Bondholders Tire of Losing Out When Funding Failed Acquisitions

Bondholders Tire of Losing Out When Funding Failed Acquisitions

(Bloomberg) -- The headache U.S. bond investors get from financing failed takeovers is getting worse, and they are calling for change.

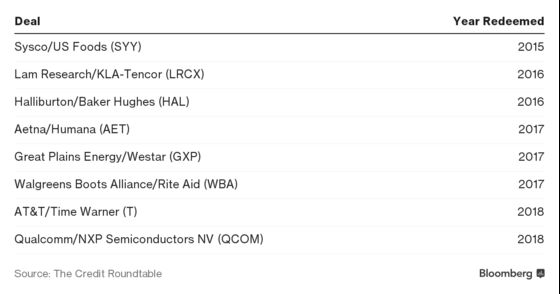

Since 2015, at least eight proposed M&A transactions that were funded in the bond market had to be called off, according to the Credit Roundtable, a New York-based organization advocating on behalf of bondholders. All eight allowed the borrower to repay the notes at 101 cents, even if the securities were trading at levels far higher than that.

Now, and despite years of complaints from bondholders about inadequate compensation, some borrowers are repaying the notes at 100 via a make-whole call rather than a so-called special mandatory redemption, which typically sees repayments at 101.

AT&T Inc. and Qualcomm Inc. used a make-whole provision when poised to miss deadlines related to the acquisitions of Time Warner Inc. and NXP Semiconductors NV after raising a total of about $40 billion. Walmart Inc.’s $16 billion bond offering in June to fund its acquisition of Flipkart Group also includes a make-whole call provision.

It “was bad to get called at 101 but what we’ve seen more recently is folks getting called at less than 101,” said Alex Diaz-Matos, an analyst at Covenant Review, a firm specializing in debt document analysis. “People never thought the make-whole call would really be cheaper than the special mandatory redemption provision and now it is,” Diaz-Matos said.

Make-whole calls are typical in bond indentures and allow the issuer to redeem the debt at specific spread above a U.S. government bond or at par, whichever is greater. Rising rates can make the make-whole call cheaper, and give a lower-cost alternative to the special mandatory redemption clause.

“As bond investors, the only time we can negotiate these terms is at the new issues and that’s where we’re trying to educate the market,” said David Knutson, a co-head for the Credit Roundtable, which is made up of 42 member firms. “If the language is in there, and management has the option to do things at the interest of shareholders but expense of the bondholders, this is where you’re really transferring value away from fixed income holders.”

To be sure, it’s rare for bonds to be called back at a make-whole price under the 101% percent premium guaranteed by the SMR, said Joseph Kaufman, partner at Simpson Thacher & Bartlett LLP. SMRs are in just 50 percent of M&A financing deals and there are only limited circumstances in which it could be applied. Such a bond would need a low coupon, rising Treasury rates and only then could the make-whole calculation come out below the SMR premium of 101 percent, Kaufman said.

In June, Credit Roundtable published proposals setting limits on the use on the clauses. Knutson says bondholders are accepting looser terms just as the credit cycle is reaching its latter stages.

“The market is generally pretty healthy and pretty strong and typically later in an economic cycle or market cycle, you get investors often willing to accept less -- less return or less restrictive covenants or less robust indentures,” Knutson said.

--With assistance from Brian Smith and Thomas Penaherrera.

To contact the reporter on this story: Shelly Hagan in New York at shagan9@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, ;Christopher DeReza at cdereza1@bloomberg.net, Faris Khan

©2018 Bloomberg L.P.