Trump’s Tweets Aren’t Expected to Hold Down the Dollar

Trump’s Tweets Aren't Expected to Hold Down the Dollar

(Bloomberg) -- When it comes to the dollar and President Donald Trump’s signals that he’d prefer it to be weaker, as the Rolling Stones sang, “You Can’t Always Get What You Want.”

That’s the take from strategists at State Street Bank & Trust and John R. Taylor, formerly head of what was once the world’s biggest currency hedge fund. Part of the support for that thesis includes expectations for robust U.S. growth (even if tit-for-tat tariffs play out) that will keep the Federal Reserve hiking rates. Against that backdrop, the dollar has gained almost 6 percent since mid-April.

Dollar bulls also took cheer Monday after Treasury Secretary Steven Mnuchin over the weekend moved to ease fears that trade disputes had brought on a currency war. The greenback reversed some of its losses from Friday, when Trump criticized China and the European Union in a tweet, accusing them of “manipulating their currencies and interest rates lower.”

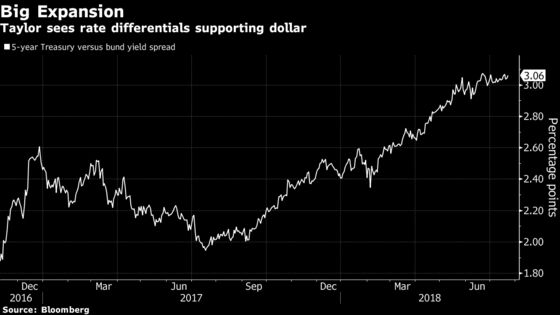

“The dollar will become stronger and stronger, despite Trump’s efforts to keep it weak,” said Taylor, who runs Taylor Global Vision, which produces a newsletter on financial markets. “The Fed will keep tightening and the worsening deficits will keep Treasury supply increasing,” which will keep U.S. yields attractive to international investors, supporting the greenback.

Although the European Central Bank is on course to end its asset-purchase program this year, it has indicated record low rates should remain at least until mid-2019. With the Fed lifting rates seven times since it began tightening in December 2015, the gap between U.S. and German benchmark yields at some maturities is the widest since at least the 1990s.

Favorable Case

Data this week should add to the case for the dollar. The U.S. economy likely grew at a 4.2 percent annual rate last quarter, the fastest since 2014, according to a Bloomberg survey. So even as trade tensions threaten global output, last year’s tax overhaul is helping stoke consumer spending and business investment.

For Tim Graf, head of macro strategy for Europe, the Middle East and Africa at State Street Bank & Trust, Mnuchin’s comments at the Group-of-20 summit this past weekend resonated.

“We are still overweight dollars,” Graf said. “If it’s a tariff-only story, then for the time being it’s still dollar-positive,” because China and the euro region have more to lose than the U.S. in such an environment.

“The dynamic changes if things around the currency change, but that’s still a fairly low probability of happening,” Graf said, referring to a scenario where countries race to weaken their currencies to gain an advantage.

Sanguine Outlook

Derivative traders seem to agree, as despite actual swings in exchange rates picking up on Friday, the outlook for the pace of movements (measured by implied volatility on the options) still mostly fell.

Roberto Perli, a partner at Cornerstone Macro LLC and a former Fed economist, says Trump’s criticism of Fed rate hikes actually may have improved the likelihood that policy makers tighten as planned, to drive home their independence.

“If anything, the incentive will be to tighten more, not less, because of this political pressure,” Perli said in a note Friday.

That’s good for traders who were long the dollar before Trump’s tweet storm.

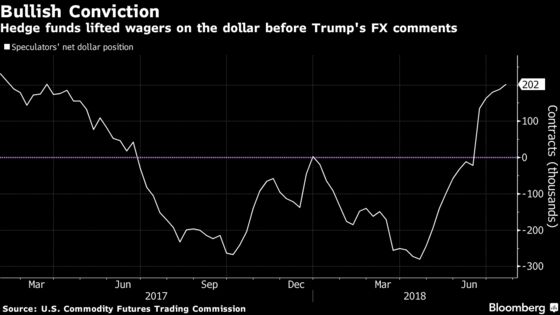

As of July 17, hedge funds and other futures speculators were the most bullish on the greenback since February 2017, U.S. Commodity Futures Trading Commission data show.

Their growing confidence in the U.S. currency does fly in the face of history, which shows that a full-blown trade war typically causes dollar weakness in the end.

But for now, as Taylor sums it all up, “Trump might want a weaker dollar, but he won’t get it.”

--With assistance from Jacob Bourne.

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Boris Korby

©2018 Bloomberg L.P.