Hedge Funds Facing Trump's Trade War Crossfire Feel the Pain

Hedge Funds Caught in Trump's Trade War Crossfire Feel the Pain

(Bloomberg) -- In a booming year for mergers and acquisitions, hedge funds that seek to make money from corporate marriages are struggling.

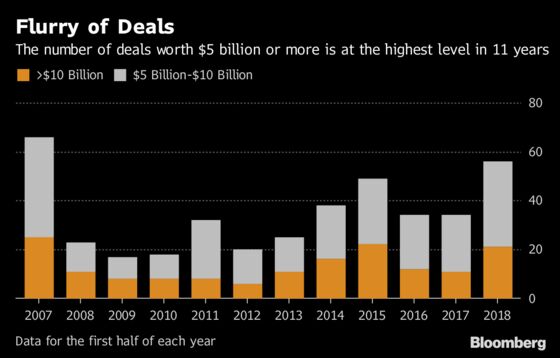

The value of deals surged 43 percent in the first half of the year, with large takeovers reaching the highest number since before the financial crisis. That should have offered a fertile hunting ground for managers who bet on or against such deals. Yet their investment pools, known as merger arbitrage funds, lost money in the period, sending some investors fleeing.

The underperformance -- in a strategy that’s considered somewhat insulated from the usual market swings -- is caused in part by rising political risks to high-profile deals that blindsided some funds. The Trump administration this year blocked what would have been the largest technology deal ever, Singapore-based Broadcom Ltd.’s attempted purchase of Qualcomm Inc., while another deal was delayed by the increasing tensions between the U.S. and China. Spikes in market volatility are adding to the damage.

“U.S. deals are increasingly getting caught in a political slugfest and it’s difficult for fund managers to become political analysts," said Pierre Henri Flamand, who helps oversee $38 billion as chief investment officer of Man Group Plc’s GLG unit. “It has been a riskier environment since the couple of blow-ups we have seen.”

Merger-arbitrage funds seek to profit from the difference between the stock price of a target company when a deal is announced and the price when the transaction is completed. The larger the difference, or spread, the greater the potential profit for the fund -- unless a deal falls apart or faces long delays.

That’s what happened with Qualcomm Inc.’s bid for chipmaker NXP Semiconductors NV. The deal became a proxy in the U.S. and China trade war earlier this year, with Chinese antitrust authorities delaying the offer further on April 19. The shares, one of the most widely held positions across hedge funds, slumped more than 10 percent in April, inflicting losses on some event-driven money pools and causing deal spreads to widen across the industry.

While the shares have since rebounded, the slump caused losses at a number of hedge funds in April. The $1.2 billion PSquared Event Opportunity Master Fund lost 2.4 percent on its bet on NXP alone, while the Abrax Merger Arbitrage Fund lost 2.7 percent on its investment in the company, their letters to investors show.

A spokesman for Abrax said the fund has since recovered losses from NXP. Officials for PSquared didn’t return phone calls seeking comment.

Across the industry, merger-arbitrage funds fell 0.6 percent in the first half, and event-driven funds, which seek to profit from corporate actions more broadly, slumped 4.5 percent.

“Despite strong global deal flow, complex cross-border regulatory oversight and political and macro rhetoric has created an unprecedented amount of volatility across the merger-arbitrage space," said Jamie Sherman, a portfolio manager at London-based event-driven hedge-fund firm Kite Lake Capital that manages $1.1 billion.

Qualcomm itself had been the target of a $117 billion hostile bid by Broadcom, but the deal was derailed by the U.S. government, which cited national security concerns. Large deals such as this one generally offer better money making opportunities for hedge funds because the spread tends to be wider and the shares are very liquid, making it easier to trade in and out of a position.

In total, companies splurged $1.7 trillion on mergers and acquisitions in the first half, according to data compiled by Bloomberg. The total value of deals worth at least $5 billion more than doubled to $777 billion.

Yet some deals may reflect a desire to make use of cheap money while interest rates are still low, instead of longer-term thinking, leading to a bigger likelihood of them falling apart.

“Strategically, the deals that are happening appear to be of lower quality,” Flamand said. “People make approaches and then disappear. This makes it tougher for merger arbitrage funds.”

Another high-profile deal to fail, Fresenius SE’s $4.3 billion offer for American drugmaker Akorn Inc., has since evolved into a legal battle over exactly why the German health-care company dropped its bid. Fresenius officials said in April they pulled their offer after being misled about Akorn’s product-development practices. Akorn sued to force a completion of the buyout, saying the German company simply had “buyer’s remorse.”

Funds that got caught in the crossfire of such deals now face an accelerated client exodus as some investors conclude the strategy gives a false sense of protection and the money pools are not offering sufficient returns to compensate for the expected volatility in the market. Already, event-driven hedge funds -- which include merger-arbitrage strategies -- have been hit by $4.6 billion of net outflows during the first five months of this year, the most for any strategy, according to data compiled by eVestment. Hedge funds overall collected $12.5 billion during the period.

“There is now a general risk-aversion related to the growing anxiety on trade rhetoric from the U.S. administration and other governments around the world," said Michele Gesualdi, who oversees $3 billion as the chief investment officer at Kairos Investment Management, which invests in hedge funds.

To contact the reporters on this story: Nishant Kumar in London at nkumar173@bloomberg.net;Suzy Waite in London at swaite8@bloomberg.net

To contact the editors responsible for this story: Neil Callanan at ncallanan@bloomberg.net, Christian Baumgaertel, Ross Larsen

©2018 Bloomberg L.P.