A Peculiar Practice in Japanese Bond Sales Hurts Investors and Banks

A Peculiar Practice in Japanese Bond Sales Hurts Investors and Banks

(Bloomberg) -- When Japan’s Denso Corp. issued 40 billion yen ($362 million) of bonds in a recent offering, its underwriters said the notes sold out. Investors weren’t so sure that was true.

That’s a reflection of a peculiar practice in Japan: underwriters keep it to themselves who the investors buying bonds are, unlike in the U.S. and Europe, where managers usually share information about the bidders. In Japan, if a sale doesn’t attract enough demand, bankers can keep the unsold portion themselves but still declare that everything was sold.

That is what investors suspect happened with Denso. Similar issues have occurred with recent note offerings by companies including ANA Holdings Inc., JFE Holdings Inc. and Nippon Steel & Sumitomo Metal Corp., according to people familiar with the matter.

Issuers benefit because they get to complete a deal at a lower yield. But investors and underwriters lose. Banks sometimes offload the debt at lower prices, which is bad for the original buyers of the bonds, said the people familiar with the practice, who asked not to be identified because they aren’t authorized to make public comments. And the underwriters have to take the loss on the difference, the people said.

This phenomenon is fueled by pressure among brokerages to win underwriting deals, at a time when the Bank of Japan’s negative-rate policy is making it harder to price corporate notes. Underwriters don’t want issuers to know if the yield premiums offered were too low and failed to attract enough demand, because it may raise questions about their competence.

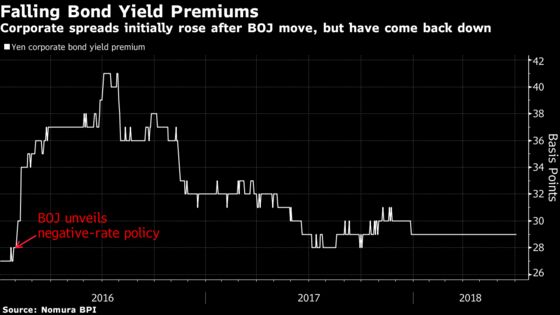

See also: Japanese regulators are cheering more transparent bond sales

“We’ve recently seen many cases in which spreads are set at too tight a level,’’ said Takahiro Oashi, senior fund manager at Asahi Life Asset Management. Some brokerages gave him the impression that “they are setting prices in favor of issuers rather than investors,’’ he said.

The phenomenon isn’t new. In a 2010 report, the Japan Securities Dealers Association acknowledged criticism that bond terms had at times diverged from market levels due to inaccurate reporting by underwriters on demand for the securities. Japan’s Financial Services Agency is aware of market concerns about corporate bond sale practices, but the regulator doesn’t see it as something that needs to be tackled immediately, an official said earlier this year.

The practice is an industrywide problem rather than specific to certain underwriters, said the people familiar with the matter. The spokesmen for the five biggest underwriters of yen bonds this year -- Mizuho Securities Co., Nomura Securities Co., SMBC Nikko Securities Inc., Daiwa Securities Co. and Mitsubishi UFJ Morgan Stanley Securities Co. -- declined to comment.

Misjudging Demand

While data aren’t available for how many note offerings haven’t sold out, the issue is attracting more attention as the BOJ pushes ahead with its negative-rate policy introduced in 2016.

In a three-tranche bond offering by auto parts maker Denso in April, for example, brokerages failed to sell some of the 10-year notes, according to four people familiar with the matter. The yield premium on the securities has climbed two basis points since late-April to 28 basis points, according to Bloomberg-compiled prices.

Underwriters also weren’t able to sell some of the 20-year bonds offered by ANA Holdings in May, because the terms weren’t as good as those for an earlier comparable bond sale with a similar tenor, said people familiar with the matter.

And brokers couldn’t sell out seven-year debt in a three-tranche offering by Nippon Steel & Sumitomo Metal last month, according to people familiar with the matter.

Read more: Hungary sold Samurai bonds using so-called pot system

The accounting division of Denso said by email that its underwriters said the orders exceeded the sale amount. ANA spokesman Atsushi Tanabe said the lead manager reported to the company that all the bonds were sold. Spokesmen for Nippon Steel & Sumitomo Metal said the company hasn’t heard from underwriters that some of its bonds were unsold.

In the face of criticism about Japan’s prevalent bond sale practice, which is known as the retention system, issuers are slowly beginning to sell notes more in line with U.S. and European norms. Under the so-called pot system used overseas, syndicate banks share details with issuers about bond buyers to find the best prices.

Billionaire Tadashi Yanai’s Fast Retailing Co. opted to use that system when it priced notes in May, and so have a string of overseas borrowers selling Samurai securities including BNP Paribas SA, as well as domestic issuers of hybrid bonds such as Nomura Real Estate Holdings Inc.

More use of the pot system in Japan could reduce trading costs for investors by making the debt offerings more transparent, according to Manulife Asset Management.

“That’s something positive that could materialize over the long-term,” said Shunsuke Oshida, senior credit analyst at the money manager. “I expect that the pot method will gradually take hold.”

To contact the reporters on this story: Issei Hazama in Tokyo at ihazama@bloomberg.net;Takashi Nakamichi in Tokyo at tnakamichi1@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum

©2018 Bloomberg L.P.