Asia's $184 Billion Debt Wall to Spark Buybacks, Bond Swaps

Asian borrowers in need of refinancing are expected to engage bondholders ahead of debt maturities to stave off default risks.

(Bloomberg) -- Asian borrowers faced with rising refinancing needs are expected to actively engage bondholders ahead of debt maturities as they look to stave off default risks.

That means getting investors to agree to discounted buybacks and maturity extensions, so-called liability management deals that can help firms cut funding costs. More issuers are in talks with their legal advisers to reassess their future financing arrangements and capital structures because of an uncertain primary market, according to law firm Linklaters LLP.

"Liability management actions, whether these be tender offers, exchange offers or consent solicitations, have the best chance of success if they are launched early," said James Warboys, R&I and special situation partner at Linklaters. "Timing is critical and issuers in distress can negotiate a better deal with investors than those who wait for an imminent default."

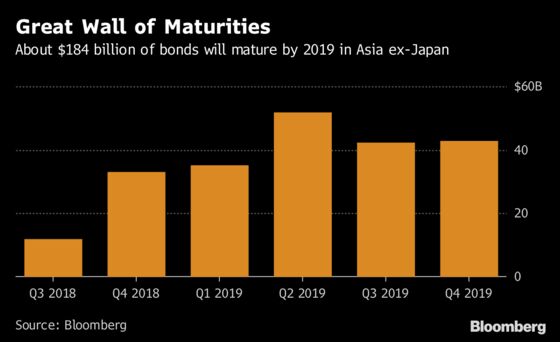

With China headed for a record year of corporate-bond defaults, Asian companies could get caught up in the turbulence ahead. About $184 billion of bonds from companies in the region excluding Japan will mature through 2019, according to data compiled by Bloomberg.

Here are some companies that have done buybacks and exchange offers recently:

- Last week, Vedanta Resources Plc accepted $522.5 million of 2019 notes and $229.8 million of 2021 bonds in a buyback tender

- Tunghsu Venus Holdings Ltd. bought back $30 million of its 2020 bonds in July

- Hydoo International Holding Ltd. issued $130 million of new notes due 2020 after an exchange offer for 2018 senior notes in May

- Kaisa Group Holdings Ltd. made on-market repurchases of $85 million senior notes due 2022 and $25 million senior notes due 2024 in May

These liability management deals benefit both issuers and investors because credit issues that are identified and addressed early on would help minimize stress and reduction of the bonds’ values, said Warboys.

Moody’s Investors Service expects more such transactions in Asia, especially from high-yield companies, rather than investment-grade ones as the latter has better access to funding.

“They may proactively manage their liabilities and refinancing to raise funds in advance,” said Ivan Chung, head of greater China credit and analysis at Moody’s. “In the past they raised funds three to six months before the redemption, but now some of them are more proactive and whenever the window opens, they try to issue to raise funding at once, albeit at the cost of negative carry.”

Chinese property and industrial issuers will likely feature in many of these deals given the massive amount of maturing debts they face in the next 12 months, according to Citigroup Inc. It also expects some from Indonesia’s high yield space.

“Liability management gives the companies a chance to extend their maturity profile especially in the current market window where it looks like issuance can tap the markets, provided they are willing to price well,” said Manjesh Verma, Hong Kong-based head of Asia credit sector specialists at Citigroup, adding “Given the uncertainty around how long the window is going to remain open, timing seems to be ripe now.”

Even so, further defaults are anticipated, said Linklater’s Warboys, particularly in China’s offshore bond market, due to widening yield spreads, tight regulatory pressures and over-leveraged companies struggling to repay the record volumes of debt maturing in a year’s time.

“To better protect themselves from these challenges, investors should pay closer attention to risk, stress-test the underlying business, cash-flows and analyze the credit protection package to understand potential options should enforcement or other debt recovery action be necessary," he said.

Investors may welcome companies’ moves to actively manage their balance sheets because that would reduce the risk of defaults and ease secondary market pricing pressure.

“We have been involved in several high-yield names that we were maybe concerned about the maturities they had in the next 12-18 months, but they have been able to refinance and extend maturities," said Alejandro Arevalo, a London-based fund manager at Jupiter Asset Management. “This is across the board. Many smart CFOs have studied the opportunities -- you take out expensive debt and pay premium to debtors and you gain on duration.”

--With assistance from Annie Lee and Allen Yan.

To contact the reporters on this story: Carrie Hong in Hong Kong at chong61@bloomberg.net;Narae Kim in Hong Kong at nkim132@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Chan Tien Hin

©2018 Bloomberg L.P.