This Might Be the Worst Time for a Trump Trade War

(Bloomberg Opinion) -- Donald Trump has proclaimed that now is the greatest time (in the history of times, surely) for a trade war. It’s a sentiment shared by even some of his critics.

Trump’s reasoning for his great trade war timing seems to be that stocks are up since he was elected, which shows once again how much his policy decisions and view of the economy are market-driven. “You know the expression, ‘We’re playing with the bank’s money,’ right?” Trump told CNBC’s Joe Kernen. “We’re up almost 40 percent.”

Put aside the fact that neither Kernen nor anyone else knows that expression. The correct saying comes from gambling, not finance, and it’s “playing with the house’s money.” It refers to being willing to risk your winnings, because at worst you could end up back at even.

The bigger problem is that Trump doesn’t seem to understand who has collected the gains in the current recovery in general and more specifically in the nearly two years since has was elected. Even more important, Trump doesn’t understand who has the most to lose if his trade war goes wrong. (He does seem to recognize that some sort of deal would be better than tariff walls being erected around the world. On Wednesday, Trump reached a deal with the European Commission President Jean-Claude Juncker to ease trade tensions and put tariffs on car imports, a chief battleground, on hold. Still, that is a skirmish on a second front compared with the trade war’s main theater — China.)

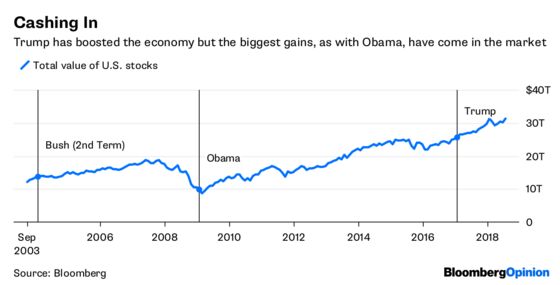

The stock market has added $7.5 trillion in value since Trump was elected and about $24 trillion since the bottom of the market in 2009. But that wealth is not spread equally. Only about half of Americans own stocks, and most don’t own a lot. A study late last year from New York University economist Edward Wolff found that the 10 percent of Americans own 84 percent of the wealth in the stock market, up from 77 percent in 2001.

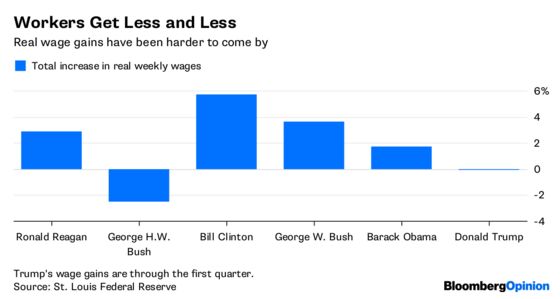

Americans who get most of their wealth and income from their paychecks most likely don’t feel as if they’re playing with anybody else’s money. In fact, they may feel like someone else is playing with money that has been promised to them, especially after the tax cuts. Real wages, after inflation, are up less than 1 percent since Trump was elected. That’s underwhelming when you realize how much of a hole workers are in. Since 2006, real wages were down 7.7 percent through the first quarter.

And while it is still too early to condemn the tax cuts as solely a boost for stock buybacks, the evidence so far is not good. Real wages appear to have dropped in the second quarter. Still, much of that has to do with a rise in gasoline prices, which is most likely temporary. Get past that, and growth in real wages could pick up steam by the end of this year as long as this recovery continues. At least that was the case before the threat of a trade war. Instead, the Tax Foundation expects the tariffs that have already been enacted could cut wage growth by about 0.33 percent, nearly half the expected increase in real wages, excluding the jump in gas prices. The Tax Policy Institute also estimated that the tariffs could cut employment growth by nearly 400,000 jobs. The result is workers will need an even longer expansion to come out of the recovery ahead.

“Does Trump know anyone who is going to give their stock market gains to people who lose their jobs in a trade war?” asked Dean Baker, a liberal economist at the Center for Economic and Policy Research. “That’s just nuts.”

Baker argues the best time for a trade war, like stimulus, may in fact be when a country is in the depths of a recession, when a boost to domestic job growth is needed at all costs. Instead, when inflation is already rising — and the fear of inflation is way up — tariffs are only likely to put more upward pressure on prices. That will cause the Federal Reserve to be more aggressive with interest rates, which more than anything else could cut off the recovery and pay gains faster than anything else. That’s a big gamble with other people’s money, especially when you don’t understand the game.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.