Crude's Bull Run Made This Oil-Sands Producer Canada's Top Stock

Crude's Bull Run Made This Oil-Sands Producer Canada's Top Stock

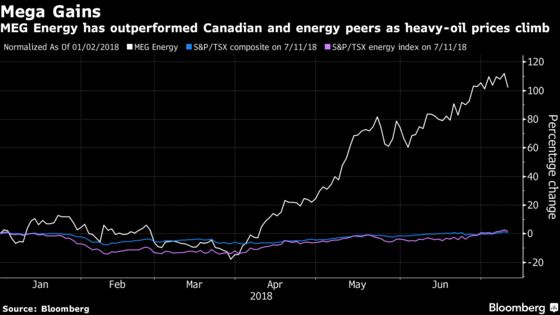

(Bloomberg) -- For any investor who was looking to gain from rising oil prices, there may not have been a better way to play the recent bull run than MEG Energy Corp.

So far this year, the Canadian oil-sands producer has more than doubled in value. Its shares in Toronto are leading the 246-company S&P/TSX Composite Index and blowing away peers in the S&P/TSX energy index, which is up just 3.7 percent. Calgary-based MEG is even beating the best-performing U.S. rivals on the S&P 500 energy index.

“This is, perhaps more than any other energy equity in North America, the most levered name to oil you can think of,” said Chris Cox, an analyst at Raymond James. “It’s probably the preferred name for anyone who’s getting bullish on oil and trying to get exposure.”

MEG’s surge has been driven by its status as a pure-play heavy-oil producer, churning out about 93,000 barrels a day from Alberta’s Athabasca oil sands, at a time when falling production from Venezuela and Mexico has left U.S. Gulf Coast refiners hunting for more heavy crude. The situation has pushed up the price of Western Canada Select almost 50 percent this year, about triple the 16 percent gain for more expensive West Texas Intermediate light oil.

By contrast, Canada’s other major oil-sands players all produce some natural gas or have refining operations that dilute their benefit from rising heavy-oil prices. MEG also is carrying a higher-than-average debt load, making it more vulnerable to crude prices when they drop but more dramatically improving its prospects in a rally like this year’s.

Debt Concerns

While MEG’s hefty borrowing was exactly what had led many investors to shy away from the stock, the company addressed concerns over its indebtedness earlier this year by selling its stakes in the Access Pipeline and the Stonefell Terminal oil-storage facility for C$1.61 billion ($1.2 billion). The shares jumped 13 percent the day that deal was announced.

Though the company still has debt of more than four times its earnings before interest, taxes, depreciation and amortization -- more than peers like Suncor Energy Inc. and Canadian Natural Resources Ltd. -- Cox said the asset sales made MEG much more “palatable” for investors.

“That gave the market the comfort to take the risk on the story on the basis that oil goes higher, without the balance sheet being so challenging that you couldn’t get around it,” he said.

Lowering Debt

MEG will start generating free cash flow next year and should work its debt down to about two times Ebitda, in line with peers, by 2020, said John Rogers, MEG’s head of investor relations. The company also is ramping up production to 113,000 barrels a day by 2020, which will increase its ability to generate cash, he said.

“We’ll basically be growing into our debt,” Rogers said.

However, there are risks ahead. Company founder Bill McCaffrey retired as chief executive officer in May, and MEG is searching for a successor who will continue to execute on the company’s strategy. The transportation system in western Canada remains fragile, even though MEG currently has capacity to move a third of its output to refiners on the Gulf Coast.

As for oil, OPEC and its allies recently pledged to increase production by 1 million barrels a day, while a trade war between the U.S. and China, the world’s two largest consumers of crude, dims the outlook for growing demand. Prices for the WTI benchmark in the U.S. plunged 5 percent on Wednesday after U.S. President Donald Trump’s government announced tariffs on another $200 billion of Chinese-made products. MEG fell 4.6 percent.

Chinese Investment

Plus, the producer’s rally this year to C$10.78 Wednesday still leaves it more than 80 percent off its high of almost C$53 seven years ago, and the company remains a money loser for China’s CNOOC Ltd., its biggest shareholder.

That’s not to mention that the run-up in MEG’s shares has stretched its valuation. The stock is trading at an enterprise value of about eight times next year’s estimated Ebitda. That’s higher than the ratio of 6.8 times at Suncor and Canadian Natural Resources. Cox downgraded MEG’s shares to the equivalent of a hold last week, based solely on its valuation.

For his part, MEG’s Rogers says the company’s value hasn’t been fully realized. MEG is boosting its production amid rising oil prices with an improved balance sheet and free cash flow on the horizon, he said.

“We’re still kind of in the early innings of this game, in terms of this entire recovery,” Rogers said in an interview. “We don’t think we’re fully valued today at all.”

To contact the reporter on this story: Kevin Orland in Calgary at korland@bloomberg.net

To contact the editors responsible for this story: Reg Gale at rgale5@bloomberg.net, Carlos Caminada, Steve Stroth

©2018 Bloomberg L.P.