Health Insurance Startups Bet It’s Time for a Nineties Revival

Health Insurance Startups Bet It’s Time for a Nineties Revival

(Bloomberg) -- Nineties throwbacks have swept through music, television and fashion. Some startups want to bring a bit of that vintage feel to your workplace health insurance plan.

Health maintenance organizations drove down costs but were painted as villains in that decade for limiting patient choice, rationing care and leaving consumers to grapple with high bills for out-of-network services. But some features of the plans are regaining currency. Companies reviving the model say that new technology and better customer service will help avoid the mistakes of the past.

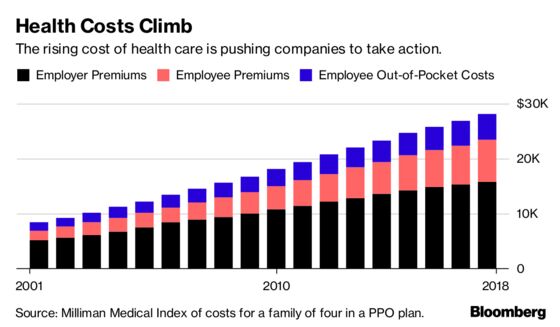

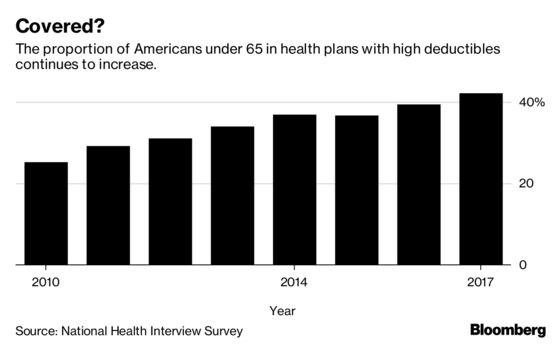

Rising health-care costs and dissatisfaction with high-deductible plans that ask workers to shoulder more of the burden are pushing employers to consider new ways of controlling spending—and to rethink the trade-offs they’re willing to make to save money.

Medical costs have increased roughly 6 percent a year for the past half-decade, according to PwC’s Health Research Institute, outpacing U.S. economic growth and eroding workers’ wage gains. Some employers, such as Amazon.com Inc., Berkshire Hathaway Inc. and JPMorgan Chase & Co.—wary of asking workers to pay even more—are trying to rebuild their health programs.

Barry Rose, superintendent of the Cumberland School District in northern Wisconsin, went shopping recently for a new health plan for the district’s 290 employees and family members after its annual coverage costs threatened to top $2 million.

“How do we provide quality, affordable and usable health care for employees,” said Rose. “I can’t keep taking money out of their paychecks to spend on health insurance.”

The company he picked, called Bind, is part of a new generation of health plans putting a tech-savvy spin on cost controls pioneered by HMOs.

Bind, started in 2016, ditches deductibles in favor of fixed copays that consumers can look up on a mobile app or online before heading to the doctor. Another upstart, Centivo, founded in 2017, uses rewards and penalties to nudge workers to get most of their care and referrals for specialists from primary-care doctors.

For many years, employers offered health plans that paid the bills when workers went to see just about any doctor, imposing few limits on care. The companies themselves usually paid much or all of the premiums.

Confronted with rising costs in the 1990s, many employers switched to HMOs or other forms of what became known as managed care. The switch worked, helping hold health costs down for much of the decade.

Soon, however, consumer and physician opposition grew amid horror stories of mothers pushed out of the hospital soon after childbirth, or patients denied cancer treatments. States and the federal government passed laws to protect consumers, and, in 1997, then-President Bill Clinton appointed a panel to create a health consumers’ Bill of Rights.

“The causes of the backlash are much deeper than the specific irritations or grievances we hear about,” Alain Enthoven, the Stanford health economist who helped pioneer the idea of managed care, said in a 1999 lecture. “They are first, that the large insured employed American middle class rejects the very idea of limits on health care because they don’t see themselves as paying for the cost.”

