The Biggest Winner of Dell's Public-Market Return? Michael Dell

Michael Dell is returning his eponymous technology company to public markets, but on his terms.

(Bloomberg) -- Michael Dell is returning his eponymous technology company to public markets, after extolling the virtues of being private for years. But this time, it’s going to be on his terms.

Dell Technologies Inc.’s meticulously orchestrated plan to trade Class C shares on the New York Stock Exchange will give the computer and software maker all the advantages of a public listing with few of the drawbacks that caused the company to retreat in a 2013 leveraged buyout. Dell, who’s been in the tech business for 34 years, is in some ways taking a lesson from younger founders, such as Evan Spiegel of Snap Inc.: maintain as much control as possible and be less beholden to the whims of outside investors.

New Dell shareholders will be investing in a very different company from the one that delisted five years ago. Besides Dell’s diversification into faster-growing nooks and crannies of the technology market, investors will now have far less voting power than they once did. Michael Dell will own about half of the company, and he and private equity partner Silver Lake Management LLC will be able to ensure all votes go their way. As it worked to win approval for the 2013 buyout that took Dell private, billionaire activist investor Carl Icahn led a proxy fight to install a new board that would have replaced Dell. The new structure would rule out any similar revolt in the future.

Before Dell can move forward with the new simplified structure, the company has to get past the buyout of the DVMT tracking stock, originally meant to mirror its stake in Silicon Valley software maker VMware Inc. -- a move scheduled for the fourth quarter. Dell is offering DVMT holders the new Class C stock or $109 in cash per share. Current shareholders may not play nice, despite the offer’s $4.7 billion premium over the $17 billion valuation of the tracking stock as of Friday. They’ll be getting a diluted value for VMware, which currently has a market cap of $66 billion, and their new shares will mostly give them equity in Dell’s slower-growing hardware divisions.

Icahn, who holds a sizable position in both VMware and the tracking stock, is still studying the proposal to determine whether he’ll support it, according to a person familiar with the matter. Elliott Management Corp., another activist firm, is the fourth-largest shareholder of the tracking stock. A representative for Elliott declined to comment on its intentions for the DVMT buyout.

The transaction is a “major disappointment” for DVMT holders, Keith Moore, an FBN Securities analyst, wrote in a note Monday. Dell is “funneling” cash from VMware in a dividend, increasing the value of the tracking stock without holders seeing benefits of the increase. Still, it stops short of a merger, which could have sparked a VMware shareholder rebellion. The tracking stock rose 9 percent Monday to $92.20 -- short of the cash offer price, reflecting investors’ dim view of Dell’s value.

The heart of the deal is VMware’s $11 billion special dividend for its shareholders -- crafted to transfer about $9 billion in cash from the software maker’s balance sheet to Dell’s. One of the biggest drawbacks of Dell’s controlling stake in VMware, while maintaining the software maker’s independence, has been the inability of debt-ridden Dell to draw cash from fast-growing VMware.

“We are excited about VMware’s independent future as a company,” Chief Executive Officer Dell said on a conference call Monday. “We don’t have any future plans to change the structure and we’re excited about the go-forward.”

Dell’s decision not to pursue a full merger with VMware may also reflect concern about the so-called conglomerate discount -- a term for when a large diversified company trades at a lower valuation than its discrete parts. Besides that, VMware shareholders have blasted the notion of a merger of Dell and VMware -- one of the options Round Rock, Texas-based Dell laid forth when it announced its strategic review in January. VMware shares jumped 10 percent in New York trading Monday.

The deal potentially “takes away an overhang that Dell will reverse merge into VMware,” Mark Moerdler, an analyst at Sanford C. Bernstein & Co., wrote in an email.

Dell retreated from the public markets after becoming fed up with dealing with angry investors. With annual revenue at the time of $57 billion, Dell was the largest company ever to be taken private, based on sales, according to data compiled by Bloomberg. For a long time, Michael Dell thought it was a good idea.

“We have a structural advantage in terms of speed and our financial structure and we have the added benefit of being able to think about our business in a much longer-term horizon,” he said at his company’s annual trade show last year. “Certainly, as a founder that’s something I absolutely love.” Dell spoke of the virtues of being private as recently as the Dell Technologies World conference two months ago.

Some of those virtues have been measurable. Since going private, the supplier of personal computers and servers has expanded to capture a larger swath of the information technology market. Much of the change stems from its $67 billion deal in 2016 for storage-technology provider EMC Corp. and with it a majority stake in data-center software vendor VMware, cloud manager Virtustream and cybersecurity firm RSA. It also has a $3.2 billion stake in software company Pivotal, and a $900 million stake in Secureworks.

All those additions and changes make Dell a bigger force in the tech industry than ever before, and Michael Dell now has the opportunity to boost the valuation of his company. The stronger IT spending environment has buoyed the company’s sales, and a public listing could similarly bolster the CEO’s personal net worth. Dell, the man, had $22.1 billion before this new proposal, according to the Bloomberg Billionaires Index. More than $14 billion of his fortune is equity in his company. Those figures could soar if his company is able to execute this direct listing the way it expects.

Michael Dell’s stake in the newly public entity will be 47 percent to 54 percent fully diluted, the company said. He’ll also have considerable voting rights. Before going private in 2013, the founder had a personal stake of more than 15 percent -- and he needed to win a majority of the voted shares excluding his own to favor the buyout. That gave activists like Icahn plenty of leverage over the transaction’s outcome.

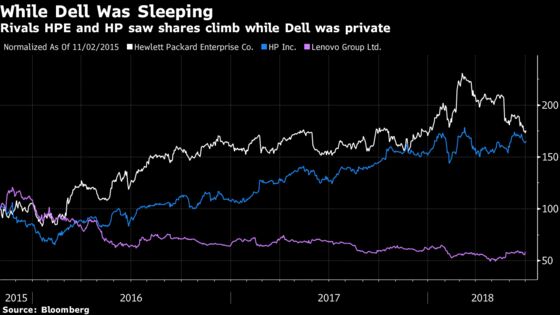

Dell, long known for his love of deals, also will now have more bandwidth to pursue them. Rather than pay in cash -- a precious resource needed to pay down debt -- the company can employ share swaps as currency to acquire new businesses and teams. This will help it stay competitive with rivals Hewlett Packard Enterprise Co. and Nutanix Inc., which have been snapping up smaller companies to burnish their offerings.

“The company’s go-forward opportunities in the internet of things, the edge, artificial intelligence and connectivity are very profitable ones, buttressed especially by software and services from VMware, RSA, Secureworks and Pivotal,” said Patrick Moorhead, an analyst with Moor Insights & Strategy. “There are still good profit pools in storage, networking infrastructure and, going forward, machine learning.”

Still, public investors in the new Dell will be staring down a lot of debt. Dell said it now has about $74.4 billion in annual revenue, and $53 billion invested in public subsidiaries, but also has $39.8 billion in core debt, as of the end of its first fiscal quarter, much of which funded the deal for EMC.

Dell on Monday said it has paid down about $13 billion in debt since acquiring EMC, and management is keen to get a good write-up from the credit rating services. Executives have already had preliminary "top level phone calls" with debt agencies on Friday, and "will be meeting them in next few days," Tom Sweet, Dell’s chief financial officer, said on a conference call Monday following the announcement.

--With assistance from Ian King, Dina Bass and Scott Deveau.

To contact the reporters on this story: Nico Grant in San Francisco at ngrant20@bloomberg.net;Giles Turner in London at gturner35@bloomberg.net

To contact the editors responsible for this story: Jillian Ward at jward56@bloomberg.net, Andrew Pollack

©2018 Bloomberg L.P.