(Bloomberg Opinion) -- General Electric Co.’s breakup gives its health-care unit a chance to shine.

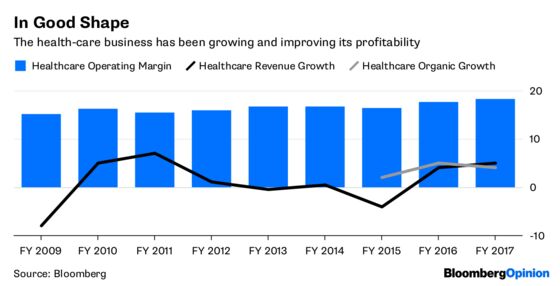

The industrial company on Tuesday said it would spin off the division as part of a broader restructuring that will also include the divestiture of its stake in the Baker Hughes energy business and a further shrinking of GE Capital. The health-care unit, which makes MRI machines and cell-therapy tools, is one of the better businesses at GE. It generates steady cash flow, its revenue is growing, and it has seen meaningful margin improvement — thanks in part to CEO John Flannery, who was brought in to fix the division in 2014 after it had hit a lull.

But as I wrote last year, the fact that the business hasn’t been a problem child has tended to mean it gets taken for granted. That was true back when GE’s biggest problems were missed growth forecasts and falling oil prices, and has only become more so as the company unraveled. No one wants to hear about biologics and digitally driven health-care services management when earnings in the power unit are falling off a cliff and the dividend is on death watch.

There’s a clear investor base for the health-care unit once it’s unshackled from the rest of GE. The S&P 500 Health Care Equipment & Services Industry index is up almost 17 percent over the past year, outpacing the broader benchmark and obviously surpassing the 50 percent decline at GE.

The media valuation for a basket of Bloomberg Opinion-compiled health-care equipment peers is about 15 times forward Ebitda. Assuming investors assign a similar multiple to GE Healthcare, back of the envelope math suggests a valuation for the business in the neighborhood of $60 billion to $70 billion. It also suggests GE was getting very little credit for that business under its current conglomerate structure.

GE will add $18 billion of debt and pension obligations to the health-care spinoff, but has yet to detail the breakdown between the two. That’s a significant piece of the company’s plan to reduce its net debt by $25 billion. The health-care unit should be able to handle it. A debt load of that magnitude would put GE Healthcare’s leverage ratio in line with peers in the BBB credit-rating tier, estimates Bloomberg Intelligence analyst Joel Levington. The leverage will be higher than what Siemens AG placed on its Healthineers spinoff on an adjusted basis, Levington said, but Siemens wasn’t under as much financial duress, so it is what it is.

Even with the liability transfer, the health-care business should have flexibility to make acquisitions. That’s the most significant benefit from this portfolio shakeup. It was striking to hear Flannery speak on the conference call about feeling held back at times from pursuing opportunities while he was running GE Healthcare. He took a different tune while serving under former CEO Jeff Immelt, who was an advocate for the benefits of being able to tap into the parent company’s resources and benefits. Some areas where the health-care unit could look for acquisitions include cell therapy, artificial intelligence and machine learning.

Taking this growing, cash-flow generating business out of GE will leave an amalgamation of longer-cycle operations, and the company will have to execute well to prove their value. But for GE investors, the prospect of owning an unleashed health-care business should be appealing.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.