MetLife Gets More Cautious About High-Yield Credit, Muni Markets

MetLife Gets More Cautious About High-Yield Credit, Muni Markets

(Bloomberg) -- MetLife Inc. is becoming wary of high-yield credit and debt sold by cities and states with pension shortfalls.

“While we do not believe a downturn is imminent, we are keeping a close eye on the evolving credit market,” Chief Executive Officer Steven Kandarian said Thursday on a conference call discussing second-quarter results. “We are more cautious on general obligation bonds of states and municipalities with large unfunded pension obligations as well as certain parts of the high-yield market.”

MetLife, which oversees more than $430 billion in investments, is “neutral” on U.S. investment-grade bonds and municipal bonds with dedicated revenue streams, Kandarian said.

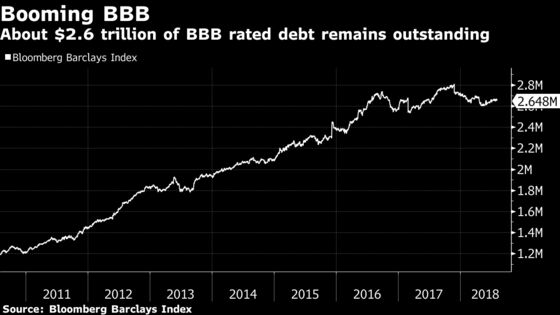

Investment managers have been trying to gauge where the U.S. stands in the credit cycle and some, including Guggenheim Partners’ Scott Minerd, have said the country could be heading toward a recession because of brewing trade tensions. Kandarian said that while economic growth is still “strong,” he pointed to the surge in BBB rated corporate debt and “aggressive” issuance in the syndicated-loan market. About $2.6 trillion of BBB debt is outstanding, more than triple what it was a decade ago, according to Bloomberg Barclays index data.

Kandarian, who was the insurer’s investment chief before being named CEO in 2011, also said MetLife is scrutinizing the credit cycle even more carefully as dwindling liquidity makes it tougher to find a quick exit. Investment managers have been lamenting the lack of liquidity, which can make it harder to find a buyer or seller of certain securities without drastically moving the price.

Kandarian said asset classes including private-placement credits and agricultural loans still offer opportunity, and Chief Investment Officer Steven Goulart stressed that the life insurer wasn’t “sounding any alarm bells.”

“We’re investing billions of dollars a quarter and we’re still finding sound, attractive investment alternatives,” Goulart said. “It’s just that market conditions remain tight, market structure is different than it was years ago, so we’re spending more time just thinking about what happens in the next downturn and how do we position ourselves when we think it’s coming.”

--With assistance from Molly Smith.

To contact the reporter on this story: Katherine Chiglinsky in New York at kchiglinsky@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Steve Dickson, Steven Crabill

©2018 Bloomberg L.P.