Japan Bond Exodus Fears May Be Overblown, Regional Banks Say

Higher BOJ Yield Range Is Said to Be Too Low for Regional Banks

(Bloomberg) -- Global bond markets may have less to worry about from an all-out Japanese exodus. The yields on Japan’s benchmark bond are still too low to tempt regional lenders to switch investments back home, even after the central bank permitted a higher trading range, according to managers and traders at the companies.

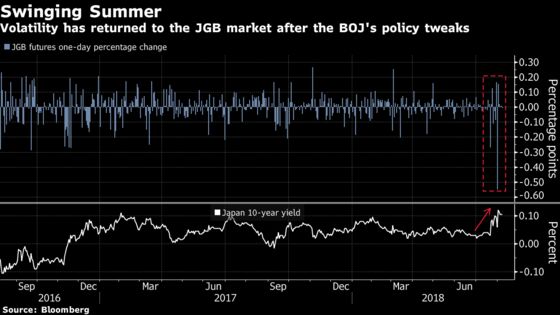

Regional lenders want to see 0.5 percent on the 10-year bond before considering a pivot back from overseas markets, according to bankers who asked not to be identified in discussing strategies. Still, the Bank of Japan’s new guidance, tolerating a yield of as high as 0.2 percent, has spurred volatility and is boosting trading profits, they said.

The BOJ’s policy tweaks, made partly to ease the pain of its stimulus for local banks, have spurred speculation that Japanese funds could shift some of the $2.4 trillion invested in overseas debt back home. Regional banks account for about a fifth of foreign securities held by the whole banking sector, or the equivalent of $80 billion, according to data from the central bank.

“A slight yield steepening is welcome but it’s too marginal to hope for a dramatic change to banks’ profitability,” said Ayako Sera, a strategist at Sumitomo Mitsui Trust Bank Ltd. in Tokyo. “A steepening by a mere few basis point after the BOJ’s decision isn’t sufficient to ease the severe situation facing them.”

Years of BOJ monetary easing have squeezed lending margins at Japanese banks and lowered income from domestic securities, with Governor Haruhiko Kuroda acknowledging the pain on July 31 when he said the BOJ would allow a wider swing in bond yields.

Regional bank holdings of government debt fell in May to their lowest since March 2008 to 20.6 trillion yen, according to BOJ data.

Here’s a summary of the comments made by regional bankers:

- The new band means a trader could buy 10-year bonds at 0.15 percent, hold it and sell when the yield dropped to the 0.08 percent level, said a banker at a lender in western Japan. This creates trading opportunities, he said

- The regional bankers that spoke to Bloomberg put the average yield on their yen debt portfolios at around 0.7 percent

- While most of the people said the yields on the 10-year bond need to be at 0.5 percent for a change in strategy, one banker at a larger lender in western Japan indicated that some initial purchases may be made at 0.3 percent

Yield Spike

Yields for the benchmark bond spiked to as high as 0.145 percent last Thursday before pulling back to the 0.11 percent level on Thursday at 2:20 p.m. in Tokyo. The 20-year was at 0.62 percent.

“In terms of helping banks make money, rising volatility is better than nothing, and as more players come and boost volatility, that will also help improve liquidity,” said Nana Otsuki, chief analyst at Monex Inc. in Tokyo. “Banks may see it easier to profit from trading when markets stabilize with a clearer vision of where yields are settling down.”

The comments by the regional bankers highlight the difference in strategies among Japanese investors and the complexities involved from any policy adjustments. While the regional lenders are more focused on shorter-duration bonds, investors are also paying attention to the trigger points for Japan’s life insurers.

Two of the nation’s largest insurers, Japan Post Insurance Co. and Nippon Life Insurance Co., said in April they will consider buying more JGBs once 30-year yields climb above 1 percent.

Ill Afford

Although regional lenders want yields to rise, they don’t want it to happen too quickly. Any significant increase would send bonds plummeting and boost unrealized losses on their holdings which they can ill afford to withstand.

According to an estimate by Japan’s Financial Service Agency, the group’s risk exposure to yen interest rates relative to capital is nearly triple that for major banks. If yields on both yen and foreign securities were to rise 50 basis points from levels as of the end of March, more than a quarter of the lenders would suffer valuation losses that exceed profits, it said.

Yields on the 10-year bond may not climb further, according to Morgan Stanley MUFG Securities Co. The benchmark will probably settle closer to 0.1 percent once market volatility settles down, partly because the BOJ owns so much of the five-to-10 year debt.

The central bank’s relentless buying of bonds has resulted in it owning about 65 percent of all outstanding five-to-10 year securities -- the highest among all the maturity zones -- squeezing supply of the notes in the market.

To contact the reporters on this story: Chikako Mogi in Tokyo at cmogi@bloomberg.net;Takako Taniguchi in Tokyo at ttaniguchi4@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2018 Bloomberg L.P.