:00pm -- USDA’s WASDE grain stocks report for August

- 1:00pm -- Pompeo meets with World Bank President Jim Yong Kim

- 2:00pm -- Monthly Budget Statement

- 2:48pm -- PGA Round 2: Tiger tees off alongside Rory and Justin Thomas

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.