That Three-Day Meltdown Might End Up Being a Blip: Taking Stock

That Three-Day Meltdown Might End Up Being a Blip: Taking Stock

(Bloomberg) -- Stock futures are little changed ahead as we hit one milestone yesterday, with Apple smashing the trillion-dollar barrier (cue the Austin Powers "one milllllllion dollars" meme), and we’re coming up on another, as we’re just fourteen trading days to go until the bull market becomes the longest of all time (3,543 days, according to BofAML).

All eyes are on the jobs number at 8:30am, where those closely watching the 10-year yield, which is hovering a couple bps below 3.00%, may gravitate more towards the wage figures (est. +0.3% m/m from June’s +0.2%) over the payrolls prints (est. +193k from June’s +213k) -- click here for a good rundown of what the Street is expecting ahead of the number.

Nothing incremental came out on the trade war front and very little else is really going on besides some earnings-related movements, though things will be quieting down on that front going forward. There was one positive semi-eco datapoint that hit yesterday: Preliminary Class 8 truck orders for July set an all-time monthly record, which could help the machinery bulls make the case that the cycle isn’t near a peak yet -- and we could see positive read-across from names like Cummins, Navistar, and Paccar today.

Global markets were mixed, with Europe trending higher -- Stoxx 600 up 0.6% on strength in tech, autos, and the banks (RBS and Credit Agricole both up multiple percentage points on earnings) -- while the Shanghai composite takes yet another leg lower, down 7 of the last 8 sessions and off almost 6% over that time frame.

As for flows, try this one on for size: Lipper data is reportedly showing that investors plowed more than $2 billion into U.S.-based equity funds, or the most since May, for the week that ended on Wednesday (this includes that three-day washout in tech). Almost $6 billion poured into ETFs while mutual funds saw outflows of nearly $4 billion -- and of those inflows, $520 million went right into the tech space.

Meanwhile, EPFR Global data shows outflows throughout, with $800 million for U.S. equity funds and $600 million for Europe, which marks the 21st straight week of redemptions for that region and a whopping $35 billion since the beginning of 2018.

One Giant Spectator Sport

We’re coming off a session that looked grim from the get-go, especially worrisome given the start below the key 2,800 support level, but the bids piled up the second the opening bell rang and the S&P 500 saw an impressive trough-to-peak reversal of ~34 handles.

You can thank the tech bulls, the Apple fanatics, and all of the traders & algos that pinned their stock and options trades to the magic number that triggered the $1 trillion milestone -- this helped lift the other FAANGs (Facebook +2.8%, Amazon +2.1%), flip several key momentum stocks that initially traded weak on earnings (Square +8.9%, Wayfair +7.5%), and lit a fire under most every other part of the tech sector. Thursday was basically one giant spectator sport with a countless amount of market participants sitting around and rooting for a thirteen-figure market cap print (shouldn’t we have all gotten hats or some other type of schwag for this?).

Perhaps the bigger question is why the market was down so much to begin with, as I imagine most traders were asking on their morning commutes when a sea of red popped up on their mobile phones. Earnings remain strong (I’d be remiss not to mention Tesla’s 16% squeeze), the Fed was a snoozer, the tariff threat was a story throughout the prior session, nothing has been set in stone in regards to the new-and-improved 25% hike (it all just seems like a negotiating tactic for now), and the talk of China retaliation was a given as this response has been like clockwork for pretty much every recent Trump threat.

Could It All Just Be a Blip?

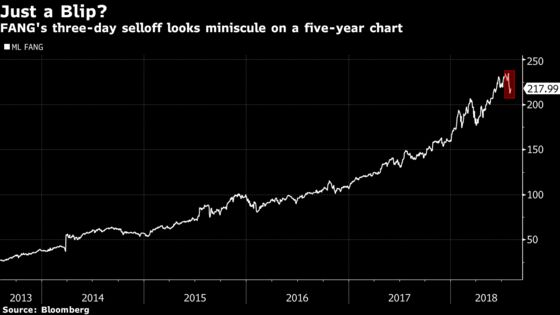

In the end, the three-day meltdown in tech that began with Facebook’s flop last week hasn’t been forgotten (just ask the panic sellers who rid their portfolio of every momentum stock), but the worries over a widespread collapse fade with every hint of resilience.

