Hedge Fund That Made 6,000% on VIX Jump Bets on Next Blow-Up

Hedge Fund That Made 6,000% on VIX Surge Wagers on Next Blow-Up

(Bloomberg) -- A hedge fund that reaped an outrageous gain in February’s vol-mageddon is eyeing a fresh target.

Houndstooth Capital Management LLC secured a 6,000 percent return from a bearish bet on an exchange-traded product tied to calm markets.

Now, the $7.5 million fund sees trouble in an ETF designed to profit from the opposite -- turbulence in stocks. It’s wagering technical forces in the volatility complex will help spur a swift return to stability in the wake of a blowout, undoing the leveraged product in its wake.

It goes like this: Even though Houndstooth expects another surge in price swings, it’s using out-of-the-money puts with near-term maturities to bet against the $413 million ProShares Ultra VIX Short-Term Futures ETF. UVXY, as it is known, is one of the most liquid, leveraged ETFs that profit from rising volatility. The theory is that after an initial spike there will be a snapback in vol that will decimate the product.

“We’re looking for areas where buying or selling volatility is mispriced by the market, or at least where we think there’s a very good risk-reward trade-off,” Lincoln Edwards, founder at Houndstooth, said in an interview. “There’s a risk that another massive VIX spike could destroy UVXY in a single day.”

Tucker Hewes, a spokesman for ProShares at Hewes Communications, declined to comment.

At $70,000 the trade is modest, but it highlights the contentious issue of whether securities such as UVXY can exert an outsize pull on the very contracts they track, exacerbating their own volatility in the process.

Hot Summer

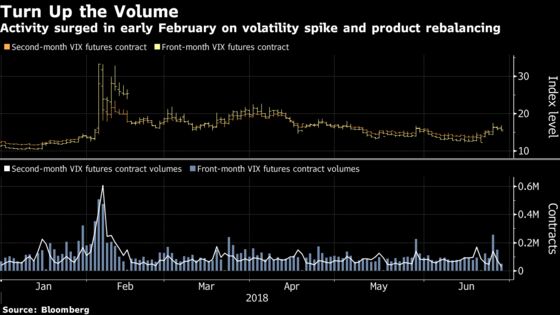

Volatility investing has boomed in recent years as ETPs offered cheap and liquid ways for professional money managers and retail investors to punt on the burgeoning asset class. As Wall Street warns of a “hot” summer full of risk, and a more normal regime for volatility after two placid years, many traders are betting on bigger price swings in the latter half of the year.

And that’s how Houndstooth made its spectacular February return. The Austin, Texas-based firm bought put options on the ProShares Short VIX Short-Term Futures ETF, or SVXY, thinking that an upward move in the Cboe Volatility Index would shake sellers out of their torpor. Sure enough, the gauge staged a record-one day spike, sending the ETF plummeting 83 percent -- and handing the fund its best-ever first quarter with a double-digit gain.

Houndstooth reckons it has a keen eye for technical risks in the underbelly of the volatility complex. Since the VIX isn’t tradable, many products hold futures contracts on the gauge. Given their size, some participants say they can exert a large pull on the price of the assets they track, underscored by the spectacular collapse of ETNs linked to calm markets in February.

Both long and short products buy and sell futures contracts on a daily basis to maintain their desired degree of exposure to implied equity volatility. That means a large one-way move in the VIX can dramatically increase the number of contracts they need to buy -- challenging liquidity and potentially driving the price of futures higher, according to Edwards.

Cboe Global Markets Inc. didn’t immediately respond to an email request seeking comment. It has recently outlined changes to the monthly auction for the VIX settlement.

Scenarios

For the Houndstooth strategy to pay off, VIX futures need to lose two-thirds of their value in a single day. That, in theory, would be enough to send the price of the 1.5-times leveraged UVXY to zero.

“Even if VIX futures gained 200 percent or even 10,000 percent in a single day, a one-day decline of 66 percent makes UVXY worth $0 regardless of how high it climbed,” Edwards said.

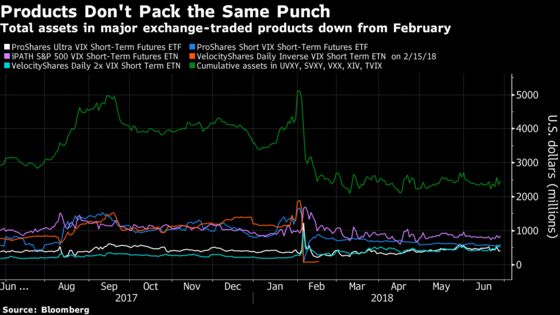

Of course, the grip ETFs assert on VIX futures likely diminished after February, as products either closed or shrank, while several ProShares ETFs reduced leverage, including UVXY, curbing their need to rebalance after sharp moves.

And the scenario didn’t play out after the VIX’s record spike on Feb. 5. The next day, the volatility gauge slumped by one-fifth -- only enough to send UVXY down by a third for the day.

Still, buying put options on the ETF rather than shorting it allows Houndstooth to limit potential losses on the trade, and there are a few scenarios that could lead to its success.

Under one, the VIX spikes from its current level to 40. The next day, as panic eases, the gauge knifes back down, its movements exacerbated by long buyers rushing to cover positions, and by volatility products flooding the futures market to rebalance holdings.

In another, the VIX could surge on bad-news speculation and then quickly reverse, producing a large enough intraday spike for the bet to pay off. Alternatively, the gauge could gradually climb higher -- only to deflate suddenly if favorable news emerges.

Edwards believes volatility is poised to move higher as November’s U.S. congressional elections approach.

“We’ll also see a third interest-rate hike, which will spark much more volatility than what we’re seeing now. Political uncertainty in Europe will continue causing major fits of volatility. Expect to see the VIX over 30 at least one more time this year,” he said.

The Houndstooth investor concedes that a 6,000 percent return on the strategy is a tail scenario -- but one “that’s massively underappreciated and underpriced.”

--With assistance from Melissa Karsh and Luke Kawa.

To contact the reporters on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net;Suzy Waite in London at swaite8@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.