China's Peer-to-Peer Lenders Are Falling Like Dominoes as Panic Spreads

China's P2P Platform Failures Surge as Panic Spreads in Market

(Bloomberg) -- The shakeout in China’s $192 billion peer-to-peer lending industry is accelerating at a rapid clip.

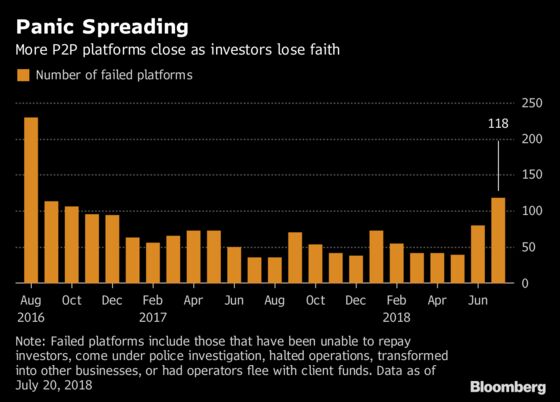

At least 118 platforms have failed this month through early Friday, according to Shanghai-based Yingcan Group, whose tally for July stood at 57 just three days ago. The number of failures, which includes platforms that have halted operations or come under police investigation, is already the highest in two years with more than a week left in the month.

China’s clampdown on financial risk has weighed on P2P platforms for the past two years, but the pressure has intensified in recent months after the country’s credit markets tightened and the banking regulator issued an unusual warning to savers that they should be prepared to lose all their money in high-yield products. While that has triggered bouts of panic among users of smaller P2P platforms, there’s little evidence that the turmoil has spread to more systemically important parts of China’s financial sector.

Authorities are focused on weeding out bad actors in the P2P industry, one of the riskiest and least-regulated parts of China’s $10 trillion shadow-banking system, according to Chen Shujin, chief financial analyst at Huatai Securities Co. in Hong Kong.

“The industry is going through an elimination process,” Chen said. “There’s no perfect way for the government to get rid of all those bad ones because there are thousands of them online. They will be reduced to a handful before we see any healthy development.”

Analysts at China International Capital Corp. estimated on July 13 that no more than 200 firms, or about 10 percent of existing platforms, will still be around in three years.

The nation’s P2P platforms, which facilitate loans from mostly individual investors to borrowers willing pay high rates of interest, have about 50 million registered users and 1.3 trillion yuan ($192 billion) of outstanding loans, which yielded an average 10.2 percent in the first half of the year, official figures show. Reported default rates vary from zero on the best platforms to 35 percent on the worst, according to National Internet Finance Association of China.

Jinyinmao, a Shanghai-based P2P lender, was one of the latest platforms to close down this week. Investors lack confidence and funds are flowing out “significantly,” the company said in a statement on Wednesday. “Some borrowers have lost their intention and ability to repay their loans, leaving a huge impact on our operations and drying up our liquidity.”

The government introduced a complex registration process in December to clean up the sector, with officials in Shanghai identifying 160 problem areas such as overly high interest rates, misuse of funds and exaggerated return figures.

“People that are running these P2P companies don’t actually understand what P2P really is,” said Kenny Lam, president of Noah Holdings Ltd., China’s first private asset manager for the ultra rich. “When regulations come in, a lot of P2Ps won’t survive.”

To contact Bloomberg News staff for this story: Alfred Liu in Hong Kong at aliu226@bloomberg.net;Jun Luo in Shanghai at jluo6@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues

©2018 Bloomberg L.P.

With assistance from Editorial Board