Workers would soon bear the cost, though. By the end of the decade, employers had moved away from these limited health plans. In their wake, costs skyrocketed, giving rise to a new cost-containment tool: high deductibles.

Centivo co-founder Ashok Subramanian spent the past decade trying to figure out how to offer better health insurance at work. His first startup, Liazon, helped workers pick from a big menu of coverage options. He sold it for some $215 million to Towers Watson in 2013, but he said it didn’t fix the bigger problem: Workers had lots of options, but none of them were very good.

“Yes, we were increasing choice, yes we were enabling personalization, but the choices themselves were not that good,” Subramanian said in an interview. “The choices themselves were predicated on a system in which the fundamental incentives in health care are broken.”

Tony Miller, Bind’s founder, helped give rise to health plans with high out-of-pocket costs. He sold a company called Definity Health that combined health plans with savings accounts to UnitedHealth Group Inc. for $300 million in 2004. He now says high-deductible plans failed to deliver on their promises.

“There’s a fever pitch of frustration at employers,” he said. “They’re tired of using the same levers that they’ve been using for the past 20 years.”

UnitedHealth, the biggest U.S. health insurer, helped create Bind with Miller’s venture capital firm and is an investor in the company, which has raised a total of $82 million. Bind is also using UnitedHealth’s network of doctors and hospitals as well as some of its technology.

Centivo has raised $34 million from investors including Bain Capital Ventures.

Centivo and Bind both promise to reduce costs for patients and employers while making it easier to find doctors and check coverage. They say they’ll reduce costs by making sure patients get the care they need, keeping them healthy and avoiding emergencies or unnecessary treatment.

In most cases, workers who follow the rules of Centivo’s plans won’t face a deductible. When signing up, employees pick a primary-care doctor, who’s responsible for managing their care and making decisions on whether they need to see a specialist. Care provided or directed by that primary physician is free, as is some treatment for chronic diseases such as diabetes, depending on how employers choose to set up the coverage.

The goal is to ensure workers get the care they need, while avoiding low-value treatments. Those who go to an emergency department in cases that aren’t true emergencies, for example, could face high costs.

“The big question is: Is the market ready for it?” said Mike Turpin, who advises employers on their health benefits as an executive vice president at USI Insurance Services. “The American consumer just has it built into their head that access equals quality.”

Bind bundles its coverage so consumers don’t get billed for lots of charges for services that are part of the same treatment. In Rose’s district, the copay for an emergency room visit is $250, while the cost of a hospital stay is capped at $1,000. Office visits are $35; preventive care is free.

Bind also offers what it calls on-demand insurance. Coverage for planned procedures such as knee surgery, tonsil removal or bariatric surgery must be purchased before the operation. That gives Bind a chance to push customers toward a menu of lower-cost alternatives or cheaper providers.

A patient who looks up knee arthroscopy, for instance, would also be offered physical therapy. The patient’s cost for the surgery ranges from $800 at an outpatient center to more than $6,000, in an example used by Miller. Surgeries in hospitals are typically more costly. Bind also charges more for providers who tend to be less efficient or have worse outcomes.

The ability to view costs upfront is part of what appealed to Rose, the Wisconsin superintendent. “Each of my employees knows exactly what they’re paying for, and they have choice in it,” he said.

Rose said the switch to Bind will save his district several hundred thousand dollars, depending on how much health care his workers need over the next year.

Lawton R. Burns, director of the Wharton Center for Health Management and Economics at the University of Pennsylvania, recently authored a paper with his colleague Mark Pauly arguing that it’s probably impossible to simultaneously improve quality, lower costs and achieve better health outcomes. The ideas now being pushed forward, he writes, are similar to ideas tested in the 1990s.

“It’s deja vu all over again,” he said. “It’s not clear to me, this is just me talking, that people have learned the lessons of the 1990s.”

To contact the editor responsible for this story: Drew Armstrong at darmstrong17@bloomberg.net, Timothy Annett

©2018 Bloomberg L.P.