Asia Embraces Dual-Class Shares, and Investor Activists Smolder

Asia Embraces Dual-Class Shares, and Investor Activists Smolder

(Bloomberg) -- In the battle between Asia and the U.S. for the next wave of technology listings, the shareholder advocates lost out.

After years of debate, Hong Kong and Singapore’s stock exchanges this year allowed companies to list shares with different voting rights. The fear that the next Alibaba Group Holding Ltd. or Baidu Inc. would opt for New York finally won out over concerns that dual-class shares would erode the long-term integrity of markets by allowing corporate founders to run roughshod over other investors.

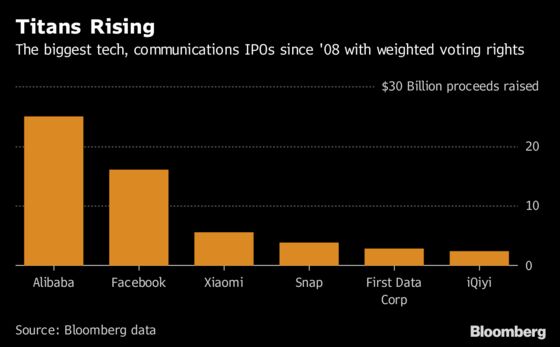

Xiaomi Corp. illustrates why. The Chinese smartphone maker raised $5.4 billion in an initial public offering in Hong Kong in July, shortly after the new rules took effect. It is now one of the most actively traded stocks on the exchange and its second-largest tech company by market value. And a raft of other tech issuers are waiting in the wings, including restaurant review and delivery giant Meituan Dianping.

It’s “the dawn of an exciting new era,” Hong Kong Exchanges & Clearing Ltd. Chief Executive Officer Charles Li said in April when announcing the adoption of dual-class shares.

While opponents to dual-class shares like Aberdeen Standard Investments are sticking to their guns, the rising clout of tech companies -- whether they use such structures or not -- underscores why there’s no turning back for Asian exchanges. Apple Inc. is now the world’s only $1 trillion market value company, and tech companies occupy the top five spots by that measure. Alibaba and Tencent Holdings Ltd., China’s most famed internet success stories, are also its most valuable companies.

“It looks like dual-class shares are here for now,” said David Smith, Asia head of corporate governance at Aberdeen. “We need to be careful, though, that investor protection is balanced with this commercial desire to attract listings.”

Dual-class shares are nothing new, and they’ve long been a favored option among tech founders who say the setup allows them to make strategic decisions that may be unpopular among investors focused on the vagaries of quarterly earnings. As Google parent Alphabet Inc. and Facebook Inc. rose to global dominance, Chinese founders took note.

Hong Kong changed its rules in April to allow dual-class listings, while Singapore approved them in June. China is finalizing rules for so-called Chinese depository receipts, a new type of security that will allow dual-class structures, to keep up in the race for tech listings.

Their decisions are bearing fruit: Hong Kong’s IPO market is in the middle of its biggest summer on record, despite a slumping benchmark stock index and some high-profile disappointments. The city will be a key beneficiary as Greater China companies with a combined value of as much as $1 trillion seek listings this year, consultancy EY estimates.

Singapore so far has had less luck attracting tech IPOs. However, Hong Kong billionaire Richard Li’s insurer FWD Group is considering listing there with dual-class shares, Bloomberg News reported last month.

These developments are getting New York’s attention. Bob McCooey, Nasdaq Inc.’s senior vice president of listings and Asia-Pacific chairman, calls Asia’s new approach “a big deal” and the NYSE Group’s Chief Operating Officer John Tuttle said Hong Kong’s new rules have affected the New York Stock Exchange “a little bit.” The unit of Intercontinental Exchange Inc. is still seeing “strong appetite” among Chinese firms for a U.S. IPO, Tuttle said.

However, corporate governance watchers repeatedly warn of what they call a race to the bottom. Outsize voting rights make it impossible to oust senior management or enforce discipline, they argue -- witness Mark Zuckerberg’s unassailable position as both chairman and chief executive officer of Facebook despite the controversy swirling around the company’s data sharing and its disappointing earnings, which last month triggered the biggest ever single-day loss for an individual stock.

“Dual-class structures generally harm investor rights. Subordinated shareholders have little, if any, say in how the company is run,” said Mark Humphery-Jenner, an associate professor of finance at the University of New South Wales in Australia. “This is especially a concern in the current climate where institutional investors are facing greater pressure to actively engage with managers and promote good corporate governance.”

Some critics are advocating for protections such as a sunset clause, which would see the founders’ extra voting rights expire after a set time period. Safeguards would prevent the formation of a “corporate royalty” that controls the future of the world’s most innovative companies, Robert Jackson, a top official at the U.S. Securities and Exchange Commission, said July 31.

For now, however, bourses realize that investors will automatically flock to high-profile IPOs, so they’re focused on bagging the next big deal rather than implementing protections, according to Humphery-Jenner.

Norges Bank Investment Management, the world’s biggest sovereign wealth fund, is an example of this tension: while it has spoken against dual-class shares, it’s one of the biggest investors in Facebook. There’s also a touch of government jockeying involved, said Lyndon Chao, head of equities at the Asia Securities Industry & Financial Markets Association.

“The U.S. and China would want their home-grown technology companies to list within their borders,” he said. “It’s not just competition for trade, it’s also competition for technology.”

--With assistance from Ben Bain and Nick Baker.

To contact the reporters on this story: Benjamin Robertson in Hong Kong at brobertson29@bloomberg.net;Andrea Tan in Singapore at atan17@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Philip Lagerkranser, Jeanette Rodrigues

©2018 Bloomberg L.P.