It’s Hard to Know What the Safe Havens Are Anymore: Taking Stock

It’s Hard to Know What the Safe Havens Are Anymore: Taking Stock

(Bloomberg) -- Aside from the whippy action in the yuan that afflicted markets last night, it was a relatively quiet session for stock futures right up until Trump’s comment that he was "ready to go" with import tariffs on $500 billion of Chinese goods was aired on TV -- this hit S&P e-minis to the tune of ~12 handles and we’re now poised to open right at the key 2,800 mark.

One area of promise is the early positive reaction to the big industrial earnings that just crossed the wires, with GE rising ~0.5% (on a penny beat and, probably more importantly, no major panic-inducing announcements) and Honeywell up more than 2% after boosting its revenue target above the consensus view. Also the oil service majors, Schlumberger and Baker Hughes, are both indicated up after their reports.

Another promising trend is the renewed interest in U.S. stocks as shown by the latest fund flows data. Lipper data shows $5 billion in inflows for U.S.-based equity ETFs for the week ended July 18, after six straight weeks of withdrawals, while EPFR Global data said U.S. stocks took in $2.3b versus outflows in Europe and emerging market equities.

The Bad News for the Bulls

The S&P 500 had its largest decline in six sessions on Thursday in conjunction with overall market volumes coming in at their highest in three weeks. The good news for the bulls is that we held the 2,800 level after a very brief test in the first half hour of trading; the bad news is that earnings reactions were much worse on Thursday than Wednesday while the Philly Fed six-month outlook dropped to its lowest in over two years and the expectations for future labor demand tanked to levels unseen since last February of last year.

Trump’s meddling in Fed affairs may only complicate things when it comes to the dot plots, or at the very least heighten the sense of uncertainty over Powell’s frame of mind in the near term, while his talk on China tariffs may make any longs nervous going into the weekend.

As for sector moves, the defensive groups led the S&P 500 on Thursday for the first time all week, with both utilities and REITs climbing ~1% while consumer staples had a respectable showing considering that Philip Morris looked like grim death off the open (similar to how shares collapsed 16% after last quarter’s results) only to stage an impressive recovery throughout the session.

On the flip side, the big run-up in the financials (BKX up 3.6% in first three days of the week) stalled out after a multitude of concerning results from the regional banks and the trust banks as well as from AmEx, Travelers, and Blackstone.

FAANG Safe Haven No More?

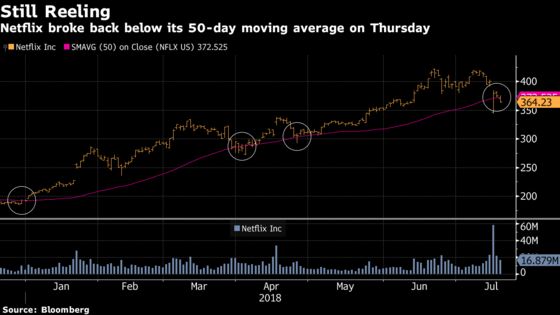

Meanwhile, tech traded more or less in line with the tape, but the same can’t be said about the FAANGs, where every member underperformed aside from Apple -- the most notable laggard was Netflix, as shares slipped through their 50-day stronghold for the second time this week and are now down more than 9% since Monday night’s subs miss.

It initially appeared as though the bulls dodged a FAANG-tipped bullet when Netflix staged that massive reversal off the open on Tuesday, but the recent action might give some momentum traders pause, perhaps even make some start to question whether the crowding into some of these hedge-fund hotels is starting to look a tad frothy.

The concern was highlighted yesterday by Wolfe Research Chief Investment Strategist Chris Senyek in a note titled, "Time to Sell FAANG?" He points to the wide P/E valuation spread between momentum and value stocks, as many investors "perversely" used the market’s most expensive stocks as safe havens during more turbulent times.

In turn, he recommends using these momentum stocks as a source of funds in the coming weeks because 1) if a trade resolution comes about, he expects a sharp rotation out of these names, or 2) if a trade war unfolds further, he expects another drawdown in the market with the highest P/E momentum names materially underperforming.

Mark Your Calendar: Monday 12pm ET

Along these lines, I’d like to invite all Taking Stock readers and Bloomberg terminal clients to join me Monday at 12pm as I host a Top Live Q&A on Netflix. We’ll have a bull vs bear debate between two analysts, BTIG’s Richard Greenfield, who raised his price target to $420 after the earnings report, and Wedbush’s Michael Pachter, who has had Netflix at underperform for years with a current price target of $125.

