Puerto Rico Power Utility Bonds Soar on Restructuring Deal

Puerto Rico Power Utility Bonds Soar on Restructuring Deal

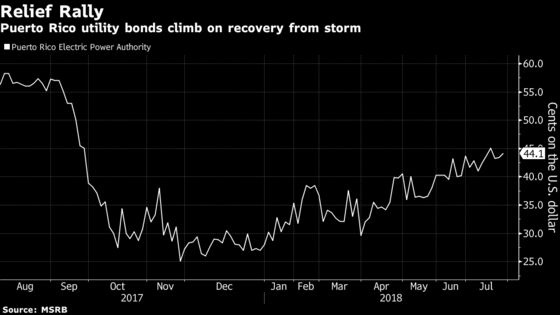

(Bloomberg) -- The Puerto Rico electric company’s bonds surged after it struck a preliminary agreement with bondholders to restructure its crippling debts, marking a major advance in the government-owned utility’s efforts to emerge from bankruptcy.

The pact -- reached by the island’s government, the territory’s federal oversight board and a key group of investors -- would slash the debt service bills of the Puerto Rico Electric Power Authority more deeply than an agreement the board rejected a year ago. The board said in a statement Monday that it’s working to finalize the deal for the power company known as Prepa.

The company’s bonds were the most actively traded municipal securities Tuesday, when investors pushed up the price of some of them by nearly 40 percent. Debt due in 2040 jumped to an average of 60.2 cents on the dollar from 43.4 cents Monday, according to data compiled by Bloomberg.

Reducing the utility’s $9 billion of debt may push the utility closer to privatization because investors would be cautious about lending needed money to the company if it continues to be run entirely by a government that steered it into collapse, said Matt Fabian, partner at Municipal Market Analytics. Puerto Rico is seeking to sell some of the utility’s assets or enter into long-term concession agreements with private operators.

“The board likes this deal because it’s going to force the issue of privatizing Prepa,” Fabian said. “Investors will always be more careful in lending a Prepa successor money.”

The step marks a major stride toward resolving years of negotiations with creditors of the territory’s electric company, which was heavily battered by Hurricane Maria last year and has been struggling with management turmoil. While the company had previously struck a deal with creditors, it was rejected over a year ago by the oversight board because of concerns it failed to do enough to modernize the utility and lower residents’ costs.

The agreement "is an important milestone and a big step forward towards Prepa’s debt restructuring process, which will support the privatization and transformation of Prepa into a modern, world-class utility,” Jose Carrion, the chairman of the oversight board said in the statement. “We are hopeful that the terms and financial concessions agreed to with this group of Prepa bondholders can lead to a fair consensual transaction that adjusts their ultimate level of recoveries with the success of the utility."

The latest agreement would require bondholders to exchange their debt for two new classes of securities at a rate of 77.5 cents on the dollar, well above where the securities had been trading.

They would receive one type, which matures in about 40 years and pays 5.25 percent interest, at an exchange rate of 67.5 cents on the dollar. The second -- so-called growth bonds that are due in 45 years and whose payments are pegged to the island’s turnaround -- would be exchanged at 10 cents on the dollar. The deal that was rejected by the board would have given investors 85 cents.

Prepa is still negotiating with other creditors, including bond insurers. The agreement announced Monday included Knighthead Capital Management, Franklin Advisers, BlueMountain Capital Management, OppenheimerFunds, Silver Point Capital, Angelo, Gordon & Co. and Marathon Asset Management, according to a filing with the Municipal Securities Rulemaking Board. The bankruptcy court would also weigh in on any restructuring deal.

The utility still needs to persuade other parties to agree to the plan and it continues to face the challenge of rebuilding an electrical grid that was destroyed by Hurricane Maria. That led to some skepticism about the degree of Tuesday’s rally, which followed a run up in the price of the securities this year amid optimism about Puerto Rico’s recovery from the hurricane and progress in the island government’s own bankruptcy process.

“There doesn’t seem to be a long-term solution of addressing how to provide a stable and reliable electrical grid to the island and who is going to pay for that,” said Dora Lee, an analyst at Belle Haven Investments, which manages $7.4 billion of municipal debt, including insured Puerto Rico securities.

Prepa’s tentative deal has also boosted prices on some Puerto Rico bonds. General obligation debt that’s due in 2035 traded Tuesday at an average price of 39.8 cents on the dollar, up from 38.4 cents on Monday.

“Prepa has always been seen as the credit to reach the finish line first in the bankruptcy puzzle,” Lee said. “The closer that Prepa is perceived at reaching its conclusion, the other investors also see their own finish lines coming closer.”

To contact the reporter on this story: Michelle Kaske in New York at mkaske@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, William Selway, Michael B. Marois

©2018 Bloomberg L.P.