Pakistan Woes Too Deep to Make Rupee Jump More Than Fleeting

Pakistan Woes Too Deep to Make Rupee Bounce More Than Fleeting

(Bloomberg) -- Don’t be fooled -- the Pakistani rupee’s biggest jump in a decade Monday was probably a flash in the pan.

The South Asian nation’s finances remain dire and the rupee is likely to start weakening again soon, according to Edwin Gutierrez, the London-based head of emerging-market sovereign debt at Aberdeen Standard Investments.

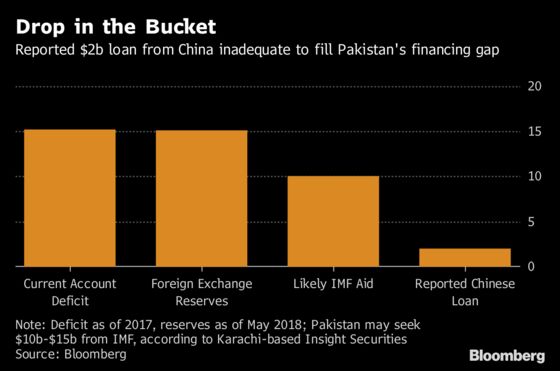

The currency climbed 0.7 percent to 124.188 per dollar at the close in Karachi, according to the central bank. The rupee advanced more than 2 percent Monday on press reports of a $2 billion loan from China. Yet longer term, the incoming government of Imran Khan may have to seek a bailout from the International Monetary Fund to stave off an economic crisis, and those funds may come at the cost of a weaker rupee.

“The currency needs to adjust given the current-account deficit and the fact that they are bleeding FX reserves,” Gutierrez said. “Indeed, an IMF deal might look like the one that they recently struck with Argentina which strongly encouraged letting the currency go.”

The Argentine peso slumped to a new low in June, even after the country reached a record $50 billion agreement with the IMF just weeks earlier. By contrast, Karachi-based brokerage Insight Securities predicts Pakistan is likely to seek $10 billion to $15 billion from the multi-lateral lender, a sum that may not be enough to restore market confidence.

Pakistan’s foreign reserves fell to $15.1 billion in May from a peak of $24 billion in 2016 following a current-account deficit of $15.2 billion last year. As the central bank attempts to stem the flow, policy makers have devalued the currency four times since December.

All of that comes against a global backdrop of higher oil prices, trade war tensions and an emerging-market sell-off.

Even before the rally, Eaton Vance Corp. had expected the rupee to weaken by another 10 percent to 15 percent before it would be “more fairly valued,” said Eric Stein, a Boston-based co-director of global income at the firm. The money manager, which oversees $444 billion, is no longer invested in the country’s assets.

“You could see a short-term boost in assets with the new government and IMF money, sure, but we don’t think it’s a good long-term investment thesis given our view that the fundamentals are weak,” Stein said. “Effectively you would be buying assets just hoping for the IMF to save the day, which can sometimes be an effective strategy, but not one we would be pursuing as of now.”

--With assistance from George Lei and Faseeh Mangi.

To contact the reporter on this story: Netty Ismail in Dubai at nismail3@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, ;Rita Nazareth at rnazareth@bloomberg.net, Philip Sanders, Alec D.B. McCabe

©2018 Bloomberg L.P.