(Bloomberg Opinion) -- Calling the turn in industrial cycles isn't easy. It looks like investors in the beaten-down machinery sector have decided to stop trying.

Wade past the impact of the trade war and its potential collateral damage, and conditions are looking up. U.S. bellwether Caterpillar Inc. sounded an optimistic note in results last week, as did its typically cautious Japanese industrial machinery peers, which have businesses spanning the globe. It was a quick reversal from the dismal tone that alarmed investors just months ago.

But there’s a disconnect between the views of companies and of markets. Stock prices of industrial machinery makers remain down 20 to 30 percent this year, almost entirely unmoved by the latest crop of upbeat results and forecasts.

Take Komatsu Ltd., for instance, which said it expects operating income to be up around a quarter in the fiscal year ending March 2019. The maker of excavators and bulldozers maintained its fiscal-year forecast for construction and mining equipment demand, seeing a 5 to 10 percent gain across all its regions. The Tokyo-based firm’s operating profit margin was almost 15 percent in the first three months, up close to 6 percentage points from the previous quarter. At the same time, its book-to-bill ratio – a proxy for supply and demand – remained in balance.

Investor intransigence partly reflects a failure to differentiate. Mining and agricultural equipment, along with machinery for North American oil and gas, are in a better place than, say, construction machinery, as capital expenditure cycles diverge. Australian and Latin American demand for mining machinery is showing signs of a recovery, as is Indonesia.

There are more positive signs. Chinese stimulus will spur construction demand. At the same time, a longer-term boost could come from Japan, where the government is discussing manufacturing subsidies and a corporate tax cut for companies that raise wages and embrace technology.

Reflecting the optimistic mood, Hitachi Construction Machinery Co. predicted a 70 percent jump in mining revenue despite a strong yen. The segment accounts for 15 percent of the Japanese firm’s total revenue.

Caterpillar also offered a solution for the potential impact of tariffs, which it estimates at $100 million to $200 million, saying it will raise prices and further cut costs that are already at their lowest in years as a percentage of net sales. The company has already booked in orders for delivery next year.

To be sure, there’s always the risk of a sudden upset: a slowdown in China, in commodities, in global economic growth, you name it. But given the way things are moving, the view of markets is unduly dire.

These companies are trading at a 40 percent discount to their long-term price-earnings average. That puts Komatsu and Hitachi Construction at the levels they were at five years ago, when the cycle was at a trough and global growth remained in a funk.

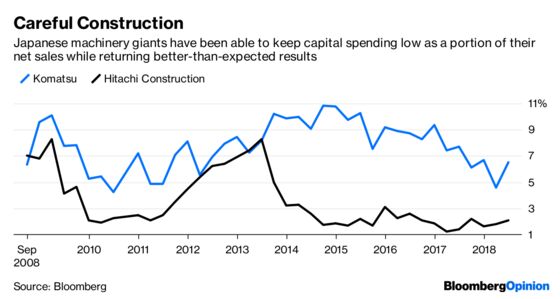

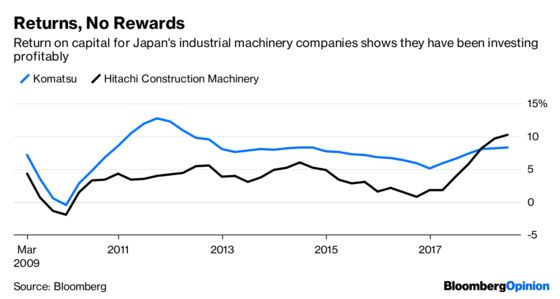

Fast forward to 2018. Returns on invested capital are on the rise, at between 6 percent and 10 percent, versus 3 percent to 7 percent five years ago. The companies are taking each dollar further, while keeping capital spending as a percentage of sales low. Their weighted average cost of capital has also fallen. Basic finance theory would tell you these firms are indeed creating value.

Yet shareholders aren’t rewarding them. Machinery giants’ ratio of enterprise value to invested capital – a measure that indicates the value investors ascribe to each dollar of capital the companies invest – is close to levels in 2009, amid the great financial crisis.

Perhaps investors know something about the cycle that isn’t showing up in economic indicators or in what companies are seeing on the ground. The other possibility is that they’ve given up too early. This improvement looks like it has some room to run.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2018 Bloomberg L.P.