Banks Rolling Over May Be a Bad Omen for This Market: Taking Stock

Banks Rolling Over May Be a Bad Omen for This Market: Taking Stock

(Bloomberg) -- Stock futures are looking a bit delicate this morning, with the e-minis down more than 10 handles and at one point coming close to testing Monday’s lows. Weakness in the global markets begets weakness in the U.S., with the persistent tumbling of Chinese stocks (H Shares joined Shanghai in a bear market today) and the breakdown in European banks (Deutsche Bank sank almost 5% to a record low) continuing to put a hurt on sentiment.

Uncertainty on trade and the mixed messages from the White House remains the number one concern for the markets -- Lighthizer made some strong comments last night on "unjustified tariffs" by WTO members and the saga over ZTE Corp. continues to drag on -- while a stunning upset in the New York primaries that shined light on the ongoing struggle over the Democratic party’s identity (and how this might look for a real challenge to Trump in 2020) is also grabbing a lot of attention today.

Ugly Action in the Banks

The action on Tuesday was a pretty clear reversal from Monday, where tech bounced back from its brutal start to the week and defensive groups (most notably, the consumer staples) turned into laggards. That all makes fine sense as there wasn’t any huge trade-related bombshell that rocked the markets like we saw on Monday. In fact, it seemed as though the finance world was more interested in the denials from Navarro and crew versus the implications from the story (an emergency law whereby U.S. would curb China investments in sensitive U.S. industries) that initially made waves.

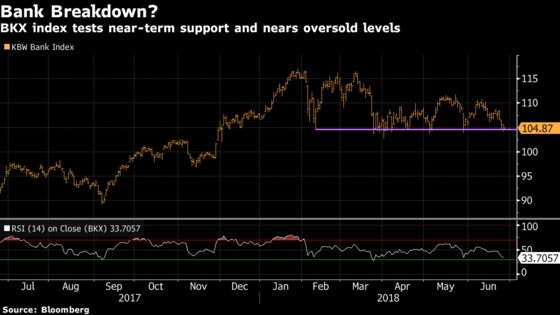

But one sector stood out like a sore thumb right from the get-go, and that’s the financials (S5FINL currently on a record twelve-day losing streak), more specifically the selling in the banks off the open that barely subsided as the day wore on. Some of these charts are just downright ugly, like JPMorgan and Bank of America both breaking their 200-day moving average last week and Goldman nearing 52-week lows (and pretty major support at the $220 per share mark).

How this tape can hold up if the banks continue to roll over is anyone’s guess, but the quickfire sentiment shift from 10-year yields to the moon (or at least well above 3.00% at this point) to major concerns about a flattening yield curve (see this QuickTake for why you should care) is something that could linger for some time.

The next catalyst is just two trading sessions away, and that would be the second round of stress test results (or CCAR). And while all 35 banks passed last week, it isn’t all sunshine and puppy dogs for this next event if you go by Bloomberg Intelligence’s take, which said Wells Fargo and Deutsche Bank’s regulatory issues may signal qualitative risk while Goldman, Morgan Stanley and State Street may need to slash their shareholder-return ambitions.

Plus we’re just a little more than two weeks away from the kickoff to bank earnings season. Last quarter was filled with awful-slash-questionable price action, where traders immediately sold into strength on virtually every major bank’s results.

Two other things that stuck out yesterday:

- Homebuilders: Could Lennar’s blowout beat, where new home orders popped 62% year-over-year, be an inflection point for a group that has done nothing but trend lower since the January peak? Maybe KB Homes will have an answer for us on Thursday

- Rental Cars: Hertz and Avis remain on shaky ground as all it took to sideswipe both stocks by 12% and 9.7%, respectively (plus the bonds, as both companies were the worst performers in the high-yield market), was a Morgan Stanley note that warned on industry fundamentals and financial leverage; welp, watch out for further pressure as Goldman cut estimates for both names last night after a survey of airport rental car rates suggests "peak season pricing may be at risk of being softer" year-over-year

Three Things to Watch

Bed Bath & Beyond’s earnings were already in focus -- options imply ~12% move on a heavily-shorted retailer who has been absent for much of the "end of retailpocalypse" trade -- but things got a little more interesting yesterday after one of the stock’s bears, Wolfe’s Adrienne Yih, called for a potential upside surprise to gross margins after doing some promo checks.

