Utility Companies Head Into a Cloudy Future

Utility Companies Head Into a Cloudy Future

(Bloomberg Opinion) -- The world’s publicly listed utilities employed 3.7 million people, had a third of a trillion dollars in capital expenditures, and brought in $2.2 trillion in revenue in 2017. Power supply is an enormous industry. It’s also an industry that would still be recognizable to utility executives from a century ago. Delivery of electricity, natural gas and water will remain part of the future — but what changes will that future entail for utility companies themselves?

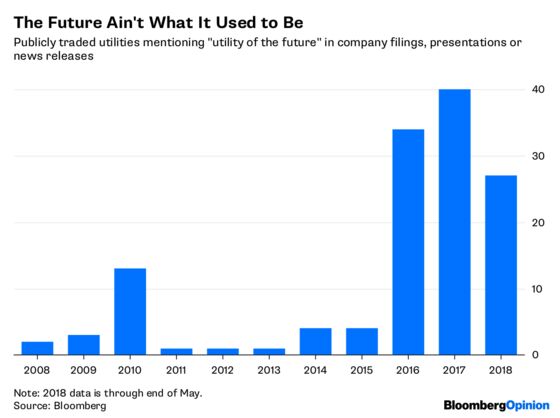

It involves a lot more talking about “the utility of the future”:

Part of that is a focus on technological, economic and even demographic changes as the industry’s workforce ages. Part of it, too, though, is probably marketing: In 2016, MIT released a 382-page (and heavily utility-sponsored) study called “Utility of the Future: An MIT Energy Initiative Response to an Industry in Transition.” It’s insightful; “utility of the future” is also the sort of catchy phrase that finds its way into company literature.

As the MIT study notes,

A range of more distributed technologies – including flexible demand, distributed generation, energy storage, and advanced power electronics and control devices – is creating new options for the provision and consumption of electricity services. In many cases, these novel resources are enabled by increasingly affordable and ubiquitous information and communication technologies and by the growing digitalization of power systems.

I’m not certain that the most innovative work being done is central to the existing utility business model. For some of the most innovative work currently underway, there might not be a clear role for utility companies themselves, now or in the future.

Google’s data center energy optimization is a perfect example. Google has been optimizing data center hardware — both its servers and its cooling and lighting systems — for years. By 2014, it had already created data centers that used half the energy of the industry average. Taking it further, though, was something quite different.

So efficiency engineer Jim Gao wrote a software model that first recommended maximizing data center efficiency by shutting off the data center entirely. After some refinements, the eventual attentions of Google’s DeepMind machine learning team, and more “robust and general working models,” Google achieved some extraordinary results: Implementing the models at the company’s facilities led to a 40 percent reduction in cooling energy load and a 15 percent reduction in overall energy overhead. Google’s data center intelligence team believes that it has only just “scratched the surface” of machine learning’s general applications to their work. It’s an impressive bit of energy optimization with economy-wide implications, all without the help of utilities.

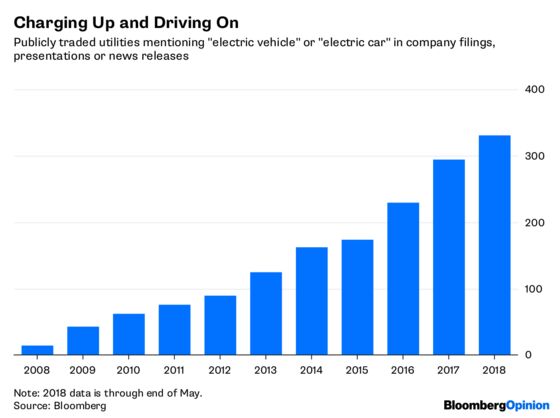

Electric vehicles are a different matter. A decade ago almost no utilities mentioned electric vehicles; this year alone, more than 300 have. Charging infrastructure is an obvious play for utilities; the 582,000 public charging outlets installed worldwide as of the end of last year are a fraction of what will be needed to support a fast-growing EV fleet. That infrastructure needs capital, experience, real estate, and policy and regulatory finesse. Utilities have all of these things.

Utilities have competition in the charging industry, and increasingly that competition comes from big oil. Last year, Royal Dutch Shell Plc purchased NewMotion, a large European charging provider. Last month, BP Plc followed suit, buying Chargemaster, the operator of the largest charging network in the U.K. Power suppliers, long a regulated monopoly, know they face a challenge.

Weekend reading

- A poll of Americans ages 20 to 45 reveals why they have, or expect to have, fewer children than they consider ideal. Climate change was an issue for a third.

- The tiny country of Dominica says that it can beat climate change.

- A new study finds that “real estate at higher elevations in cities at risk for climate change and sea-level rise appreciates at a higher rate than elsewhere.”

- The United Nations’ Green Climate Fund is at a low point after its director resigns.

- Amundi Energy Transition, a joint venture with French power generator EDF, has raised 500 million euros “to finance projects for energy transition among French regions and industries.”

- A new study of a proposed delay in coal plant retirements finds that the policy would support 790 coal mining jobs and cause 353 to 815 premature deaths.

- President Donald Trump’s trade policies are hurting those they purport to help – such as the 97 percent of jobs in aluminum that are “downstream” businesses shaping the metal into parts.

- To spite Harley-Davidson Inc., the president may have to turn to its Japanese and German motorbike-making rivals.

- Amy Myers Jaffe argues that when it comes to oil prices, business cycles and geopolitics “are now intersecting more integrally with structural technological change.”

- A Polish environmental group attached a device to the back of a white stork in order to track its migratory habits, and eventually lost track of the bird in eastern Sudan – where someone removed the tracking device’s SIM card, put it in their own phone, and racked up a $2,700 bill.

- A new doctoral dissertation finds that Lyft and Uber “nearly eliminate racial differences” in car pickup services.

To contact the editor responsible for this story: Brooke Sample at bsample1@bloomberg.net

©2018 Bloomberg L.P.