European Banks Exploit a Weakness to Cut $145 Billion in Trades

European Banks Exploit a Weakness to Cut $145 Billion in Trades

(Bloomberg) -- Some of Europe’s biggest banks may have found a perfectly legal way to exploit a weakness in one of the finance industry’s most loathed rules.

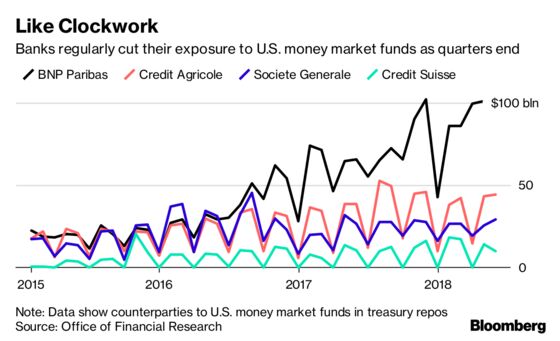

Euro-area and Swiss lenders cut their short-term borrowings by tens of billions of dollars just before the end of each quarter, improving their reported financial health, only to build them up again in the following weeks, according to the Bank for International Settlements. BNP Paribas SA, Credit Agricole SA and Societe Generale SA regularly shrink such trades, U.S. statistics show.

Almost a decade after the global financial crisis, lenders in Europe may be taking advantage of a loophole in the implementation of a key reporting requirement that aims to curb the amount of debt banks take on. While U.S. and U.K. banks must use an average figure over the quarter when reporting the measure, known as the leverage ratio, the Europeans only have to report numbers for the end of a quarter, enabling them to apply “window dressing,” according to a BIS report last month.

“It allows banks to provide a picture of their own state to the market that is distorted,” said Francesc Rodriguez-Tous, a finance professor at City University in London. “The leverage ratio is precisely there to ensure that banks don’t game the system.”

How It Works

The BIS report points to the $1 trillion U.S. market for short-term collateralized loans known as repurchase agreements, or repos, a segment that provides a glimpse into how banks fund themselves. In a typical deal, a bank borrows cash by selling U.S. Treasuries to a money-market fund and agreeing to buy back the securities the following day. Banks can also use the borrowed cash to make loans through trades known as reverse repos.

If the repo market sounds complex, the “window dressing” is relatively simple, according to the BIS. As the end of a quarter approaches, euro-area and Swiss banks just pull back from the market for a few weeks, unwind much of their existing repo trades and turn down new ones.

Since European banks started disclosing their leverage ratio in early 2015, the “amplitude of swings” in euro-area banks’ repo trades has been rising, with major banks showing a contraction in borrowing from U.S. money market funds of $145 billion at the end of 2017. That compared with $35 billion two years earlier, according to the report. “Similar patterns are apparent” for Swiss lenders, the BIS said.

“Window dressing in repo markets is material,” wrote the BIS, which acts as a central bank for the world’s central banks. “Data from U.S. money market mutual funds point to pronounced cyclical patterns in banks’ U.S. dollar repo borrowing, especially for jurisdictions with leverage ratio reporting based on quarter-end figures.”

BNP Paribas, based in Paris, was a counterparty to $99 billion of repo trades with U.S. money-market funds backed by Treasuries at the end of May, 16 percent of the total and more than any other lender, data from the Office for Financial Research show. The next four biggest -- Barclays Plc, Credit Agricole, HSBC Holdings Plc and Societe Generale -- account for about 23 percent of the market.

Many of them show big swings between the middle and the end of a quarter that have been increasing in size. Since the start of 2015, Credit Agricole and Societe Generale cut their Treasury repo exposures during the final month of every quarter, with declines averaging more than 50 percent, according to Bloomberg calculations. BNP Paribas reduced its dealings in the vast majority of periods, by an average of 34 percent.

To get a better sense of the swings, take Credit Agricole’s dealings so far this year. The bank, based in the Parisian suburb of Montrouge, had $9.9 billion of Treasury repo trades outstanding on Dec. 31, 2017, OFR data show. This soared to $38 billion in January and $42 billion in February before slumping 65 percent to $15 billion at the end of the quarter in March. Trades have since swelled again to more than $44 billion.