Staying in the consumer space, Chipotle’s turnaround is in full force, much to Bill Ackman’s elation (assuming Pershing is still the top holder with at least a 10% stake), but could today’s "special investor call" be a sell-the-news event with the stock already rallying 60% year-to-date? See our preview for what the Street is expecting out of the event, from updates to any outlooks to details on the company’s strategic plans.

A slew of auto suppliers relief rallied on Tuesday for the first time since Trump threatened to impose a 20% import tariff on European cars. Lear was one of them, gaining 1.7% ahead of today’s investor day -- this is a company that had ~12% of revenues tied to China and more than 10% levered to Europe in 2017 (according to Bloomberg data), so you have to think trade impact will be a topic that investors will want to hear about, especially after what we’ve seen lately from Daimler and Harley-Davidson.

Notes From the Sell Side

Goldman is incrementally negative on INTC, which is already reeling from the recent CEO resignation and two downgrades this week (Nomura Instinet and Bernstein) and AMD after a trip to Asia; on the flip side, analyst Toshiya Hari is now more positive on ON and MU..

Morgan Stanley is no longer cautious on telecom services, upgrading the sector to an in-line view (and resuming AT&T with an overweight rating) on valuations and a more balance competitive and regulatory outlook..

Bernstein says bank stock valuations are looking more attractive and upgrades STI and MTB to outperform: "The regional banks look like the big excess capital stories today, with CFG (18% of market cap), ZION (17% of market cap), and CMA (14% of market cap) at the high-end of the group."

Wolfe Research’s Nigel Coe, formerly with Morgan Stanley, has rolled out coverage on the industrials sector ("we lean more towards the ’art of the deal’ scenario in that trade tensions will simmer down"); he pins outperforms on UTX, HON, EMR, FTV, IR, ETN, RBC, HDS and underperforms on MMM, ITW, LII, FAST.

And GE gets an upgrade from Oppenheimer after yesterday’s 7.8% breakup-fueled rip, YUM is raised to a buy at BTIG on GrubHub partnership benefits, and MRVL gets a couple bullish notes with an upgrade from Deutsche Bank and an outperform initiation at Evercore ISI.

Tick-by-Tick Guide to Today’s Actionable Events

- 7:00am -- GIS earnings

- 7:45am -- EROS earnings (roughly)

- 8:00am -- UNF earnings

- 8:30am -- Durable Goods, Wholesale Inventories

- 8:30am -- PAYX earnings, GIS earnings call

- 8:30am -- AVAV investor meeting

- 10:00am -- Pending Home Sales

- 10:00am -- Senate committee meeting on reducing health care costs

- 10:00am -- World Cup: Mexico vs Sweden, South Korea vs Germany

- 10:30am -- DoE oil inventories

- 12:00pm -- MNKD investor meeting

- 12:00pm -- Bill Gates to speak at Johns Hopkins on future of U.S. leadership

- 12:15pm -- Fed’s Rosengren speaks on economics and ethics

- 12:30pm -- LEA investor day

- 2:00pm -- World Cup: Switzerland vs Costa Rica, Serbia vs Brazil

- 2:30pm -- Senate panel hearing on TMUS/S merger competitive impact

- 4:00pm -- RAD earnings (roughly)

- 4:05pm -- CAMP earnings

- 4:15pm -- BBBY, PIR, PRGS earnings

- 4:15pm -- CMG special investor call

- 4:30pm -- NTRA call to discuss strategic roadmap

- 5:00pm -- BBBY earnings call

- Tonight -- IPOs to price: BJ’s Wholesale (BJ), BrightView (BV), Tricida (TCDA), Forty Seven (FTSV), Goodbulk (GBLK), EverQuote (EVER), Translate BIO (TBIO), Neuronetics (STIM)

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.