I’ll be handpicking questions from clients so please email TopLive@bloomberg.net in advance of the Monday event. Note that these questions will show up as anonymous i.e. your name and firm will not be advertised.

Sectors that may outperform today:

- Tech sentiment in general should get an uplift after Microsoft (+3.3% post-market) followed IBM with solid numbers; watch the cloud names after the company signaled strength in that business

- Apple suppliers after Skyworks (+3%) numbers, as Qorvo ticked higher post-market and others that may do the same include Cirrus Logic and Analog Devices

- Financials after a pitiful day on Thursday, as mentioned above, with Capital One (+2.1%) notching a huge earnings beat while Discover Financial announced a $3 billion buyback and boosted its dividend

- Industrials given the early strength in GE and HON, as mentioned above

- Chemical sector after CE (+7.3%) forecast midpoint topped the highest analyst estimate out there

Sectors that may underperform today:

- Footwear and apparel companies after a ginormous whiff all around by Skechers (-26% and the downgrades are starting to hit), a similar plunge as last quarter for the stock; this could hit a wide array of names in the space, from VF Corp., Crocs, Deckers, Foot Locker and DSW to the biggies like Nike and Under Armour

- Floral and gift stocks, the few that are out there, could get hit after smallcap FTD Companies (-21%) gave brutal preliminary revenue figures and an updated outlook with a lot of mentions of the word "headwind"; watch 1-800-Flowers.com for any read-across

- Machinery stocks after weaker-than-expected orders from Sweden’s Atlas Copco (-4.8% in Stockholm)

On Tap Next Week

Earnings will be the focus given that ~40% of the S&P 500 will be releasing results during the next five days, including three-fifths of the FAANG complex (AMZN, FB, GOOGL), semiconductor giants (INTC, QCOM, and TXN, who gave some preliminary numbers on Tuesday), industrial bellwethers (BA, HON, UTX, MMM), big automakers (GM and F), oil majors (XOM, COP, CVX, RDS/A, HAL, SLB), and some recent high-fliers like AMD, TWTR, GRUB, NOW, and WWE.

Risk arbitrage traders will be awaiting a couple huge events, from the NXP Semi/Qualcomm deal termination date (and end the saga of this potential trade war casualty, unless it gets extended) to the Fox shareholder vote over the Disney deal.

On the macro front, we have the G-20 in Buenos Aires coming up this weekend, the WTO’s General Council meeting to go over the U.S.-China trade conflict, talks between Trump and European Commission President Jean-Claude Juncker (Trump said auto tariffs will be a focus) as well as the resumption of Nafta negotiations, and several key economic datapoints such as the Markit PMIs, 2Q GDP, New & Existing Home Sales (after Wednesday’s clunker of a housing starts print), and the ECB meeting.

And for those with vacations coming up, JonesTrading Institutional Services Head of ETF Trading and Macro Strategy Dave Lutz has compiled his Summer reading list after a survey of traders. Picks include "Hedge Hogs" by Barbara T. Dreyfuss, "Bad Blood" by John Carreyrou, "The Everything Store" by Bloomberg’s Brad Stone, "Shoe Dog" by Phil Knight, "Thinking in Bets" by Annie Duke, "Skin in the Game" by Nassim Taleb, and many more.

Notes From the Sell Side

It’s a sea of earnings reviews and previews, and not a whole ton of major calls but here are the biggest calls so far:

Deutsche Bank lifts targets on the FAANGs reporting next week (all buy rated), with AMZN remaining the top pick and a new PT of $2,200 matching the highest on the Street -- says any concerns are far outweighed by the "large and expanding" TAM, e-commerce penetration, the "power of Prime," and many more positives..

Goldman sees the rally in large banks continuing in the near term thanks to attractive valuation after earnings that were largely better than expected; the analyst cites further NIM expansion, NII growth, operating leverage, and "capital markets lapping easier comps" in the second half..

Bernstein reduces price targets on the defense stocks ahead of earnings next week, noting that growth appears more muted in 2019 and thereafter.. BofAML moves Yum China to an underperform on earnings downside risks ("likely peaking trend for KFC").. Goldman sees an overall decline in sales for HOG after final checks for the second quarter..

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- IPO lockup expiry: TRTX

- 7:00am -- SLB, STT earnings

- 7:30am -- MAN earnings

- 8:00am -- Fed’s Bullard speaks on economy and monetary policy

- 8:00am -- KSU, CLF, GNTX earnings

- 8:30am -- Commerce Department hearing on potential tariffs on auto imports

- 8:30am -- GE, SLB earnings calls

- 9:30am -- HON, BHGE earnings calls

- 11:00am -- SCHW business update call

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.