Take a look at the three charts below for a current state of affairs, with the first pointing to how teeny this correction has been for the FANG stocks when looking at the group on a long-term basis, the second showing the QQQs holding the 50-day moving average, and the third calculating a 2.5% move to the upside for the tech ETF to get us back where we were before the Facebook fiasco.

On Tap Next Week

A much quieter week is ahead of us after the recent earnings and central bank bonanza. The economic calendar is relatively light, with the end-of-week CPI likely to garner the most attention.

Trump has a scheduled vacation for most of the week, save for one rally ahead of the special election in Ohio, but odds of him taking a break from feeding the Twitter machine are slim to none, so the trade war (of words) rolls on.

Second-quarter earnings are coming to a close, with 80% percent of the S&P 500 having reported (73% beats on the top line and 85% on the bottom line). The biggest names left are media stalwarts, and coincidentally all deal stocks, like Disney, Fox, and Viacom.

We’ll also get earnings from industrial conglomerate Emerson Electric, where comments from CEO David Farr are always parsed for additional glimmers into the cycle; last quarter he gave a rebuttal to Caterpillar’s contentious "high water mark" talk, saying there were "no CAT calls in this call," sparking a bit of a relief rally in turn. Pharmacy name CVS will also get on the board, potentially shedding light on the controversy over its deal to buy health insurer Aetna.

And given the recent earnings-related spillage in tech, there will be a good amount of interest in how several Internet, social media, and momentum names scheduled to report next week will react, like Snap, Roku, Etsy, Twilio, Match Group, and Dropbox.

Lastly, we’ll get a couple catalysts for the risk-arbitrage crowd, besides the aforementioned earnings -- Rite Aid shareholder vote on the Albertsons’ merger, the Tribune/Sinclair walk date, and a deadline for a new Sky bid from Fox -- as well as a few industry conferences: JPM autos, Jefferies industrials, UBS financials, and Canaccord growth.

Notes From the Sell Side

Earnings fatigue must be setting in as most every analyst note out this morning is a flash call on the results followed by a traditional model update, but here is what’s standing out so far:

More analysts are throwing in the towel on FND, the flooring company whose stock cratered 17% yesterday post-results. BofAML removed its buy rating yesterday and so far two others, JPMorgan and Piper, have downgraded the stock to a neutral today.

Morgan Stanley slashed its price target on Blue Apron to $1.30 and its bear case to $0.50 (implies 73% downside) on disappointing guidance; shares plummeted 24% yesterday to close just shy of a record low. The bank is also reducing its rating on solar name Sunrun to an equal-weight after the stock’s 150% rally year-to-date.

JPMorgan moves KN to an underweight, the only equivalent sell on the stock out of 11 analysts out there on the name, according to Bloomberg data; cites elevated near-term expectations, increased competition from traditional semis, and the fact that it may take longer than investors think for the company to reap benefits of Intelligent Audio.

UBS was the sole bear on Synchrony Financial out of 25 analysts, but no more as the analyst has upgraded shares to a neutral to reflect positive EPS revisions and the decline in valuation, but is still waving a caution flag: "Nonetheless, we believe the operating

outlook is unclear, particularly with respect to upcoming partnership renewals."

Tick-by-Tick Guide to Today’s Actionable Events

- 7:05am -- KHC (roughly) earnings

- 7:25am -- RLGY earnings

- 7:30am -- CBOE earnings

- 8:00am -- AXL earnings

- 8:00am -- AIG earnings call

- 8:30am -- Nonfarm Payrolls, Unemployment Rate, Trade Balance

- 8:30am -- GRPN earnings

- 8:30am -- KHC, CBOE earnings calls

- 9:45am -- Markit PMIs

- 9:45am -- Larry Kudlow on Bloomberg TV

- 10:00am -- ISM Non-Manufacturing

- 10:00am -- GRPN earnings call

- 12:00pm -- DISH earnings call

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.