Three Kids and a Flute. How India, Singapore Can End Index Feud

(Bloomberg Opinion) -- The path to ending the custody dispute between the National Stock Exchange of India Ltd. and Singapore Exchange Ltd. passes through a parable involving three kids and a flute.

A minor domestic quarrel has turned into a major court battle over who gets to trade the benchmark Indian index.

The Indian side wants exclusive rights over the Nifty 50. Singapore, where a dollar version of the gauge has changed hands for 18 years under a license, isn’t ready to lose the privilege, or profit. A judge in Mumbai recently ordered the partners to stay married at least for the rest of this year while an arbitrator tries to find a solution. This is a chance both parties should grab to prevent a messy, expensive divorce.

To begin with, Singapore should drop its plan to launch a Nifty clone. Yes, it was forced to come up with an alternative after the NSE abruptly decided to stop sharing proprietary index data for trading in any offshore venue. NSE gave SGX six months to wind up the SGX Nifty. That was unfair. But the cleverness of SGX’s alternative derivative, built around the once-a-month, publicly available settlement price of Indian index futures (instead of real-time Nifty index values) embarrassed the Indian side. Hence, the court injunction.

Instead of lawyers, it would help if politicians stepped in.

To see why, consider a little fable in economist Amartya Sen’s book “The Idea of Justice.” There’s a flute claimed in full by three children. Anne wants it because only she can play it; Bob demands it because he’s too poor to afford toys; Carla made the flute, so she believes herself to be the rightful owner.

The Singaporean position is the same as Anne’s. Despite investors having been shaken by the fight between the two exchanges, the most active June contract on SGX Nifty has 1.4 times as much open interest as the NSE’s original.

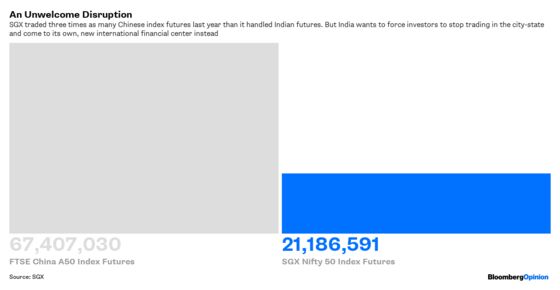

That’s not all luck. Starting in 1968, when the city-state persuaded global banks to trust it with dollar deposits when New York was off to dinner and London slept, Singapore has made big investments in its legal and regulatory architecture. Even with all that skill and reputation, SGX has managed to hit pay dirt with only a few of the many products it has tried: The FTSE China A50 Index and the SGX Nifty are its signature pieces.

However, when it comes to taxation and regulation, the Indian side is still capable of striking the odd jarring note. No surprise then that India’s Gift City, where NSE is offering its own dollar Nifty contract, isn’t exactly teeming with global investors.

NSE represents the claims of both Carla and Bob. The equity risk is Indian — not Singaporean. And since NSE doesn’t get to play with fancy toys such as the S&P 500, why should SGX make merry at its expense? No judge can resolve this dispute because, as Sen says, there’s some justice in all three claims. Only political diplomacy can ensure a harmonious solution.

One way that can happen is if NSE renews its license agreement with SGX on the condition that the Singaporeans will provide a pipe to the NSE’s operations in Gift City. The two sides began exploring a link last year before Singapore hastily announced its own suite of single-stock futures on Indian companies. SGX saw an opening created by the Indian regulator’s ban on over-the-counter offshore derivatives built around single-stock futures. But it underestimated the backlash.

It’s time Singapore gave a nationalistic New Delhi something to celebrate. A stock connect, such as between Hong Kong and Shanghai, could be the prize. It would, however, require a lot of work.

Investors should be able to see the combined order book in both India and Singapore. A trade placed by a hedge-fund customer of, say, Goldman Sachs Group Inc. or Credit Suisse Group AG in Singapore, has to be routed by SGX to this enlarged liquidity pool. Trade clearing must be guaranteed by a well-capitalized institution. The yet-to-be-appointed regulator for Gift City has to allay lingering concerns around investor anonymity and money-laundering. Tax authorities need to provide certainty on exemption from India’s 30 percent capital-gains tax.

Even after all the effort that’s currently going in into making it work, Gift City may yet flop as India’s first international financial center. The nation’s natural stock-trading hub is Mumbai, and not a patch of wilderness in Prime Minister Narendra Modi’s home state of Gujarat. Redirecting a functioning Singapore link to Mumbai wouldn’t be so hard.

Beijing had no qualms about the 67 million FTSE China A50 Index Futures traded on SGX last year, triple the volume of SGX Nifty. The People’s Republic seems to get what India has trouble accepting: Bob and Carla won’t derive any pleasure from taking away Anne’s flute — at least not until they’ve learned to attract an audience all by themselves.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.