‘Client Financing’

Credit Suisse Group AG, based in Zurich, has a smaller repo exposure compared with its French rivals. Still, the bank reduced its dealings in the final month of every quarter since the start of 2015, by an average of 97 percent.

“It is not accurate to suggest that these movements are sufficient to have a material impact on Credit Suisse’s reported leverage ratio,” James Quinn, a spokesman for the bank, said in an emailed statement. “The changes in these positions at the end of each quarter stem from fluctuating client financing needs and relate to a very small proportion of our total leverage.”

Officials for the other banks declined to comment.

Indeed, the figures give only a small window into banks’ funding operations, and the data shows similar patterns, if less pronounced, for some U.S. and U.K. firms that can’t game the leverage ratio the same way. Barclays and JPMorgan Chase & Co., for instance, also regularly reduced Treasury repos with U.S. money market funds. But in jurisdictions that still allow banks to report their leverage ratio for the end of the quarter, banks may have “strong incentives” to adjust their exposures around the reporting date, the BIS said.

‘Everyone Knows’

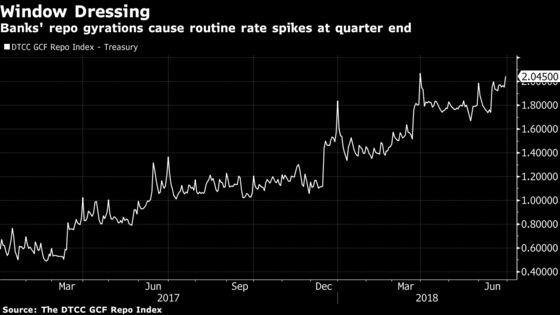

The “window dressing” in repo markets is so common that investors expect it, according to Scott Skyrm of Curvature Securities LLC, who has worked in the industry since 1990. Banks’ pullback adds volatility and helps increase repo rates before the end of a quarter, he said.

“Everyone knows that at year-end, quarter-end, rates spike,” said Skyrm in a phone interview. “It creates more volatility in the market than what naturally should be there.”

Bank employees often alert their counterparties at money funds in advance before they start to pull back, according to Debbie Cunningham, chief investment officer for money-market funds at Pittsburgh-based Federated Investors, which oversees $392 billion. When they realize later that they need additional funding after all, rates can shoot up, she said.

“It’s the surprise at the end of the quarter that causes the rate to bump up more,” Cunningham said. “In order to get back into the market place, you’ve got to pay up.”

Higher interest rates this year have provided some relief from the volatility, because they make repo trades more profitable, encouraging banks to keep trades on as the end of the quarter approaches, she said.

‘Critical Issue’

Regulators in Europe are aware of the loophole their implementation of the leverage ratio has created. Finma, the Swiss financial regulator which is overseeing the country’s largest banks, said it’s aware of the BIS report and the issue it raised. A spokesman said the regulator is analyzing the situation but declined to comment on specific banks.

The European Union is currently implementing a binding leverage ratio as part of a broader overhaul of bank-capital rules. In an attempt to plug the loophole, the European Parliament proposed a tweak that would force large banks to report the ratio based on average values, rather than take a snapshot at a reference date. A final version of the rule still needs to thrashed out with national governments, after which banks will get time to prepare for the new regulations.

“I don’t think we’re going to see a closure of the loophole anytime soon,” said Paolo Saguato, a law professor focused on financial regulation at George Mason University in Fairfax, Virginia, who cited a number of “big priorities” the EU may deal with first. “Window dressing, while being a critical issue, is not at the top of the list.”

--With assistance from Jan-Henrik Förster, Liz Capo McCormick, Alexander Weber and John Glover.

To contact the reporters on this story: Donal Griffin in London at dgriffin10@bloomberg.net;Nicholas Comfort in Frankfurt at ncomfort1@bloomberg.net;Fabio Benedetti-Valentini in Paris at fabiobv@bloomberg.net

To contact the editors responsible for this story: Ambereen Choudhury at achoudhury@bloomberg.net, Christian Baumgaertel, Jon Menon

©2018 Bloomberg L.P.